- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted October 2, 2025 at 10:00 am

The energy sector is leaving investors unimpressed. YTD the American Energy Independence Index (AEITR) is +5% and seems to be marking time. The S&P500, increasingly dominated by tech and AI exposure, is +13%. Long-time clients, having enjoyed several strong years, hope the better days will soon return. More recent investors demand to know what’s gone wrong.

Time period matters. Roll the start date back three months, and the trailing one-year return for the S&P500 is +17% and the midstream sector is +19%. 4Q24 makes a big difference.

Operating performance is beating sentiment. 2Q earnings contained few surprises and mostly confirmed the positive trend for cash flow growth. More recently, Hess Midstream revised their guidance lower but the outlook for crude, where Hess operates, is weaker than for gas. Upstream capex is declining because of soft oil prices (see The Energetic Outlook For Energy) while midstream capex is increasing to meet growing gas demand for data centers and LNG exports.

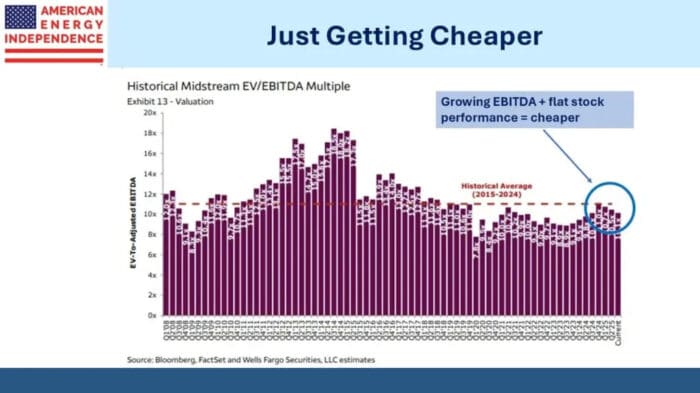

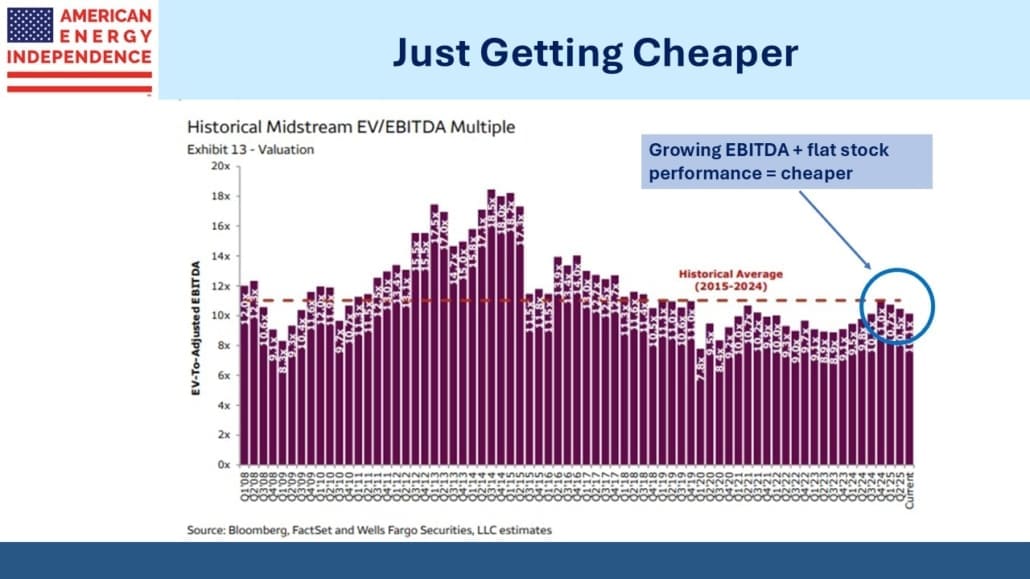

The contrast between moribund price performance and dynamic operating results is demonstrated by the Wells Fargo EV/EBITDA chart. The midstream sector has become cheaper, having pulled back almost halfway to the lows of late 2023, from which it delivered last year’s +45% total return. The problem, if a trailing one-year return of 19% deserves that characterization, is more with overly cautious investors than with how the companies are doing.

Modest price performance with growing EBITDA has left the sector more attractive than it’s been all year.

