- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted November 16, 2022 at 6:16 pm

“You don’t find out who’s been swimming naked until the tide goes out” – Warren Buffett

“It’s one big nude-o-rama” – George Costanza

This has been one heck of a week in the crypto space. In the wake of FTX’s implosion, we have a report this morning that Genesis would be pausing withdrawals. This comes after various news reports that BlockFi may be preparing for a bankruptcy filing. The monetary tide has been ebbing steadily, and we now see that the cryptocurrency section of the beach was chock full of financial skinny-dippers.

It is said that a rising tide lifts all boats, and that certainly is the case when we think broadly about financial assets. The tide of course is money, but rather than being driven by the gravitational pull of the moon over the oceans, financial tides are caused largely by the influence of central bankers. Central bankers are obviously far less predictable than the moon’s orbit around the earth. Yet the reaction to rising financial tides remains habitual. Mr. Buffett’s famous quote (at the 1:50 mark in this link), from the 1994 Berkshire Hathaway Annual Meeting, refers to the tendency of reinsurers to pile into risky bond bets en masse. The product is different, but human nature – at least when it applies to financial markets – remains all too constant.

Would cryptos have become mainstream, let alone a mania, if we had positive real interest rates? I think not. Zero nominal and negative real rates encouraged all sorts of speculative excesses. This was just the most extreme.

Easy money skews the balance between risk and return. When rates are low, investors need to take greater risks to generate returns. When rates are low, bond investors become incentivized to finance weaker credits and equity investors hew toward speculative rather than defensive names. When rates become exceptionally low, speculation can take on a life of its own. The popularity of cryptocurrencies was merely one element of the speculative fever that raged during 2020-21. Meme stock mania and the explosion in short-term call options trading stemmed from the same factors. The ultimate form of easy money – negative real interest rates – spurred a speculative wave.

The difference with cryptocurrency is that it is a relatively new financial innovation. It simply was not a mainstream product until recently. For better or worse, we’ve become relatively accustomed to booms and busts in stocks, bonds and derivatives. They’ve been pre-disastered, so to speak. Industry executives and regulators have a framework – sometimes imperfect – for how to deal with crises in these asset classes. Cryptos have not evolved that framework. Their freewheeling nature and lack of regulatory oversight were key selling points when they were rising. But they left a nascent industry vulnerable when they fell. Even now, it is premature to think that we have seen the full crypto fallout.

I’ve long asserted that every new financial innovation meets its day of reckoning. Some, like mortgage-backed securities, prove worthy and the industry adapts to make them more resilient. Others, like portfolio insurance, prove to be faddish, and fall by the wayside. (I wonder if LDI will suffer a similar fate). It is too early to know which will be the fate of cryptocurrency. Without a real-world use case, I suspect that cryptos could prove to be a historical curiosity even as blockchain evolves into a pervasive technology.

For now, broader markets can largely ignore the crypto dominos. The sequential failures are painful to those involved but had little spillover because crypto had not yet reached broad adoption. Bottom line, the total market capitalization of all cryptocurrencies is dwarfed by Apple’s (AAPL) stock alone. Those of us with little to no exposure can treat this as a sideshow – at least until the financial tides recede even further and potentially reveal even more naked swimmers.

