- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted February 7, 2025 at 9:45 am

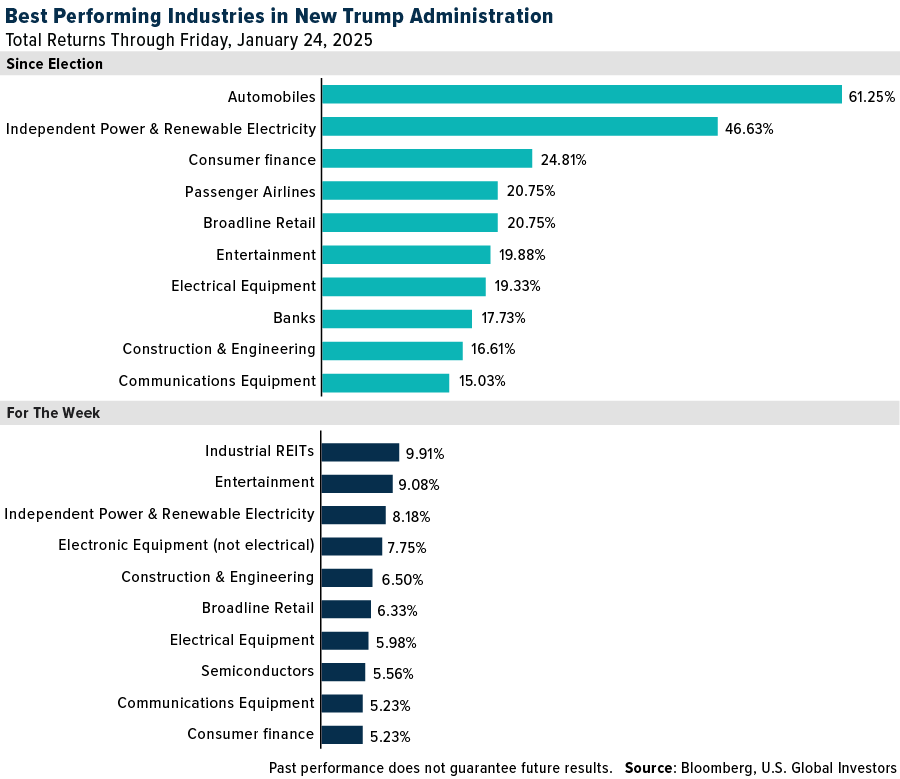

Tech stocks are selling off sharply today, triggered by concerns that China’s just-released DeepSeek AI assistant may steal the thunder from U.S.-based platforms like OpenAI’s ChatGPT. Before this week, however, markets have been responding with gusto since November’s presidential election, especially in a few key—and perhaps expected—industries.

The biggest winner so far was the automobile industry, led by Tesla, up an impressive 70% since Election Day as of Friday. General Motors, while not quite as flashy, was up about 5%. Despite President Donald Trump’s rollback of Biden-era electric vehicle (EV) mandates, Tesla has continued to command investor confidence, possibly due to Elon Musk’s close ties to the president.

Electricity producers also saw a boost, driven by the AI boom. Data centers, which currently consume 1-2% of global power, could grow to 3-4% by the end of the decade, according to Goldman Sachs.

And let’s not forget the airlines industry. United Airlines, up 33%, capitalized on record-breaking TSA screenings in 2024, operating its largest-ever domestic schedule and expanding international routes.

I also want to share the best performing industries for the five-day period as of last week, as President Trump has signed an historical number of executive orders (EOs) since taking office. The list includes many of the same areas—power generation, construction & engineering, consumer finance, retail—but there’s an interesting addition: industrial REITs.

The industrial REIT ticker is represented by a single stock, Prologis, the world’s largest industrial property developer. According to the Wall Street Journal, the company has seen its warehouse business explode since the election. It’s also been dipping its toes in the white-hot data center market, selling a facility in the fourth quarter, with more in the pipeline.

But let’s pivot to a different story—one unfolding far from Wall Street. I recently spoke with Jonathan Roth, founder of ResourceWars.com and a veteran of capital markets, who highlighted an increasingly urgent issue: the Arctic.

As polar ice caps melt, new opportunities—and risks—are emerging in this increasingly contested region. Nations like the U.S., Russia and China are jockeying for influence, not only to access the Arctic’s vast natural resources but also to secure strategic military and trading advantages.

Greenland, in particular, is shaping up to be a geopolitical hotspot, and it’s no wonder that Trump has repeated his interest in acquiring the island.

During our conversation, Jonathan emphasized the Arctic’s immense resource wealth. The region is home to some of the world’s largest untapped reserves of natural resources. A 2008 study by the U.S. Geological Survey says that the Arctic holds 1,670 trillion cubic feet of natural gas and other fuels—equivalent to Russia’s entire oil reserves and three times those of the U.S.

Greenland, the world’s largest island that isn’t a continent, is rich in critical minerals essential for modern technologies, including rare earth metals, graphite, niobium and titanium. These materials are vital for everything from smartphones to EVs to military hardware.

