- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted December 10, 2024 at 12:42 pm

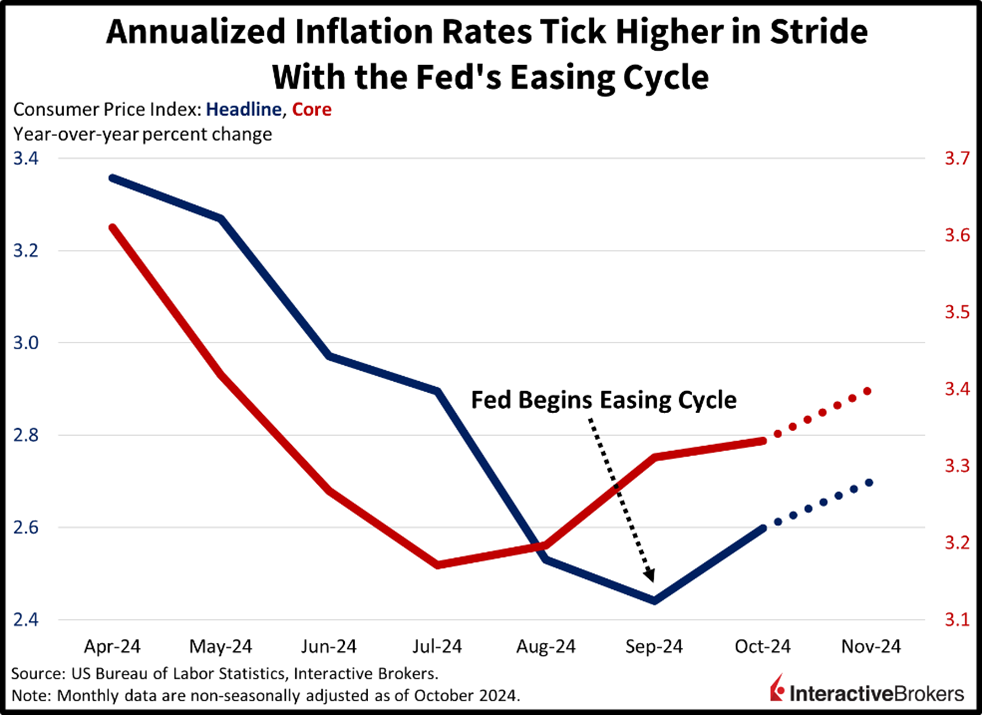

US stocks are stalling near all-time highs as investors await this year’s final CPI report, which is expected to reflect another increase in the annualized headline figure. Indeed, price pressures began to pick up following the Fed’s 50-bp interest rate reduction in September and the outlook into next year is complicated by the incoming administration, whose policy mix includes tariffs, tax relief, lighter regulations and a made in America manufacturing push, proposals that carry the potential to propel costs from both the demand and supply angles. Still, the Fed is expected to trim its key benchmark next Wednesday, following projections that the central banks of the European Union, Canada and Switzerland will cut this week. Against this backdrop, however, the ECB faces the challenge of engineering monetary policy while budget turmoil grabs Paris and Berlin and the continent teeters on the edge of recession. The BoE, meanwhile, is likely to maintain its current rate at its gathering this month, ahead of resumed talks between London and the EU on improving their economic relationship in a post-Brexit world.

Members of the European Central Bank (ECB) are debating if rate cuts can help thwart a potential recession considering significant structural and geopolitical issues on the continent. Inflation hawks maintain that the region’s economy is hobbled by a lack of business investment, an overreliance on manufacturing, high energy prices, weak demand, aging demographics and a labor shortage. Potential tariffs could be another headwind, with some of Europe’s largest economies, such as Germany, France and the Netherlands, dependent on exporting. Those concerns are countered by policymakers who believe a large reduction could help stimulate growth by reducing interest expenses and propelling consumption and investment as a result.

Shifting east, China’s balance of trade expanded last month, but its exports decelerated meaningfully, a sign of sluggish manufacturing activity ahead of the Trump administration’s return. And while some government leaders from around the world have embraced the former president with a welcome back attitude, officials in Beijing have been preparing early for tit-for-tat actions against Washington, especially after learning the lessons from last time. The Trump overhang looms large in the Far East powerhouse, as protectionist trade policies have and continue to stand in the way of President Xi Jin Ping’s lofty ambitions. Looking under the hood, exports rose 6.7% year over year (y/y), beneath the median estimate of 8.5% and the former month’s 12.7% growth rate. But imports declined 3.9% y/y, also missing expectations of 0.3% and falling faster than the previous period’s 2.3% drop. Meanwhile in Seoul, President Yoon Suk Yeol is in a precarious position following his attempt at martial law, with the opposition determined to oust him amidst the arrest of the nation’s former defense minister.

