- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted July 30, 2024 at 11:15 am

This morning’s economic releases are stronger than expected on several fronts, which is generating confusion among market participants ahead of pivotal monetary policy announcements out of Tokyo and Washington. In the US, job openings and consumer confidence beat projections, developments that coincide with a firmer-than-anticipated economic recovery in Europe. Rate watchers are responding by carefully scaling back the probabilities of imminent US and EU cuts amidst the troublesome reality that price pressures could once again accelerate. This risk is especially pronounced against the backdrop of what’s been a bumpy ride for disinflation. Emblematic of this fact are reports this morning pointing to inflation picking up steam in Berlin but decelerating in Madrid.

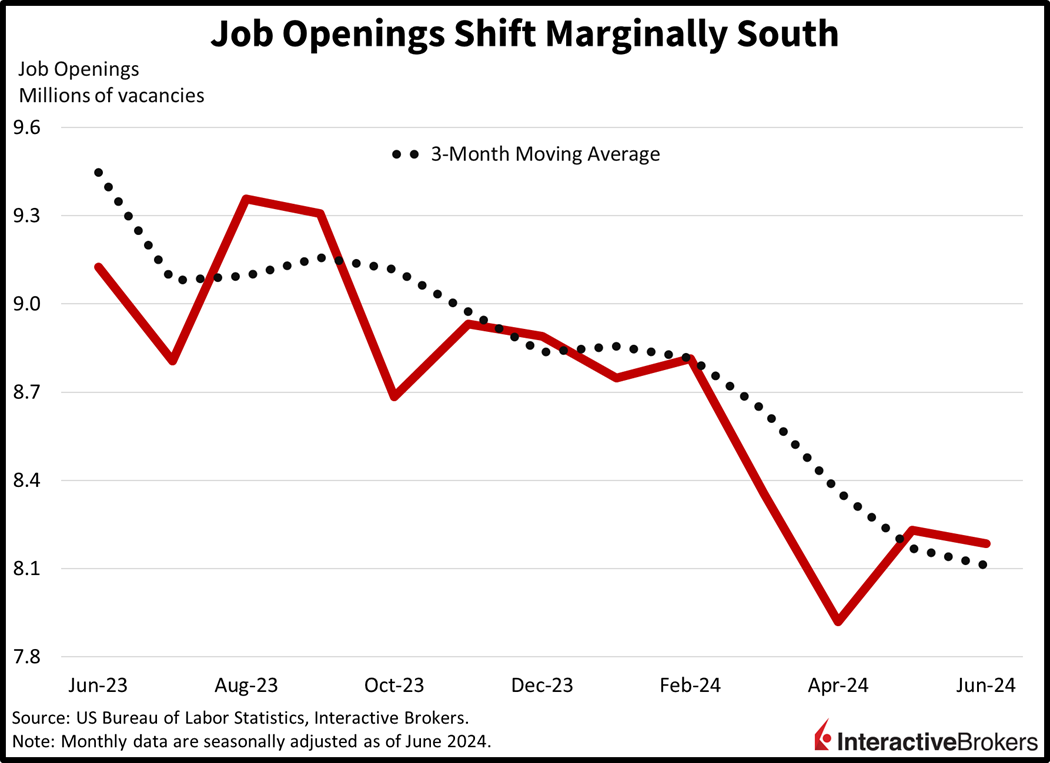

The number of businesses posting help wanted signs declined just marginally last month, issuing a blow to bond bulls who are looking for supporting evidence of a September reduction from the Fed. Job openings declined to 8.18 million, beneath an upwardly revised 8.23 million in the previous period but above the median estimate of 8 million. Quits declined, however, pointing to existing workers feeling increasingly pessimistic about replacing their current paychecks elsewhere. Continuing unemployment claims are reflecting the same dynamic, as jobless folks are taking longer to secure labor opportunities.

Softer employment conditions were also a dominant theme in this morning’s consumer confidence print, with folks feeling the worst about current labor opportunities since March 2021. Still, people are feeling slightly better than they did last month on the back of improved expectations for the future. The Conference Board’s headline figure rose to 100.3, better than the awaited 99.7 and June’s downwardly adjusted 97.8. Sentiments shifted in a bifurcated way, however, with the Present Situation Index slipping from 135.3 to 133.6 while the Expectations Index climbed from 72.8 to 78.2 during the period. Overall, households are still suffering from the familiar headwinds of elevated prices and tall interest rates, but worsening job security is the newest development weighing on families. Also hurting consumer psyche are uncertainty about November’s presidential election, a fresh 12-year low in home purchasing plans and deteriorating discretionary budgets.

