- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted October 1, 2021 at 11:25 am

Portfolio Managers Michael Keough and Brad Smith discuss why investors could benefit from taking an active approach to sustainable investments in the current investment environment for corporate bonds.

The world, and the world economy with it, is changing. Investors know this and have increasingly sought out sustainable investments. But, in our view, investing in sustainability is not only about helping to realize our values but also an opportunity for active managers to add value through their understanding of the economic disruption underway, their in-depth knowledge of industries and companies, and their experience in risk management. With subdued government bond yields and corporate bond spreads close to their historic lows, investors and investment managers should be taking advantage of all the tools and opportunities available to meet their return and risk targets, including the opportunities a transition to a sustainable global economy may provide.

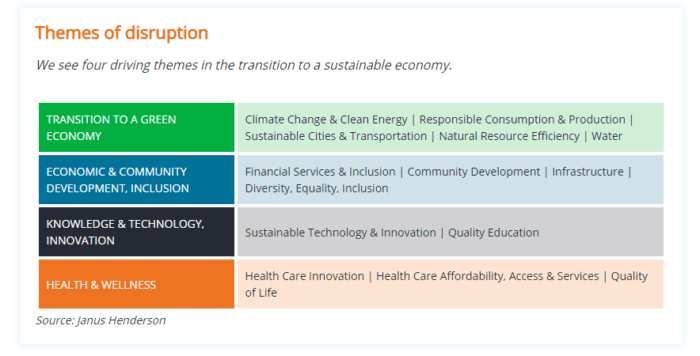

Throughout history, significant investment opportunities have arisen during times of transformational change. As recently as last year we saw the sudden changes wrought by COVID-19 and the transformational effect they had on everything from technology companies to oil prices to the housing market. In our view, the shift to a sustainable economy is a generational transformation that will create significant long-term investment opportunities.

This is not to suggest that the business cycle is no longer important, or that investors should ignore the current uncertainties around fiscal and monetary policy, or the challenges of meeting their income goals in a low-yield world. But these are largely cyclical issues while the move toward a more sustainable economy is a structural one.

We anticipate the transition to sustainability will be a driving force of economic change for years, and thus an ongoing opportunity to identify winners on the right side of disruption. Because the goal of active managers is to be proactive and extract the maximum benefit from change, they should be well positioned to find the opportunities these changes provide, while also identifying companies at risk of not keeping pace.

Passive investing, whether in corporate bonds or sustainable corporate bonds, does have its advantages. The corporate bond benchmark has well-known risk and reward characteristics, making it a comfortable solution for broad asset allocation decisions. But benchmarks are slow to reflect change. They are not designed to direct investors to where social and environmental change may take us.

Much like corporate bond benchmarks are more reflective of the past than predictive of the future, so are conventional measures of environmental, social and governance (ESG) factors. Many of the ESG ratings given to companies by third-party providers are based on past behavior, not expectations for future change. Active managers should be, and usually are, more forward looking. Regardless of their past performance, which companies are planning for change? How successful are they likely to be?

For us, the heart of sustainable investing is the simple idea that companies are more likely to succeed and deliver strong returns over the long term if they create value for all of their stakeholders, including customers, employees and society more widely. Active managers, particularly those with extensive research capabilities, can consider third-party ESG ratings as one input in a robust proprietary analysis that views a company not only within the context of broader disruption themes, but also within the context of the change in a company’s particular industry, even its related supply chains. These tools are integral to identifying those companies that have or are working toward a “future proofed,” sustainable business model. Conversely, analysis informed by sustainable considerations can uncover companies that cannot or will not change and therefore perhaps avoid the consequential underperformance.

Fundamental, bottom-up, active management necessarily engages with corporate leaders. Regular interaction with companies is crucial to better understand not only the extent of their current deficiencies, but also their ability and willingness to transition to a more sustainable business model. This engagement helps promote transparency and can encourage the company to transition to more sustainable business practices. Ideally, engagement creates a virtuous circle where the influence results in better sustainability practices, that lower the cost of capital, encouraging the company’s competition to do the same and accelerating the overall transformation to sustainability.

Engagement with companies can also help distinguish between those committed to change and those that may be greenwashing, or seeking to portray their products and services as more sustainable than they really are. To be fair, achieving sustainability is a complex process that takes time. And investing in sustainable companies is equally complex, precisely because it is challenging to meaningfully measure sustainability.

The consideration of ESG factors is not simply an evaluation of a company’s products or services, but also its behavior, conduct, supply chain and general business operations. In addition to understanding a company’s past behavior, how it deals with controversies and its latest ESG disclosure, analyzing the company’s strategy and evaluating whether it is executing on it is essential. Forward-looking proprietary analysis and active engagement are critical steps in making sound investments and promoting transparency and honesty. Companies have and will greenwash to save time, money, or both. Benchmark indices may even include companies that manage to meet a minimum ESG requirement, regardless of the company’s intentions or future plans. It is the job of an active manager to identify companies that may only look sustainable, and to avoid them.

