- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted October 13, 2021 at 10:30 am

What happens when the Fed tapers? That is the billion (or trillion) dollar question. Before we delve into the possible outcome(s) though, we must first understand what tapering means.

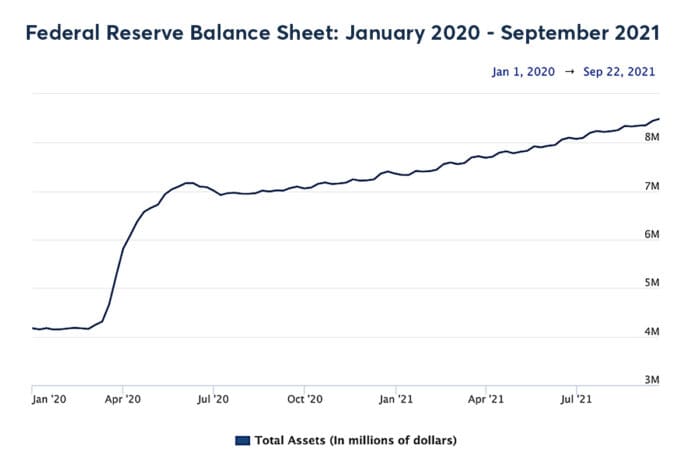

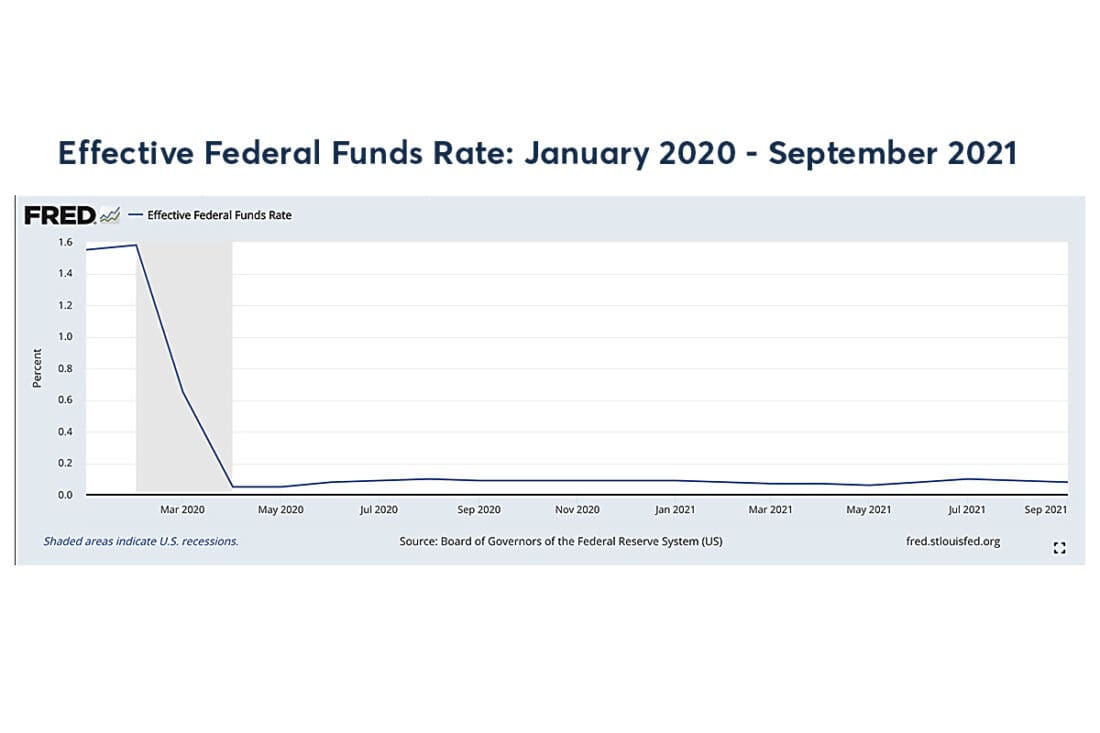

In response to the coronavirus pandemic, the Federal Reserve slashed interest rates to zero in March 2020 to help bolster growth. It also began its $120 billion in monthly asset purchases, a program known as quantitative easing (QE) that has roughly doubled the Fed’s balance sheet to about $8.5 trillion since the start of the pandemic.

Source: Board of Governors of the Federal Reserve System

QE helps by reducing long-term interest rates, thereby encouraging borrowing to help spur spending, and in turn, the economy. In doing so, the Fed essentially reduces the available supply of these bonds in the open market, forcing investors who want to own them to drive up prices. Driving up bond prices has the effect of lowering interest rates, which lowers the borrowing costs of households on their mortgages, or the costs of corporations to borrow by issuing debt.

As the Fed eases the pace and pares back the amount of these purchases, tapering begins with the ultimate goal of sending interest rates back to “normal.” Tapering can impact long-term interest rates, as this typically sends a signal to the markets that the Fed is shifting to a less accommodative policy stance in the future. The key is to understand that tapering does not mean the Fed stops purchasing assets, but it just reduces the pace of its balance sheet expansion. This is different than tightening, which means the Fed will no longer add assets to its balance sheet and will instead reduce the assets it holds by selling them.

Aside from interest rates, tapering could have an impact on the U.S. dollar. The trajectory of the U.S. dollar is important for investors as it impacts everything from commodity prices to corporate earnings. Higher yields make dollar-denominated assets more attractive to income seeking investors. Tapering is typically bullish for the dollar as it means a move toward tighter monetary policy. Since currencies normally appreciate when their domestic short-term rates rise, as the Fed continues to signal imminent tightening, markets are pricing in higher rates. This offers support to the dollar amid an already choppy risk environment that is a positive for the safe haven dollar. As mentioned above, if the Fed will be buying fewer debt assets, there would be fewer dollars in circulation.

The market is anticipating the beginning of the taper process could begin sometime in the fourth quarter of this year, possibly as soon as November. In addition, half of the Fed vice presidents project interest rates rising at some point in 2022. Fed Chairman Powell is anticipating the taper process could end around the middle of next year, as long as the recovery remains on track.

The Central Bank has insisted that they expect to keep the funds rate near zero until labor market conditions have reached levels consistent with their projections of maximum employment. We are nowhere near pre-pandemic unemployment levels (with 8.4 million unemployed persons in the U.S. now versus 5.7 million in February 2020). This could lead to concern over whether the Fed risks tightening monetary policy at a time when the economy might be significantly weaker than it already is today.

At the end of the day, if the Fed is priming the markets for a taper in the fourth quarter of 2021, we could be in for a period of extended volatility.

—

Originally Posted on October 11, 2021 – What Happens When the Fed Tapers?

© [2023] CME Group Inc. All rights reserved. This information is reproduced by permission of CME Group Inc. and its affiliates under license. CME Group Inc. and its affiliates accept no liability or responsibility for the information contained herein, including but not limited to the currency, accuracy and/or completeness of this information, and delays, interruptions, errors or omissions. This information is an unofficial copy and may not reflect the official and accurate version. For the definitive and up-to-date version of any of this information, please see cmegroup.com.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from CME Group and is being posted with its permission. The views expressed in this material are solely those of the author and/or CME Group and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!