- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted July 15, 2026 at 1:34 pm

The second consecutive trading session featuring a much lighter-than-expected inflation report alongside cheaper oil for the first time this week has stocks and Treasuries extending their rebounds following Monday’s deep losses. Markets have responded to the friendlier cost dynamics by pushing back the Fed’s initial 2026 hike to October, although September’s odds of a 25-basis point increase are slightly below a coin-flip’s. The dovish tilt occurs as central bank head Chair Warsh has warned to not declare victory on the price-side of the organization’s mandate against the backdrop of the pair of misses signaling sharp decelerations in charge pressures, as he remains firmly committed to reaching the institution’s 2% objective. Still, the greenback is depreciating as the yield curve descends in bull-steepening fashion led by the shorter tenors, adjusting to a rising likelihood of steady monetary policy in the next few months. Equities are performing well, partially a result of strong earnings even as tech is suffering from a semiconductor selloff, especially apparent in memory chipmakers, which has the Nasdaq 100 down almost 1% at the same time that 6 of the Magnificent 7 names appreciate strongly, with 5 of them up over 3%. There’s broadening movement under the hood as 7 of the 11 sectors advance along with the Russell 2000, Dow Jones Industrial and S&P 500 indices. The risk-on attitudes have participants buying cryptocurrencies and prediction contracts; however, they are unloading hedges as volatility protection instruments see reduced premiums. Commodities are retreating across the board even as financial conditions loosen, the dollar weakens and US-Iran hostilities remain tense. WTI crude is plunging from a potential pivotal resistance level of $80 per barrel.