Prudent active asset managers have traditionally viewed it as their responsibility to identify, quantify and mitigate risk. In this respect, sustainable investing is no different than traditional investing. And, in our view, analyzing a company through a sustainable lens helps not only to improve a portfolio’s returns but also to mitigate its risks, thus maximizing risk-adjusted returns.

Active corporate bond managers have long known that investing in a company experiencing distress can result in losses that are a multiple of the reward earned for picking companies that are doing “well.” For this reason, it has traditionally been more critical that active managers “avoid the losers” than “pick the winners,” but in sustainable investing, active management can help change this dynamic. It has the potential to reveal material issues in a company’s transition early on through consistent engagement practices and mitigate related losses. And, because disruption creates opportunities, there may be more opportunities for companies on the leading edge of sustainability to rapidly gain market share, improve their credit profiles and ratings and generate outsized returns.

An active approach to sustainable investment also has the potential to help reduce a portfolio’s overall risk profile by allowing for greater diversity of risk factors. Insofar as passive investing requires the replication of an established benchmark, it has the potential to create concentrations in company, industry or sector exposures that may be undesirable or unable to keep pace with change. This may or may not be advantageous at various times, but it mathematically decreases a portfolio’s diversity. In some industries or sectors this could be significant, whether due to a dearth of sustainable investment options, or a concentration in a handful of names.

We believe corporate bonds have and will play a critical role in a diversified bond portfolio, whether passively held or actively managed. But we think a process founded in robust research and proprietary ESG analysis that includes an active evaluation of a company’s path to sustainability should create the potential to both capture the upside in transformational change and help avoid downside risk as ESG laggards languish.

While we believe the challenges of the current environment require an active approach to managing risks and identifying opportunities, it is also our belief that investing with a sustainable lens is an opportunity to influence positive change. We expect the bond market, given its breadth, to play a critical role in financing the transition to a sustainable global economy and progressing various E, S and G issues. But it is active management and proactive engagement with investee companies that we think are best suited to make a difference. The engagement that active managers provide can help investors as well as consumers by demanding greater accountability and transparency from companies. In our view, an active sustainability analysis of corporate bonds does not just present the potential for returns that beat a benchmark or more active risk management, but the opportunity to focus investments in a way that can help the world transition toward a better future.

Glossary

ESG: Environmental, social and governance are three key criteria used to evaluate a company’s ethical impact and sustainable practices.

Fiscal policy: Government policy relating to setting tax rates and spending levels. It is separate from monetary policy, which is typically set by a central bank. Fiscal austerity refers to raising taxes and/or cutting spending in an attempt to reduce government debt. Fiscal expansion (or ‘stimulus’) refers to an increase in government spending and/or a reduction in taxes.

Monetary policy: The policies of a central bank, aimed at influencing the level of inflation and growth in an economy. It includes controlling interest rates and the supply of money. Monetary stimulus refers to a central bank increasing the supply of money and lowering borrowing costs. Monetary tightening refers to central bank activity aimed at curbing inflation and slowing down growth in the economy by raising interest rates and reducing the supply of money.

Spread/credit spread: The difference in yield between securities with similar maturity but different credit quality. Widening spreads generally indicate deteriorating creditworthiness of corporate borrowers, and narrowing indicate improving.

—

Originally Posted in September 2021 – Looking to Sustainability for Opportunity

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

High-yield or “junk” bonds involve a greater risk of default and price volatility and can experience sudden and sharp price swings.

Actively managed portfolios may fail to produce the intended results. No investment strategy can ensure a profit or eliminate the risk of loss.

When valuations fall and market and economic conditions change it is possible for both actively and passively managed investments to lose value.

Environmental, Social and Governance (ESG) or sustainable investing considers factors beyond traditional financial analysis. This may limit available investments and cause performance and exposures to differ from, and potentially be more concentrated in certain areas than, the broader market.

Credit Spread is the difference in yield between securities with similar maturity but different credit quality. Widening spreads generally indicate deteriorating creditworthiness of corporate borrowers, and narrowing indicate improving.

ETFs distributed by ALPS Distributors, Inc. ALPS is not affiliated with Janus Henderson or any of its subsidiaries.

Janus Henderson Group plc ©

The opinions and views expressed are as of the date published and are subject to change without notice. They are for information purposes only and should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation to buy, sell or hold any security, investment strategy or market sector. No forecasts can be guaranteed. Opinions and examples are meant as an illustration of broader themes and are not an indication of trading intent. It is not intended to indicate or imply that any illustration/example mentioned is now or was ever held in any portfolio. Janus Henderson Group plc through its subsidiaries may manage investment products with a financial interest in securities mentioned herein and any comments should not be construed as a reflection on the past or future profitability. There is no guarantee that the information supplied is accurate, complete, or timely, nor are there any warranties with regards to the results obtained from its use. Past performance is no guarantee of future results. Investing involves risk, including the possible loss of principal and fluctuation of value.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Janus Henderson and is being posted with its permission. The views expressed in this material are solely those of the author and/or Janus Henderson and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The information in this material is provided for informational purposes only and does not constitute tax advice and cannot be used by the recipient or any other taxpayer to avoid penalties under any federal, state, local or other tax statutes or regulations, or to resolve any tax issue.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!