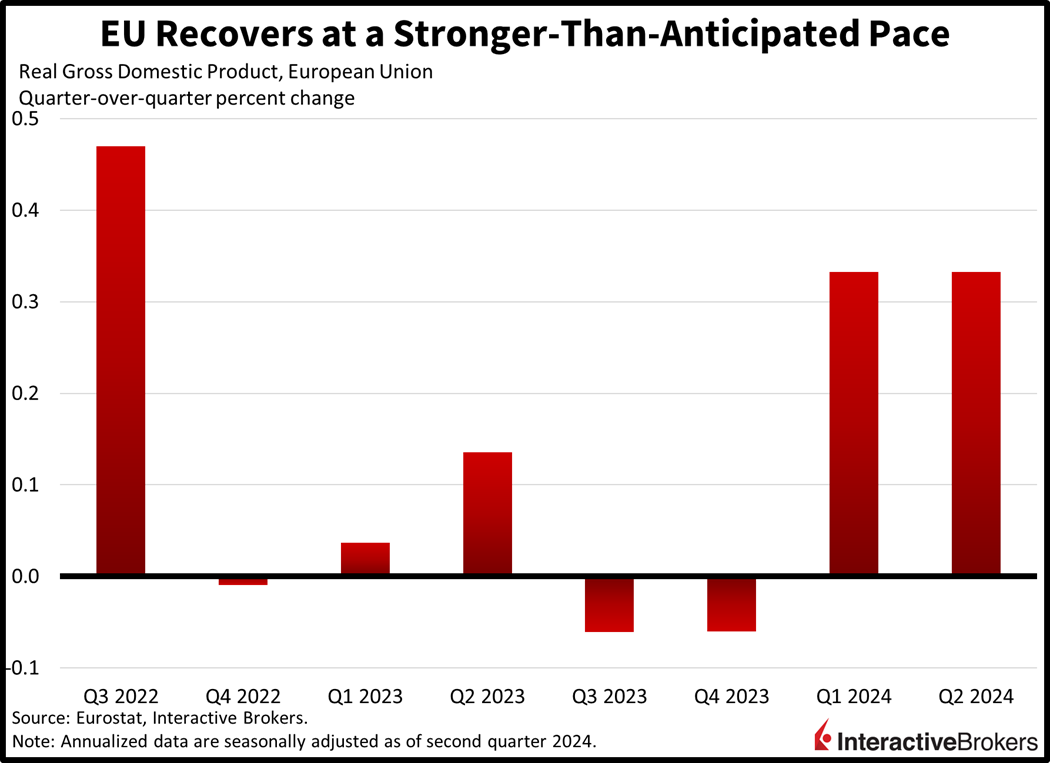

Across the Atlantic in Europe, second quarter economic growth expanded at the same pace as the previous period. The European Union’s Gross Domestic Product (GDP) release pointed to a 0.3% gain in activity, which was better than the 0.2% projection. Strong momentum in Paris and Madrid neutralized an unexpected 0.1% contraction in Berlin, the region’s largest economy.

Digital payment volumes and sales of home products imply that consumers are resilient, although at least one airline has experienced a revenue decline. These are a few observations from the following earnings highlights:

Market participants used this morning’s equity gains as an opportunity to unload stocks in the afternoon ahead of pivotal announcements from the Fed and Bank of Japan (BoJ) tomorrow as well as four of the Mag7 reporting this week. Stocks have plunged into the red with the Nasdaq Composite and S&P 500 benchmarks down 1.4% and 0.7%. The Dow Jones Industrial and Russell 2000 baskets are struggling to hold on, but are bucking the trend for now; they’re both up 0.1%. Sectoral split is negative with six out of eleven segments south on the session. Technology, consumer staples and consumer discretionary are taking the most pain, with the categories lower by 2.4%, 0.9% and 0.8%. Financials, energy and real estate are piloting the bulls, sporting gains of 1%, 0.7% and 0.3%. Treasurys and the dollar are relatively steady, however, as they await clues and commentaries from central bankers. The 2- and 10-year maturities are changing hands at 4.38% and 4.17% while the dollar appreciates relative to the euro, pound sterling and Aussie and Canadian dollars but depreciates versus the franc, yuan and yen. Commodities are taking a beating, with crude oil, copper and lumber down 1.7%, 0.8% and 0.6%. Silver and gold are trying to offset some of the bearishness with little success; they’re up by 0.3% and 0.1%. WTI crude is trading at $74.61 on worries that Beijing, the world’s largest energy importer, may fall into a recession this year. This Chinese headwind is countering supply concerns stemming from escalating geopolitical tensions between Israel and the Tehran-backed Hezbollah militia.

This week’s events are critical as we approach the weakest seasonal period for equity investors. A stacked economic calendar is lined up with big-tech earnings and central bank decisions. In Tokyo, traders will look for the BoJ to likely continue tightening policy, increasing the potential for a stronger yen and an unwinding of stock holdings. In Washington, market participants are hoping the Fed is sensitive to the risk in today’s erratic consumer behavior amidst a turn in labor market conditions. Big-tech earnings are also significant, with artificial intelligence (AI) optimism serving as the number one catalyst to this year’s stock market rally. Bullish players will be aiming for a bright picture on the future of AI in Mag7 earnings calls while bears wish that firms allude to AI delivering to the bottom line years from now, rather than right now.

Visit Traders’ Academy to Learn More About Consumer Confidence and Other Economic Indicators

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!