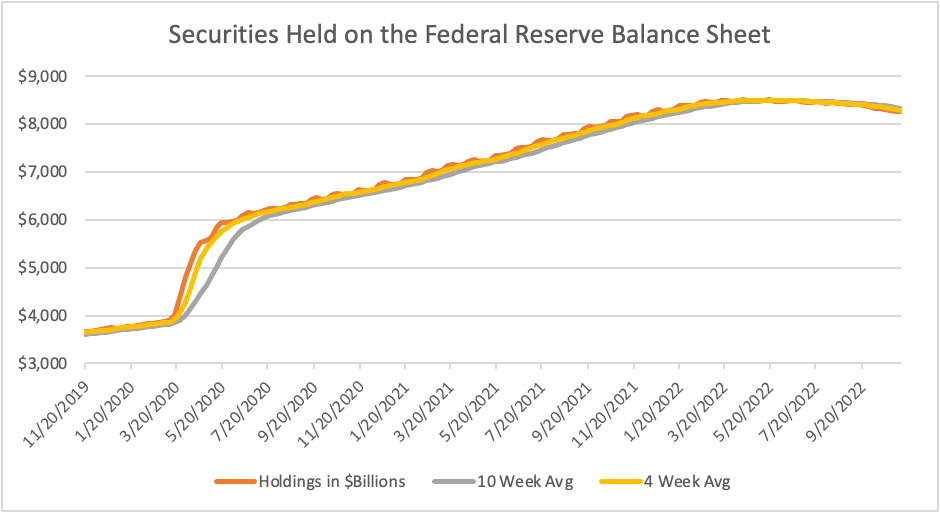

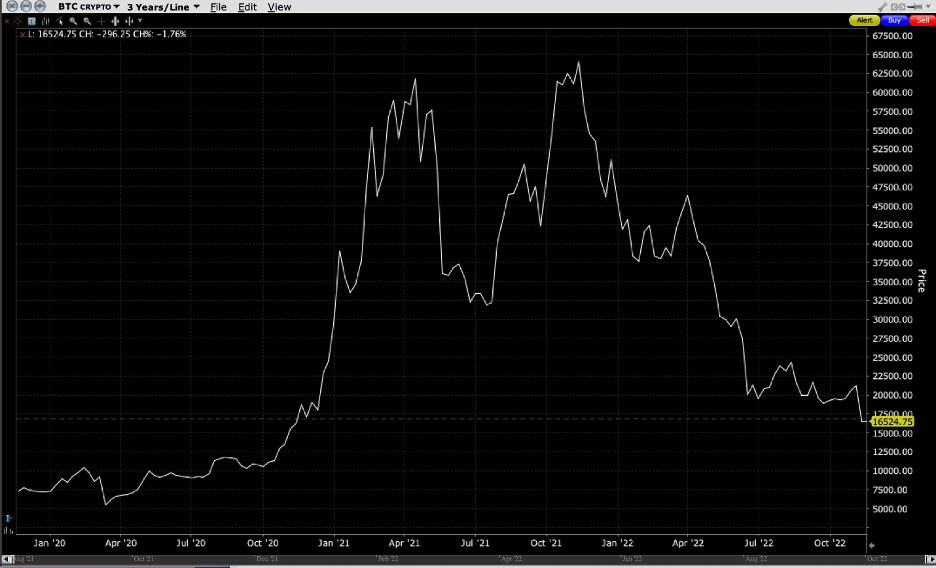

For reference, here are some financial “tide charts”:

Source: Federal Reserve H.4.1 Releases, Interactive Brokers

Fed Funds Target Rate, Upper Bound, 3-Year Chart

Source: Bloomberg

Bitcoin, 3-Year Chart

Source: Interactive Brokers

New to Interactive Brokers?

Open AccountAlready an Interactive Brokers Client?

Request Trading PermissionThe analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

TRADING IN BITCOIN FUTURES IS ESPECIALLY RISKY AND IS ONLY FOR CLIENTS WITH A HIGH RISK TOLERANCE AND THE FINANCIAL ABILITY TO SUSTAIN LOSSES. More information about the risk of trading Bitcoin products can be found on the IBKR website. If you're new to bitcoin, or futures in general, see Introduction to Bitcoin Futures.

Options involve risk and are not suitable for all investors. For information on the uses and risks of options, you can obtain a copy of the Options Clearing Corporation risk disclosure document titled Characteristics and Risks of Standardized Options by going to the following link ibkr.com/occ. Multiple leg strategies, including spreads, will incur multiple transaction costs.

TRADING IN BITCOIN FUTURES IS ESPECIALLY RISKY AND IS ONLY FOR CLIENTS WITH A HIGH RISK TOLERANCE AND THE FINANCIAL ABILITY TO SUSTAIN LOSSES. More information about the risk of trading Bitcoin products can be found on the IBKR website. If you're new to bitcoin, or futures in general, see Introduction to Bitcoin Futures.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!