- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted March 15, 2023 at 12:29 pm

This morning’s retail sales data and Producer Price Index (PPI) are strengthening expectations that the Federal Reserve will raise the fed funds rate by only 25 basis points (bps) or perhaps make no rate change when it meets next week. However, investors this morning are renewing their focus on the troubled banking sector after Saudi National Bank said it won’t increase its investment in troubled Credit Suisse due to regulatory requirements.

Credit Suisse has been hit hard by a surge of customer withdrawals and financial losses, which led the bank to raise $4 billion through an equity offering last fall. This morning, the Saudi National Bank news ignited fresh concerns about the Swiss bank and the impact of aggressive monetary tightening worldwide on the overall banking sector’s financial stability.

Just one day after shares of U.S. banks rallied as investors became optimistic that the SVB Bank and Signature Bank failures were isolated events, Credit Suisse shares have dropped more than 25%, while shares of other European banks such as Société Générale, BNP Paribas, UBS and Deutsche Bank have fallen as much as 10%.

Equities and yields are plunging this morning as investor concern about a potential bank contagion heightens. The S&P 500 Index is down 1.7% after a robust relief rally that brought it near its pivotal 200-day moving average at 3939 just yesterday. Growth equities are outperforming this morning, however, as lower interest rates increase the attractiveness of future cash flows, with the NASDAQ index down 0.9%. Yields are falling hard as European investors flock into U.S. Treasuries to preserve capital. The 2-year yield is down 44 bps to 3.79% while the 10-year yield is down 24 bps to 3.39%. Lower yields are failing to dent the dollar this morning with euro weakness providing tailwinds. The Dollar Index is up 1.3% to 104.96 as the euro is down 1.7% versus the dollar. Crude oil is resuming its downtrend as recession and oversupply fears weigh upon prices. The International Energy Agency signaled that global energy markets are in surplus, meaning that there are more than ample supplies. WTI crude oil is getting hammered, with its price down 4.1% to $68.48 per barrel, its lowest level since December 2021.

The decline in eating out alongside the rise in grocery spending may be emblematic of consumers shifting spending from wants to needs, or from discretionary spending to staples. We will continue to watch these patterns closely to determine the turning point of consumer spending which will likely coincide with labor market softness and recession.