Oracle (ORCL) revenue and earnings grew 9% and 26% (y/y) but fell short of analyst expectations during its fiscal second quarter. Encouragingly, record-high demand for AI drove a 52% increase in sales for the company’s Oracle Cloud Infrastructure product. Oracle also announced it will provide cloud services for Facebook owner Meta (META), which is developing large language models. However, the company’s guidance was weaker than anticipated and its share price dropped more than 7% last night. MongoDB (MDB), which provides document-based database technology used by application developers, posted a 22% y/y revenue jump that along with adjusted earnings exceeded expectations. MongoDB’s provided upwardly revised full-year guidance that was strong than analyst expectations. In the real estate sector, homebuilder Toll Brothers (TOL) produced a 25% y/y increase in the number of homes it delivered, but the dollar value of its backlog of orders contracted 7%, causing the company’s shares to drop approximately 4% last night. Its recent-quarter earnings and revenue exceeded Wall Street estimates. Auto parts and tool provider AutoZone (AZO), however, posted results that missed expectations. Its comparable US and international sales climbed only 0.3% and 1% compared to estimates of 0.74% and 1.02%, respectively.

Today’s trading features a stronger greenback and taller borrowing costs amidst flat stocks, with investors waiting for an all-clear CPI signal to add risk to portfolios. All major domestic equity benchmarks, including the Russell 2000, Dow Jones Industrial, S&P 500 and Nasdaq 100, are nearly unchanged. Similarly, sector breadth is split, with 6 out of 11 segments gaining on the session and led by communication services, consumer discretionary and energy, which are higher by 1.4%, 0.7% and 0.6%. The laggards, meanwhile, are represented by real estate, materials and utilities, which are lower by 0.9%, 0.7% and 0.7%. Treasurys are getting sold as rate watchers hesitate a bit ahead of tomorrow’s big CPI print. The 2- and 10-year maturities are changing hands at 4.17% and 4.24%, 4 and 3 basis points (bps) heavier on the session. Loftier borrowing costs are assisting the dollar, with its benchmark flying north by 39 bps as the US currency appreciates against the euro, pound sterling, franc, yen and Aussie and Canadian tenders. It is depreciating relative to the yuan though. Commodities are tilted bullishly, with crude oil, gold and silver higher by 1.3%, 1.2% and 0.5% while copper and lumber are flat. WTI crude is trading at $69.01 per barrel as Middle East nervousness bolsters prices.

An acceleration of monthly and annualized Consumer Price Index (CPI) figures is being penciled in by Wall Street economists and IBKR ForecastTrader participants alike as a supportive Fed, accommodative fiscal policy, tight labor conditions and buoyant capital markets stoke demand. November’s CPI is expected to jump 0.3% month over month (m/m) and 2.7% y/y, up from 0.2% and 2.6% in October. And while my headline estimate is in-line with the consensus, I am anticipating core to come in at 0.3% m/m and 3.4% y/y, a tenth loftier than the median estimate for the annualized number. Diving into segments, shelter, used and new automobiles, transportation services, medical care, apparel and food are likely to support higher charges while energy costs provide relief. Finally, the Fed will realize after its reduction next week that the neutral rate is closer to 4% rather than 3.5% and is likely to respond with long pauses in monetary policy adjustments next year.

Source: ForecastEx

To learn more about ForecastEx, view our Traders’ Academy video here

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

This is commentary on economic, political and/or market conditions within the meaning of CFTC Regulation 1.71, and is not meant provide sufficient information upon which to base a decision to enter into a derivatives transaction.

Interactive Brokers LLC is a CFTC-registered Futures Commission Merchant and a clearing member and affiliate of ForecastEx LLC (“ForecastEx”). ForecastEx is a CFTC-registered Designated Contract Market and Derivatives Clearing Organization. Interactive Brokers LLC provides access to ForecastEx Forecast Contracts for eligible customers. Interactive Brokers LLC does not make recommendations with respect to any products available on its platform, including those offered by ForecastEx.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

obviously, some knew that tomorrow’s # will be higher than expected for it is well know that info is released to a select few in tb e financial world. I know of no sound reason why investors would not accept that fact. But to address this article and expect a higher # tomorrow just reiterfies the fact that no cut is mandated for the totally uncalled for setmber Biden cut is still being digested.

Either you need to use spell check or consult a dictionary. I see why you remain anonymous.

A greenback is green. A buck and a bond. A bond and a buck. Treasure is costly, treasuries are cheap. Treacle Treason Reason Real Read Reap Dervish