- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 7, 2020 at 10:07 am

Logistics giant FedEx Corp (NYSE: FDX) priced US$3bn worth of investment-grade corporate bonds Friday, contributing to an unprecedented spike in primary market supply this past week.

A record weekly total of nearly US$118bn worth of fresh, high grade debt deals were sold in the past week, eclipsing the prior week’s tally of around US$110bn, amid solid demand from fixed-income investors and support from the Federal Reserve – and despite recent outflows from corporate funds.

For the week ending April 1, Refinitiv U.S. Lipper Fund Flows reported massive net outflows of almost US$8.5bn from high-grade corporate funds after an exit of around US$38bn in the prior week.

In fact, high quality credits have recently swung to large gains even amid investors’ withdrawals.

Nuveen analysts Bill Martin and John Miller observed that investment-grade corporate bonds had recently “rebounded dramatically,” with sentiment bolstered by news of the Fed’s purchase program.

Among the deals this past week, Memphis-headquartered FedEx priced US$3bn worth of ‘BBB’-rated bonds in three parts, amid ultra-low U.S. interest rates.

The company said it intends to use the net proceeds from the offering to repay US$1.5bn of borrowings under its 364-day credit facility, as well as US$136m of outstanding commercial paper.

Demand for the issuance was stellar, with its 5-, 10- and 30-year tranches having compressed by 30bps-40bps from initial price talk to arrive at final spreads of 350bps, 370bps and 410bps more than matched-maturity U.S. Treasuries, respectively.

The deal was co-lead managed by BofA Securities, Goldman Sachs, J.P. Morgan and Wells Fargo Securities.

FedEx’s issuance comes as its operating capabilities have been materially impaired by the deadly COVID-19 pandemic, spurring its fiscal third quarter of 2020 margins tighter, and more than halving its net income and earnings.

The company’s Q3’20 operating margin shrunk to 2.4% from 5.4% in the prior year period, while net income plunged to US$315m from US$739m and earnings per share plummeted to US$1.20 from US$2.80.

Given the uncertainties fueled by the coronavirus pandemic, FedEx CFO Alan Graf said that the company would be suspending its fiscal 2020 earnings guidance for its consolidated and segment results.

Graf added that to mitigate near-term headwinds and “position the company for future earnings growth, we are attacking costs throughout the company by managing capacity, retiring our oldest and least-efficient aircraft, integrating TNT Express, and lowering our residential delivery costs.”

FedEx had attributed the decline in its operating results to a slew of factors, including weaker global economic conditions, “higher self-insurance accruals, an unfavorable variable incentive compensation comparison, increased FedEx Ground costs from expanded service offerings, the loss of business from a large customer [Amazon (NASDAQ: AMZN)], a continuing mix shift to lower-yielding services and a more competitive pricing environment.”

In early March, the firm had also announced the replacement of CFO Alan Graf with treasurer Mike Lenz.

Graf, who is retiring, will continue to serve as the company’s chief financial officer until September 22, and will remain at FedEx as executive vice president and senior advisor through the end of 2020 to ensure a smooth transition.

Against this backdrop, Moody’s Investors Service, which assigned a lower-tier, investment-grade ‘Baa2’ credit rating to FedEx’s latest bond sale, noted that the company’s elevated financial leverage, is largely a consequence of debt-funded share repurchases in prior years, as well as a “substantial capital investment program, an increase in pension obligations and limited earnings growth.”

As of February 29, the firm’s debt/EBITDA was 3.8x, and Moody’s expects the level to increase “as economic conditions deteriorate”.

While liquidity – supported by a US$3.5bn revolver may be adequate – Moody’s noted that “free cash flow will likely remain negative as cash flow from operations softens while capital spending on aircraft, vehicles, facilities and automation continues to be elevated.”

FedEx held a cash balance of US$1.8bn as of February 29,2020, with around US$900m of that figure held overseas.