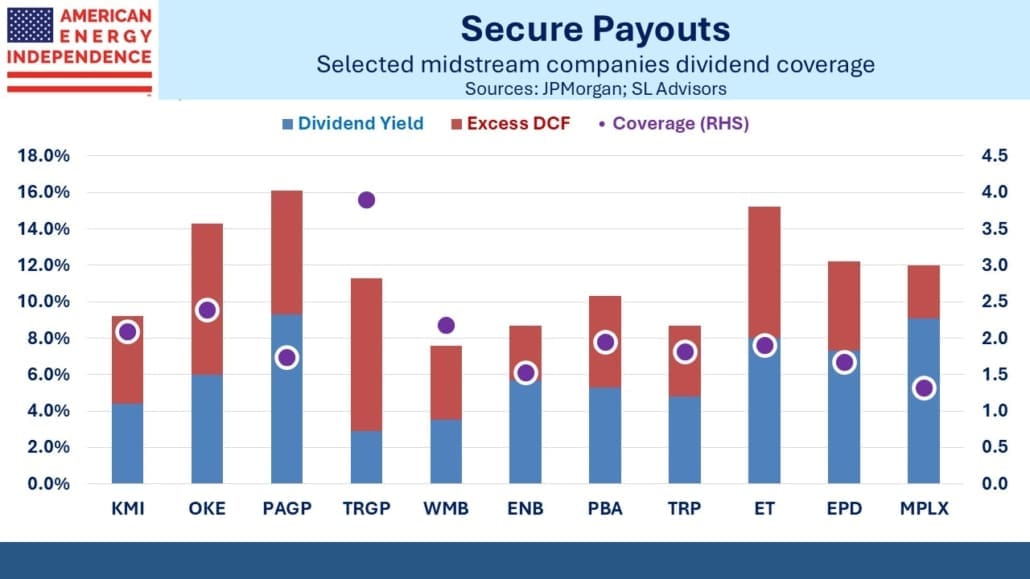

Leverage continues to drift lower with a median Debt:EBITDA of 3.5X according to JPMorgan, who also sees dividends growing at 5-7% next year. Distributable Cash Flow coverage ratios for the large cap names listed are at a median of 1.9X. We’ve omitted the LNG exporters Cheniere and Venture Global because they pay small dividends so would distort this metric higher.

The demand picture for natural gas remains robust, with hundreds of $BNs being invested in data centers that will need reliable electricity and LNG exports growing strongly. Below average sea temperatures in the Pacific near Peru meet the criterion for La Nina, meaning the odds of a warmer than average US winter are low. Natural gas prices rose accordingly on this news.

Although we’re rarely accused of insufficient enthusiasm towards pipelines, it does seem that for those underweight the sector, which would be most investors, current valuations offer an opportunity to rectify.

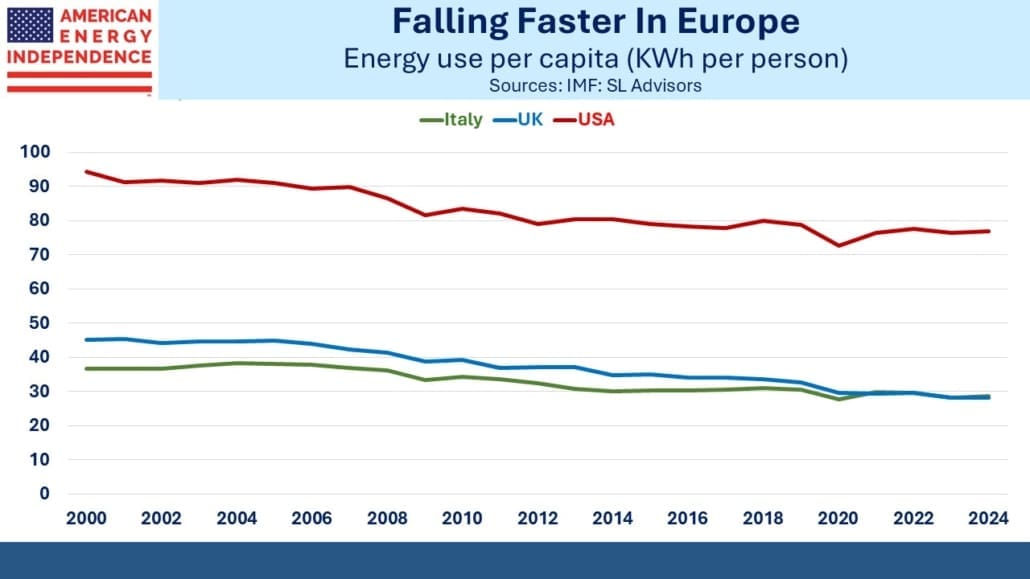

My wife and I were in Italy recently. When we travel, I’m always interested to learn more about how other countries use energy. Americans use more energy per capita than any other developed country except Canada, where the winters are long and cold.

