- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted June 3, 2025 at 12:40 pm

Stocks are jolting north today as investors are paying no mind to the OECD’s downbeat economic outlook and choosing to focus on this morning’s stronger-than-anticipated JOLTS print for April. The report also featured a favorable revision to the preceding month and is bolstering economic growth expectations. Turning to trade, US Commerce Secretary Howard Lutnick drove optimism about nearing a cross-border deal with India, the world’s fourth-largest economy. Market participants are reacting to the mix of positive news favorably, as labor conditions remain solid amidst continued progress on White House negotiations, which collectively bode well for corporate earnings prospects and an augmented economic expansion. Traders are responding by purchasing equities in most sectors and adding to their exposures of the greenback, bitcoin and forecast contracts. Conversely, folks are trimming their holdings of commodity futures ex crude oil, Treasuries across the curve and volatility protection instruments.

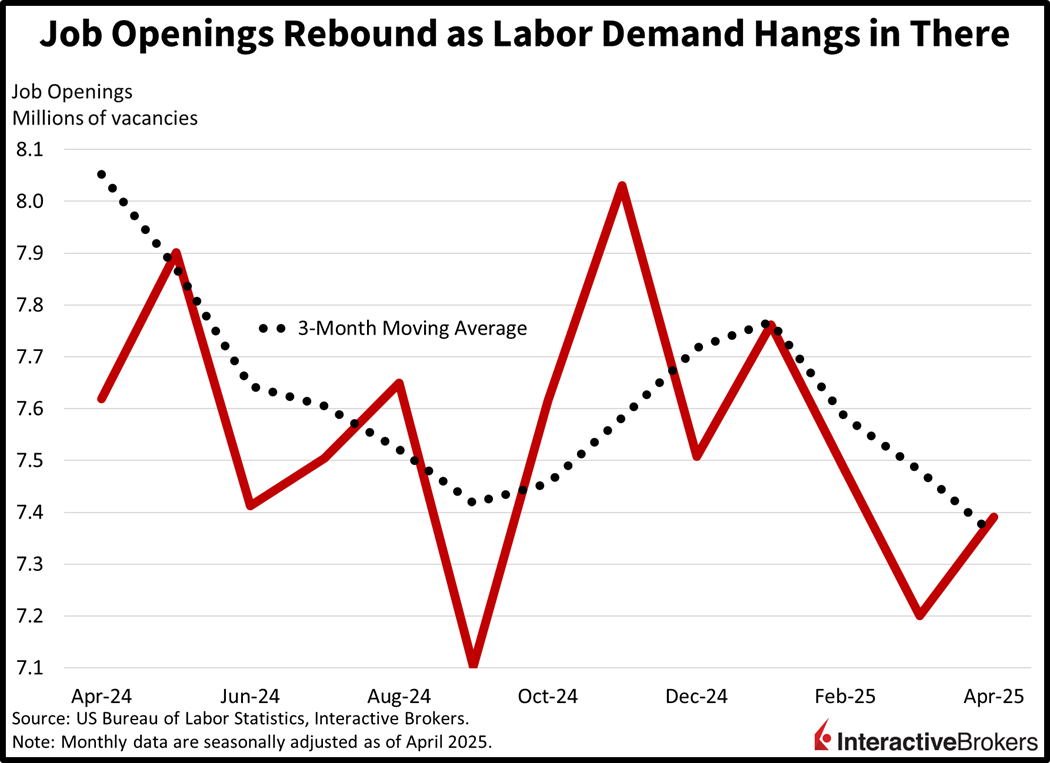

Demand for workers increased in April as help-wanted postings rebounded to start the second quarter. Job openings jumped to 7.391 million, exceeding the 7.1 million consensus estimate and the upwardly revised 7.2 million from March. Gains were driven by the professional/business services and health care/social assistance sectors, which expanded for-hire signs by 171,000 and 102,000. Meanwhile the accommodation/food services and state/local education categories were the greatest laggards, as vacancies declined by 135,000 and 51,000.

Factory orders contracted in April as broad-based weakness across the durable and non-durable categories weighed on the headline. Transactions dropped 3.7% month over month (m/m), worse than the -3% expected and offsetting March’s 3.4% gain. A sharp decline in aircraft revenues drove the durable segment down 6.3% m/m, while nondurables experienced a more modest 0.9% m/m subtraction.

Trading action in the Treasury complex remained contained despite today’s hotter-than-projected JOLTS report. Fixed income is undervalued here in my view unless you expect a sharp rise in inflation, which we haven’t seen yet although rising angst about price pressures has been prevalent in consumer surveys and earnings calls. Meanwhile, the latest reading on the headline PCE gauge was 2.1%, and coupons in the complex are at least 184 basis points (bps) higher, with the 3-year changing hands at 3.94%. In the past 25 years, real rates of 200 bps have signaled opportunities to buy bonds, as they’ve tended to express selling exhaustion and heavy economic restriction. But of course, this time is different since deficit and sovereign debt concerns are increasingly top of mind than ever. Still, I think the trade is for lower yields from here, as inflation cooperates, and term premiums settle in on better-than-expected fiscal revenue collections. Finally, technicals have offered bullish support, with investors feverishly defending critical levels across maturities.

Euro area inflation was flat in May on a m/m basis after increasing 0.6% m/m in April, according to the Consumer Price Index. The year over year (y/y) measurement, furthermore, climbed 1.9%, easing from 2.2% in April and arriving lower than the consensus forecast of 2%. Similarly, the Core CPI, which strips out items with more volatile prices declined from 2.7% y/y April to 2.3% last month and fell below the 2.4% estimate. During the month, energy and services saw costs decline 1.2% and 0.1% m/m, while the food/alcohol/tobacco and industrial goods categories experienced charge increases of 0.5% and 0.1%.

Minutes from the Royal Bank of Australia’s May meeting reveal that the bank is considering aggressive cuts in short term rates if the global trade disagreements weigh on conditions meaningfully. At the May gathering, policymakers proposed a jumbo 50-bp cut, but agreed to make a more common 25-bp reduction, citing a lack of indicators pointing to the economy weakening as a result of geopolitical tensions. Additionally, at a time of heightened tariff uncertainty, the bank wants to maintain a policy that is predictable. Australia is suffering from a housing shortage, so a lower key interest rate, while potentially providing relief to mortgage seekers, could also fuel price pressures for residential real estate.

China’s goods producing activity in May contracted at the fastest pace since September 2022, according to the Caixin-sponsored Manufacturing Purchasing Managers’ Index. The index dropped from 50.4 in April to 48.3 in May, considerably below the contraction-expansion threshold of 50 and the consensus estimate of 50.7. Weak foreign demand had the largest adverse impact on the headline. Within the gauge, both production and new orders reversed from expansion to contraction, but business sentiment improved.

The weak PMI print wasn’t the only disappointing news this morning with China’s Ministry of Culture and Tourism reporting that consumer spending during the three-day Dragon Boat Festival, on a per domestic trip basis, sank 2.2% y/y. The tight purse strings reflect low household sentiment, a result, in part, of exporters reducing payrolls due to US tariffs on Chinese products. At the same time, China has been trying to boost consumption with rebates for appliance upgrades and other incentives.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!