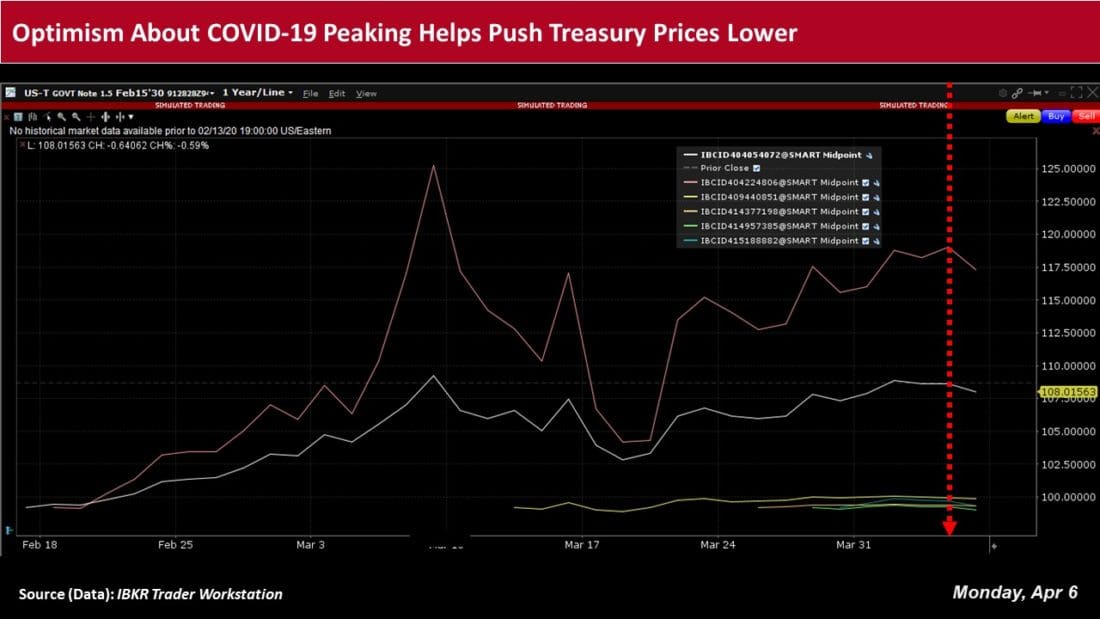

Meanwhile, cash spreads on high grade corporate bonds were roughly 7bps tighter intraday Monday, led by the communications (-10.8 bps) and health care (-8.0 bps) sectors, amid reports that the novel coronavirus outbreaks and related deaths may be reaching a crescendo.

The optimism had supported risk-taking, spurring U.S. stocks about 5.5% higher intraday and helped depress prices of U.S. Treasury securities across the curve.

Yields on the 10-year U.S. Treasury note and 30-year bond were last bid at around 0.663% and 1.261%, respectively.

While OAS on industrials also narrowed by around 6bps, some of FedEx’s shorter-dated notes remained wide.

The company’s 5.625% August 2022s were last around 75bps wider on the day at just south of 235bps more than comparable U.S. Treasuries; and its 4% January 2024s were last 21 bps wider at an OAS of 276 bps.