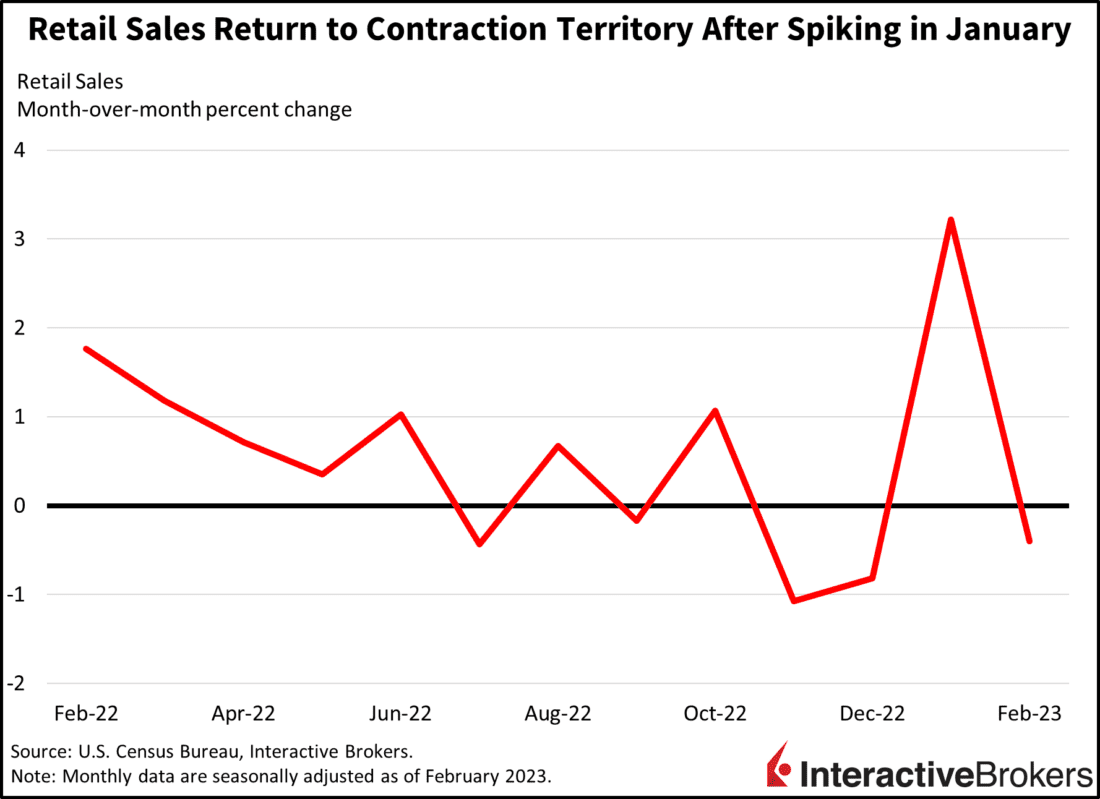

As banking fears surge among investors, it appears that the financial system may receive a reprieve from more aggressive rate hikes, at least in the U.S., with this morning’s retail sales data and Producer Price Index portraying moderating inflation and offsetting fears of persistent price increases that were sustained by yesterday’s Consumer Price Index. The Commerce Department reported this morning that sales fell by a seasonally adjusted 0.4% rate last month and weaker than the consensus expectation for -0.3% and January’s impressive revised 3.2% gain. Weighing on the headline number were transactions at department stores, furniture shops, dining and drinking parlors, automobile and parts retailers and apparel, dropping -4.0%, -2.5%, -2.2%, -1.8% and 0.8%. Sporting goods and hobbies, as well as building materials, weighed at modest levels. Offsetting broad weakness was online shopping, health and personal care stores, groceries and electronics, with each notching gains of 1.6%, 0.9%, 0.6%, and 0.3%. The decline in eating out alongside the rise in grocery spending may be emblematic of consumers shifting spending from wants to needs, or from discretionary spending to staples. We will continue to watch these patterns closely to determine the turning point of consumer spending which will likely coincide with labor market softness and recession.

The services sector has been problematic for inflation because demand for entertainment, travel, and dining out increased significantly during social distancing policies and economic shutdowns intended to curtail the spread of Covid-19. February’s report shows that the pent-up demand may be winding down as consumers succumb to the pressure of higher prices and declining savings.

This morning’s PPI release also implies that inflation may be easing. Supplier prices declined 0.1%, lower than expectations of an unchanged pace from January’s 0.3% rise. The PPI was weighed down by foods, with egg prices dropping 36.1% during the period. Energy, trade and transportation also acted as inflationary headwinds, as weakening demand drove lower prices at the wholesale level. The Core PPI, which excludes energy and food, climbed only 0.2% month over month (m/m) compared to the 0.5% increase in February. After hitting a year-over-year peak of 11.7% early last year, February’s y/y PPI increased only 4.6% compared to the revised 5.7% increase in January and the Core PPI increased 4.4% y/y, matching its January rate.

The retail sales data and PPI are countering inflation fears that were stoked yesterday by the Consumer Price Index, which climbed 6% y/y in February despite declining energy and goods prices, such as heating oil, natural gas and used cars and the Core CPI, which excludes volatile energy and food prices, advanced 5.5% y/y.

As fears about inflation subside, at least temporarily, the health of the banking sector is likely to become a major driver of market performance in the coming weeks. If bank stability issues spread to additional institutions, investors are likely to continue selling equities and rush to safe-haven Treasuries. In this regard, future market direction may be influenced by the scope of bank’s past efforts to leverage their returns by investing in long duration bonds that are the most susceptible to interest rate changes. On the other hand, if the bank troubles appear to be isolated events, investors could potentially shift their focus to softening prices and the potential for the fed to tilt dovish in its battle against inflation. This shift in focus toward a dovish fed could help reverse the current market selloff and place strong bids in favor of beaten-down, well-capitalized, rate sensitive growth stocks.

Visit Traders’ Academy to Learn More about Retail Sales and Other Economic Indicators.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

There is a substantial risk of loss in foreign exchange trading. The settlement date of foreign exchange trades can vary due to time zone differences and bank holidays. When trading across foreign exchange markets, this may necessitate borrowing funds to settle foreign exchange trades. The interest rate on borrowed funds must be considered when computing the cost of trades across multiple markets.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Spot currencies are not available at IBKR Singapore.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!