- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted May 30, 2024 at 11:00 am

Equity bears are striving to control the market narrative as lackluster corporate earnings arrive while investors contend with a downwardly revised GDP report. While we’re hearing struggles from publicly traded companies on earnings calls, privately held firms are facing similar margin compression, with this morning’s publication on economic growth featuring the first quarterly decline in overall corporate profits in a year. Inflation data, meanwhile, was also adjusted to the downside, which is giving bond and gold bulls a reprieve in what’s looking like traditional risk-off trading. Figures on the real estate sector and labor market released this morning didn’t mark much of a shift, with the former struggling amidst awful rate and price dynamics while the latter benefits from persistent demand for workers.

US first-quarter economic growth slowed to 1.3%, according to this morning’s first revision of Gross Domestic Product (GDP), down from the 1.6% previously reported and fourth quarter 2023’s pace of 3.4%. The adjustment primarily reflects lighter goods consumption and a wider trade deficit. Meanwhile, corporate profits, released in the same report, declined 0.6% on a quarter-over-quarter (q/q), annualized basis, the first drop in 12 months. The revised report also recorded headline and core personal consumption expenditures price indices rising at quarterly, annualized rates of 3.0% and 3.1%. Both were revised downward 10 basis points (bps).

The labor market was little changed during the previous two weeks from a layoff perspective, with unemployment claims remaining well-anchored. Initial unemployment claims came in at 219,000 for the week ended May 25, near the median estimate of 218,000 and the prior period’s 216,000. Continuing claims arrived at 1.791 million for the week ended May 18, also close to projections of 1.8 million and the previous interval’s 1.787 million. Four-week moving averages did rise slightly for both indicators, from 220,000 and 1.781 million to 222,500 and 1.786 million.

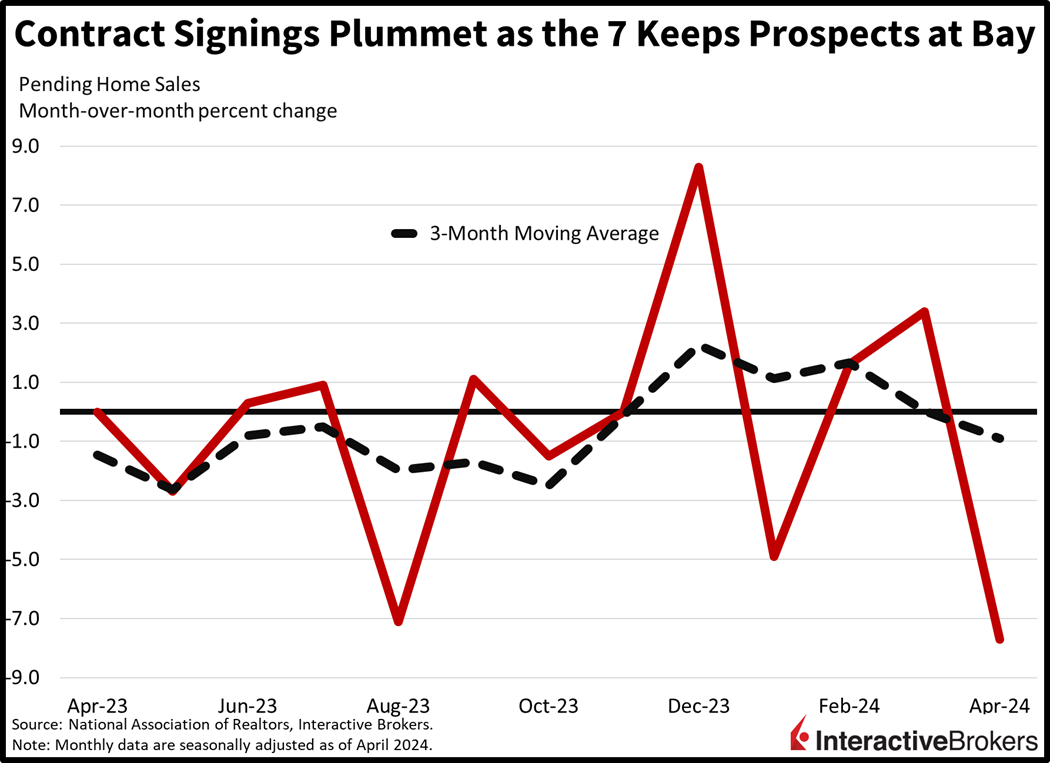

Elevated borrowing costs and all-time high prices continue to freeze real estate activity, with April contract signings dropping sharply. Pending home sales fell 7.7% m/m and 7.4% year over year (y/y), according to the National Association of Realtors. Last month’s data missed expectations by a wide margin, with economists expecting a m/m decrease of just 0.6%, while March’s results sported increases of 3.6% m/m and 0.1% y/y. The m/m shift can be easily explained by mortgages shifting from a 6-handle to a 7 during the period. Pending home sales lead future existing home transactions, as contract signings occur before keys are exchanged.

Recent earnings reports show that technology companies are generating mixed results while consumer financial malaise is challenging retail sales and causing store operators to maintain a cautious outlook for the remainder of the year. Consider the following earnings highlights:

Risk-off sentiments are driving Wall Street today, with market players dumping stocks while scooping up gold bars and Treasurys. Most major indices are moving south with the Dow Jones Industrial, Nasdaq Composite and S&P 500 benchmarks losing 0.8%, 0.6% and 0.4%. There are some glitches occurring with the Dow and S&P indices, meanwhile, with several data reporters reflecting frozen prices (38055.11 and 5241.70) for the indices and replacing them with the corresponding ETFs, in this case tickers DJI and SPY. The small-cap Russell 2000 is up a sharp 1.1% and is the sole gainer among the top US gauges. Sectoral breadth is surprisingly positive, with the selloff concentrated in technology and communication services, which are lower by 1.7% and 0.5%. Treasurys are catching a bid, with the 2- and 10-year maturities changing hands at 4.93% and 4.55%, 5 and 7 bps lower on the session. The dollar is selling off on firmer Fed easing expectations and lighter yields, with the greenback’s index down 44 bps to 104.66. The currency is down relative to all of its major counterparts, including the euro, pound sterling, franc, yen, yuan and Aussie and Canadian dollars. Risk-on commodities that depend on economic activity are getting battered while safe-haven gold is performing well. WTI crude oil and copper are down 1.2% and 2.7% while gold travels north by 0.3%.

The unexpected fall in corporate profits was this morning’s most compelling development. While the figure is broad, encompassing large Fortune 500 companies as well as mom-and-pop shops, such as those in my old Queens neighborhood, it has significant implications for earnings expectations for the S&P 500, particularly at a time when we’re sporting heavy profit margins while trading at 21 times forward earnings. Additionally, investors are assessing the likelihood that the Fed is unlikely to cut rates imminently. If corporations fail to meet earnings expectations going forward and growth projections are pared back following decelerating consumption and a challenging cost landscape, valuations and margins are increasingly likely to face mounting pressure. Finally, tomorrow’s personal income and outlays report will provide a shorter-term look at growth, spending, income and inflation dynamics for the month of April.

Visit Traders’ Academy to Learn More About GDP and Other Economic Indicators

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!