Ice loss in the Danish territory has also exposed significant deposits of lithium, hafnium, uranium and gold. A 2023 survey by the Geological Survey of Denmark and Greenland evaluated 38 raw materials on the island, most of which have high or moderate potential.

Jonathan also pointed out that Russia has been quietly building its Arctic presence for over a decade. It now has the most significant military presence in the region, with refurbished Soviet-era bases and a fleet of nuclear-powered icebreakers.

In 2024, some 38 million metric tons of cargo were shipped through Russia’s Northern Sea Route (NSR), a record amount for a single year and a nearly tenfold increase from a decade earlier. The NSR is central to President Vladimir Putin’s vision of a shipping lane that rivals the Suez and Panama Canal, but challenges like shallow, ice-filled waters and foggy conditions mean the route has a long way to go before becoming a global sea lane.

The country’s Arctic ambitions are about more than just trade. The region is a cornerstone of its strategy to secure military and economic power. This poses a significant concern for the U.S. and its allies, especially as climate change accelerates ice melt and opens up new access routes. Russia’s dominance in the Arctic could disrupt global trade, heighten geopolitical tensions and undermine U.S. strategic interests.

While Russia boasts dozens of icebreakers, including nuclear-powered vessels, the U.S. is woefully behind. Jonathan highlighted that the last heavy polar icebreaker built by the U.S., the Polar Star, was commissioned nearly 50 years ago, in 1976. Meanwhile, the newer Polar Security Cutter (PSC) class of icebreakers, intended to bolster U.S. capabilities, has faced years of delays and budget overruns.

Recognizing this, the U.S. has partnered with Canada and Finland under the ICE Pact to develop a new generation of icebreakers. Finland, which designs 80% of the world’s icebreakers, brings valuable expertise to the table.

Greenland’s importance extends beyond its resource wealth. Jonathan noted the island occupies a key position along two potential Arctic shipping routes—the Northwest Passage and the Transpolar Sea Route. As sea ice continues to melt, these routes could significantly reduce shipping times and bypass traditional chokepoints like the Suez and Panama Canals.

Greenland is also home to Pituffik Space Base (formerly Thule Air Base), a critical U.S. military installation for missile early warning and space surveillance. The base’s strategic value is compounded by Greenland’s role in the so-called GIUK Gap (Greenland-Iceland-United Kingdom)—a naval chokepoint in the North Atlantic.

Investment in Pituffik has been inconsistent, however, and its importance has waned since the Cold War. Renewed attention to Greenland could help the U.S. counter Russia’s growing Arctic dominance and China’s ambitions as a “near-Arctic” power.

The Arctic’s significance isn’t just about resources or shipping lanes. It’s about power, influence and the ability to shape the future of global trade and security.

For investors, the region offers opportunities in sectors like energy, mining and infrastructure. Companies involved in rare earth mining, icebreaker construction and Arctic logistics could see significant growth as nations ramp up their Arctic investments.

As always, investors should keep a close eye on these developments. The Arctic may be cold, but the race for its riches is heating up.

To watch my full interview with Jonathan Roth, click here!

—

Originally Posted January 27, 2025 – Cold War 2.0? Russia, China and the U.S. Clash Over Arctic Resources

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2024): Tesla Inc.

All opinions expressed and data provided are subject to change without notice. Holdings may change daily.

Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

About U.S. Global Investors, Inc. – U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by clicking here or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Foreside Fund Services, LLC, Distributor. U.S. Global Investors is the investment adviser.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from US Global Investors and is being posted with its permission. The views expressed in this material are solely those of the author and/or US Global Investors and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

The fight over the arctic. Fleet capacity, both military and commercial is at a critical standstill in the US especially. Between mismanaged shipyards, delays in procurement and inferior production quality, we are way behind the rest of the World. The American Ship production is in shambles and I have a hard time seeing anything I would bet my dime on. Instead, I have been looking for investment alternatives in European stock. Why? Why bother? When the segment has been on a steady downward slope over the last 15 years? Because of the change in the Global powers structure. That became evident during Trumps first term, and during COVID and the trend of a rebalancing the world power has been obvious since. I took a chance with BAE when it valued at 700p. I took a deep look into who supplied them with engines and other large parts over the years and sought to see what was in the pipeline. And maintenance+repair is not a bad word!. I started to look at HAL around the same time, but is has been stagnant. If exploration of the Arctic is a goal, and if an ethical approach is taken to at least curb the Russian and Chinese advances until we in the West can forge the right alliances within the nations that are the Arctic we need; better, nimbler and more advanced vessels. Fast. A nimbler political attitude will greatly improve our chances for deal making with Denmark and Greenland for example And let’s not forget Canada with its ties to the UK. The next 5-8 years will see an increase in the European share of output. And the sooner we get onboard with collaborating with nations that did not underestimate the value of strong fleets – both Mercantile and Military, the sooner we can be part of playing the game.