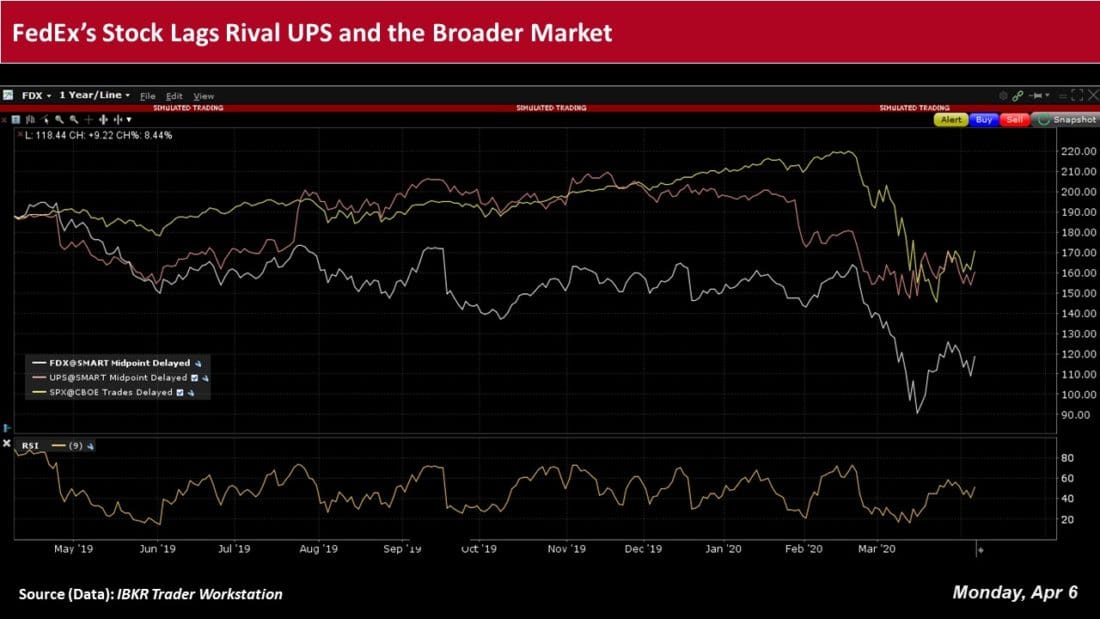

Year-to-date in 2020, FedEx’s shares have fallen around 22% to trade at around US$118.30 intraday Monday. Rival courier UPS (NYSE: UPS) has shed about 19.75% over the same period and was last bid at roughly US$94.

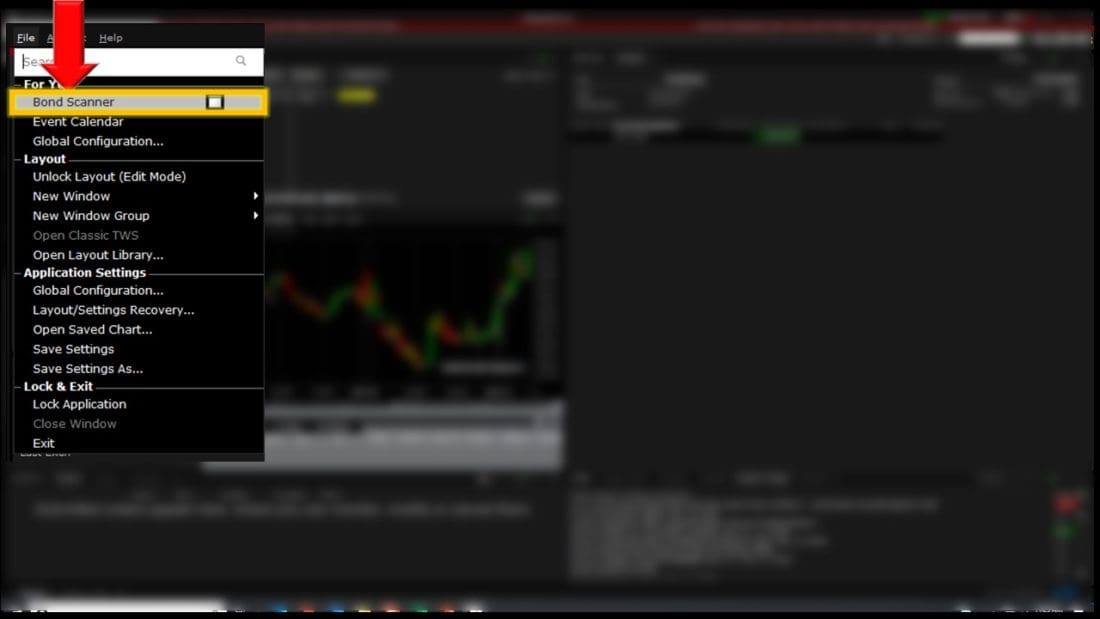

In the meantime, use the global bond scanner in the IBKR Trader Workstation to locate corporate bonds that are available to trade in the secondary market, along with U.S. Treasuries, municipal bonds, non-us sovereign debt and more.

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

The author does not hold any positions in the financial instruments referenced in the materials provided.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!