The typical Italian uses only 37% as much energy as an American. There are many factors for this – Europeans rely less on air conditioning than we do in North America. They like to open the windows, since summer heat rarely matches the US.

The cars are smaller, with two-seater and even one-seater models that would fit in the back of a Ford F150. Hotels often require you to put your key in a slot to activate the room’s power, ensuring no wasted electricity when guests are out.

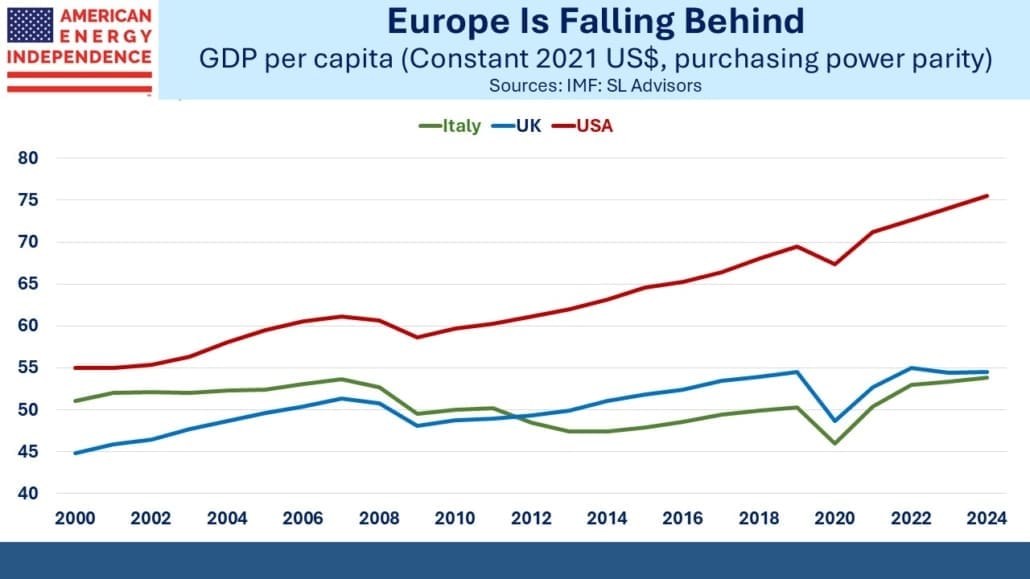

The EU is a leader in adopting policies to reduce greenhouse gases, which has led to some of the world’s highest electricity prices and a slow de-industrialization of the region. Living standards and energy consumption are symbiotically linked. Italian GDP per capita is only 71% of the US, down from 95% twenty-five years ago. Per capita energy consumption has declined 0.8% annually over the past decade, faster than the US at 0.5%.

The setting for Frances Mayes’ Under the Tuscan Sun is populated by many who care little for such analysis. It’s true that sharing a bottle of Chianti in a picturesque village overlooking rolling vineyards can generate thoughts beyond GDP. But to live like an American in Italy you need to have made your money elsewhere.

The inescapable conclusion is that relative living standards in much of Europe are sliding along with energy use. One can debate cause versus effect, but not the outcome. One of the saddest charts I ever look at is the ratio of UK to US GDP per capita, which has dropped quite sharply in the past decade. Brexit, no productivity growth and widespread use of expensive windpower have all contributed. But it does pain me to see my old country making bad choices while also confirming my 1982 decision to emigrate.

Trump’s jibe at the UN that European countries were “going to hell” in part because of energy policies was hyperbolic as usual but directionally correct. He’s wrong in denying the risks in elevated atmospheric CO2, but right in criticizing the belief that the world will run on renewables. It won’t. Fortunately, in America, we know that.

—

Originally Posted September 28, 2025 – Getting Cheaper By Moving Sideways

Please go to following link for important legal disclosures: https://sl-advisors.com/legal-disclosure

SL Advisors is invested in all the components of the American Energy Independence Index via the ETF that seeks to track its performance.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from SL Advisors and is being posted with its permission. The views expressed in this material are solely those of the author and/or SL Advisors and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Alternative investments can be highly illiquid, are speculative and may not be suitable for all investors. Investing in Alternative investments is only intended for experienced and sophisticated investors who have a high risk tolerance. Investors should carefully review and consider potential risks before investing. Significant risks may include but are not limited to the loss of all or a portion of an investment due to leverage; lack of liquidity; volatility of returns; restrictions on transferring of interests in a fund; lower diversification; complex tax structures; reduced regulation and higher fees.

Related Articles

")

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!