- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted November 28, 2023 at 7:56 am

1/ This Time is Different

2/ Ever Since Covid…

3/ Bond and Rates

4/ A Divergent Weekly Chart

5/ A 26wROC Ranking System

Investopedia is partnering with CMT Association on this newsletter. The contents of this newsletter are for informational and educational purposes only, however, and do not constitute investing advice. The guest authors, which may sell research to investors, and may trade or hold positions in securities mentioned herein do not represent the views of CMT Association or Investopedia. Please consult a financial advisor for investment recommendations and services.

There aren’t too many times when one can observe the markets and truly, authentically state that “this time is different,” but… this time is certainly different when it comes to the interest rate and bond markets.

For years, I’ve been talking to our clients about how, “One day, rates are going to stop trending down, and when they do, not only is it going to be painful for borrowers, but more importantly, it’s going to be painful for late-career working professionals and retirees who have been taught all their lives that “bonds are safe.”

The chart above is the 30-year Treasury Yield – so think, “government bonds with a 30-year maturity.” My 4th grader can look at this chart and see that, over the course of four decades, rates trended down with brief mean reversions back to the trendline…

…but things are different now, and we all know that rates have been driven higher by the Fed and inflation. The problem is, of course, that rates have been going up for more than two years now, but most investors haven’t been paying attention. Instead, their 60/40 portfolios have been decimated, not only because stocks have gone down, but moreso due to the vaporization of money in the bond market.

When a “balanced” portfolio is down -37% in 2022, and the reason is “Well, bonds were down a lot,” is that a satisfactory explanation?

This is the beauty of technical analysis and charts. While the news isn’t always actionable, the charts most certainly are!

In the chart above, I zoomed in on the same 30-year Treasury yield in the previous chart, but now we’re looking at it since the COVID bottom.

Notice how there have been brief periods of time over which an investor might’ve thought to themselves, “this is the top in rates, now bonds will be safe again,” but that simply wasn’t (and still isn’t) the case.

Even now, as Jerome Powell and the Fed hint at pausing rate hikes, there is still too much economic uncertainty to know for sure whether we’ve seen an intermediate-term high in rates, or if this is just another pause before a new climb higher.

Look at the chart – can you tell whether or not this is the big peak in rates?

Why did bonds get beaten up so bad? It’s simple…

When rates go down (like they did from the 1980s thru the late 2010s), bonds go up. However, when rates go UP, bonds go DOWN. There is no analytical element here – no secret indicator – they’re inversely related… period.

So, when the Fed started hiking rates, that should’ve been the first “red flag” indicating future potential bond carnage on the horizon.

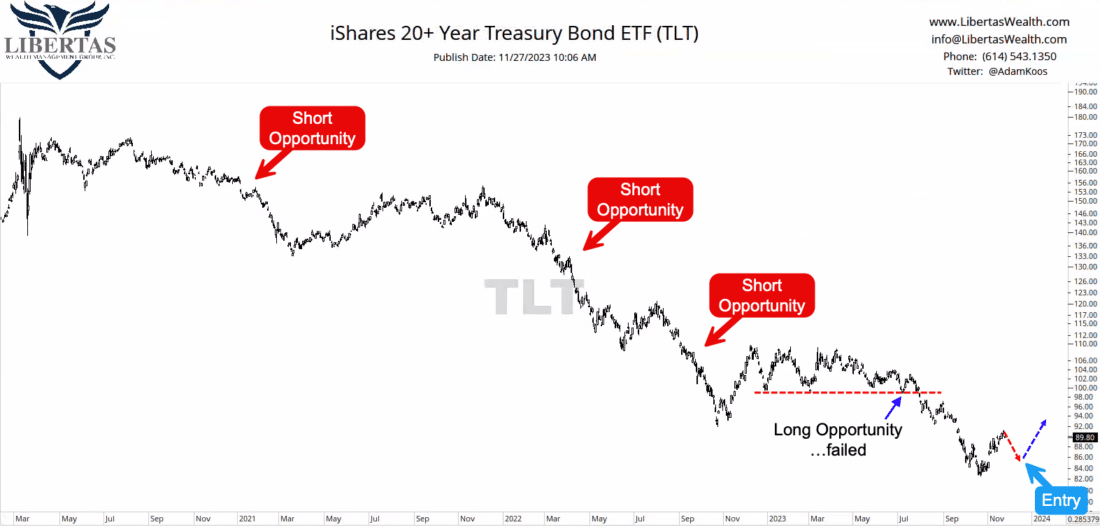

In the chart above, you might notice there were times when one could’ve considered shorting bonds to make a profit as they fell, although it’s easier to see in hindsight, and of course, shorting anything is only appropriate for investors who can tolerate that kind of activity in their investment portfolios.

That being said, there was also a good risk/reward opportunity this summer to go long bonds (in this case, TLT), but that trade failed… granted, the total loss (if using the red dashed line as a stop-loss) was extremely mild. Hence “good risk/reward opportunity.”

Today, however I wouldn’t be trying to catch a falling knife. While bonds have bounced impressively these past few weeks, I’d rather wait for a pullback, a new higher-low to use as a potential entry point, below which I’d be putting my stop.

Until then, I’d much rather camp out in the metaphorically heated, comfy lodge provided by short-term treasuries, which are currently paying around 5.3% with MUCH less risk.

Out of curiosity, I “scanned out” here, looking at TLT on a weekly chart to see if anything interesting revealed itself and I did notice a small (albeit weak) positive momentum divergence (see the lower pane – higher lows vs. lower-lows in price, above).

Divergences can be “hints” that suggest a potential future trend change, but when analyzing RSI(14) specifically, I prefer to “trust” the divergences that bottom above 30 more than those that still remain in a bearish regime.

Full disclosure: Weekly charts are much slower than daily charts, so it would also require a lot more time to pass before we could see another high, and then another higher-low in momentum ABOVE the 30 level. Point being, there’s nothing wrong with analyzing different types of charts, but always know your timeframe and stick to it!

Above is a 26-week rate-of-change (26wROC) ranking system (which is a great way to track momentum over the intermediate-term), and in this case, I’ve included a relatively robust inventory of fixed income / bond ETFs.

What you should notice immediately is the top two positions – both of which are inverse ETFs. Said another way, the best bond ETFs on this list are essentially investments that bet against the bond market!

If you let your eyes fall further down the list, you’ll see that international bonds are performing “okay,” as are convertible and high-yield bonds (although, the latter two tend to be more correlated with equities than other fixed income investments).

The rest is a lot of short and ultra-short term debt, which again lends more evidence to the fact that T-bills are STILL a great place for “bond money” vs. taking additional risk in other areas of the bond market.

—

Originally posted 28th November 2023

Investopedia.com: The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. While we believe the information provided herein is reliable, we do not warrant its accuracy or completeness. The views and strategies described on our content may not be suitable for all investors. Because market and economic conditions are subject to rapid change, all comments, opinions and analyses contained within our content are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy. This information is intended for US residents only.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Investopedia and is being posted with its permission. The views expressed in this material are solely those of the author and/or Investopedia and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Municipal Bonds are only available from Interactive Brokers for IBKR LLC, IBKR Canada, IBKR Hong Kong, IBKR Australia and IBKR Singapore entities.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!