- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted October 20, 2023 at 11:30 am

With all the attention given to the recent surge in Treasury (UST) yields, there has been an interesting by-product in the process: steepening yield curves. Remember when inverted yield curves were all the rage, and their historical track record was being highlighted as a sure sign of an eventual recession? Well, here we are, many months since the curves went into negative territory, but as yet, still no recession. Does that mean inverted curves have lost their way?

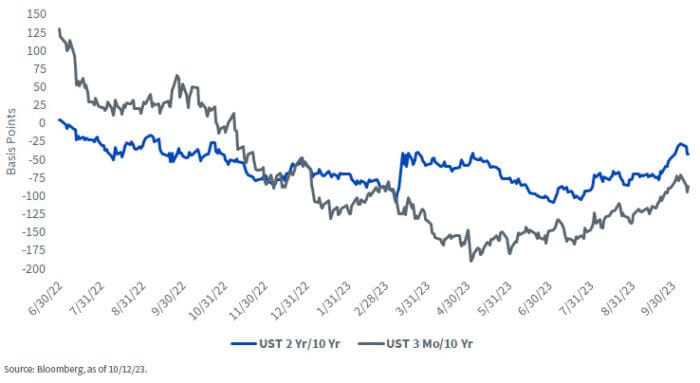

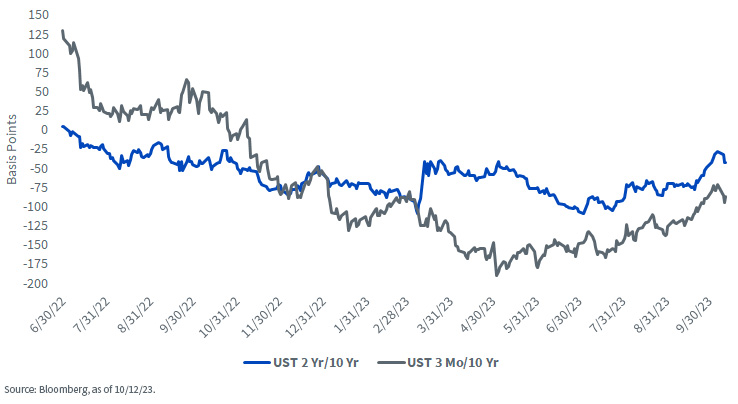

Let’s take a look at the two most widely followed yield constructs: UST 3mo/10yr and UST 2yr/10yr. Both these curves went into inverted, or negative, territory last year, but at different times. The 2yr/10yr spread moved below zero consistently at the end of June, while the 3mo/10yr differential hit the minus column during the fall of 2022.

Since then, both these constructs had been on a one-way trip into deeper and deeper negative territory. Indeed, the degree of inversion has been historical in nature, with the 2s/10s dropping to a nadir of -109 basis points (bps) in March and the 3mo/10yr plunging to its low point of -191 bps in May. While Treasury yields in general have been on the rise, the inverted nature of the curves was due primarily to the Fed’s Volcker-esque rate hikes. Indeed, the policy makers were pushing the Fed Funds target range up to levels not seen since the early 2000s, raising short-term rates such as the 3-month t-bill and the UST 2-Year note along with it. Meanwhile, the increase in the 10-Year yield could not keep pace…hence the deep inversions.

Now let’s fast forward to the present. While the Fed has been keeping the Fed Funds target range at 5.25%–5.50%, the 10-Year yield has surged. To provide some perspective, the UST 10-Year has experienced a roughly 100 bps increase since mid-July, with 60–70 bps of this rise occurring within the last six weeks. As a result, the aforementioned yield curves have steepened dramatically. For example, the 2s/10s inversion shrunk by 80 bps to only -28 bps following the jobs report, while the 3mo/10yr negative spread had re-steepened by an incredible 120 bps to -71 bps.

Back to the inverted yield curves’ forecast ability. A lot has been written about the impressive track record of inverted yield curves predicting past recessions. As a student of history, one needs to respect that. Interestingly, the U.S. economy did post back-to-back negative real GDP readings during Q1 and Q2 last year. However, that was prior to the curves discussed here going negative.

Where does that leave us, looking ahead? Well, as I mentioned in the opening, the U.S. economy has thus far avoided a downturn, and available data suggests a recession does not appear to be imminent either. So, just like a lot of other things lately, where the timing keeps getting pushed back, could a negative quarter or two of real GDP become a 2024 development? Even though Treasury yield curves have dramatically steepened, the two constructs highlighted in this blog post still remain inverted and past Fed tightening policies rarely achieved a soft landing. To quote Yogi Berra, “it ain’t over till it’s over.”

—

Originally Posted October 18, 2023 – Have Inverted Yield Curves Lost Their Way?

Investors should carefully consider the investment objectives, risks, charges and expenses of the Funds before investing. U.S. investors only: To obtain a prospectus containing this and other important information, please call 866.909.WISE (9473) or click here to view or download a prospectus online. Read the prospectus carefully before you invest. There are risks involved with investing, including the possible loss of principal. Past performance does not guarantee future results.

You cannot invest directly in an index.

Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, real estate, currency, fixed income and alternative investments include additional risks. Due to the investment strategy of certain Funds, they may make higher capital gain distributions than other ETFs. Please see prospectus for discussion of risks.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

Interactive Advisors offers two portfolios powered by WisdomTree: the WisdomTree Aggressive and WisdomTree Moderately Aggressive with Alts portfolios.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from WisdomTree U.S. and is being posted with its permission. The views expressed in this material are solely those of the author and/or WisdomTree U.S. and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!