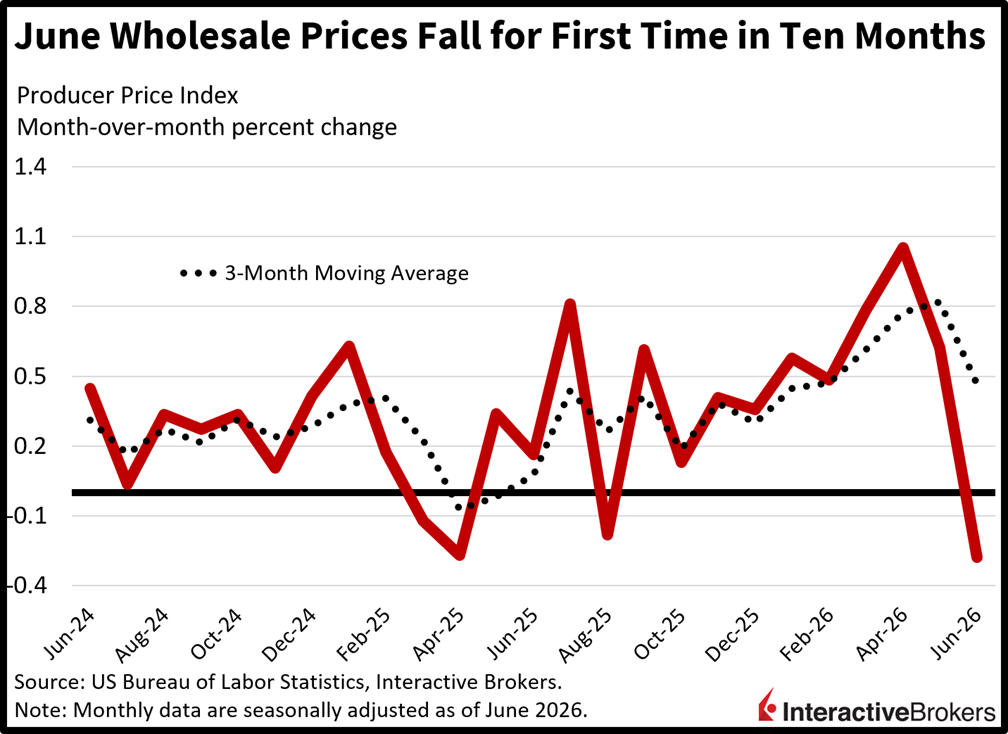

The Producer Price Index (PPI) retreated for the first time in ten months in June, as cratering fuel costs drove a massive deceleration in wholesale charge pressures. The headline sank 0.3% month over month (m/m) and rose 5.5% year over year (y/y), well below the median estimates of 0% and 6.2% as well as May’s 0.6% and 6%. The energy, food and transportation/warehousing services components led the way south, with those segments becoming 6.4%, 0.6% and 0.1% less expensive m/m. Conversely, however, trade services, goods excluding food and energy and other services experienced increases of 0.4%, 0.2% and 0.1%.

Bonds have several paths to significant appreciation from here, with an anemic housing sector and overall disinflationary trends serving as prime reasons for owning duration. Elevated rates, lofty valuations and restrictive immigration have hampered activity and pricing power in the pivotal residential real estate space that comprises the heaviest portion of the inflation picture. Indeed, rent growth and valuation increases have slowed to a halt, and are effectively reversing into the negative in many areas of the country, including the historically speculative sunbelt. This huge and ongoing cost alleviation in shelter may coincide with a possible reduction in energy costs, which could push headline price forces down to the mid 2s by year-end, and place potential cuts back on the Fed’s curve for 2027, offering strong capital gains for owners of long-term fixed-income assets.

Weak domestic demand more than offset the impact of soaring exports on China’s economy during the second quarter, which caused gross domestic product (GDP) to climb only 4.3% y/y, which missed the country’s target range of 4.5% to 5%, according to the National Bureau of Statistics. Economists had anticipated a 4.5% expansion following the 5% growth in the preceding period. On a quarter-over-quarter basis, furthermore, GDP decelerated from 1.3% in the first three months of the year to only 0.9% higher, but it matched the economist consensus estimate. In a press conference, Deputy Head of the NBS Mao Shengyong said external factors as well as temporary domestic issues, such as a slowdown in coal mining, weighed on GDP. He maintained that the economy’s fundamentals haven’t weakened. Yet, economic data covering June were mixed with unemployment falling, industrial production increasing and retail sales exceeding expectations. Less encouraging was declining house prices, weak fixed asset investment and loan growth falling below expectations.

China’s unemployment rate fell from 5.1% in May to 5% last month, a better reading than the economist consensus expectation for an unchanged statistic.

Retail sales, furthermore, climbed 1% y/y in June, exceeding the economist consensus estimate for a 0.1% decline following May’s 0.6% contraction. Industry also appears to have perked up with June production 5.3% higher than in the year-ago period, which surpassed both the economist consensus estimate of 4.7% and May’s 4.5% gain.

Home prices in China continued their long decline, sinking 3.3% y/y in June after a 3.5% drop in the preceding month. China’s aggressive construction of homes along with weak domestic demand has caused prices of residential property to fall every month since April 2022 with only one exception, which involved no price change in June 2023. Fixed asset investment also disappointed, dropping 5.7% y/y, a worse showing than the economist consensus estimate for a 5% slip following the 4.1% contraction in May. New loan issuance also disappointed. At 1.61 trillion yuan, or roughly $237.75 billion, the total value of debt initiated in June in new yuan loans substantially missed the economist consensus estimate of 1.91 trillion yuan, although it climbed from 520 billion yuan in May.

South Korea’s $39.09 billion trade surplus missed the consensus forecast for $36.15 billion but was up significantly from $27 billion in May. On a y/y basis, imports were up 30%, roughly unchanged from the 30.1% print in May. Exports grew impressively, jumping 70.7% y/y. While the metric missed the economist estimate for a 70.9% hike, it was a considerable acceleration from 20.7% in May. Exports benefited from AI stoking demand for the country’s information and communications technology. The value of shipments of products within the category soared 160.4% y/y in June, reaching a monthly high of $527.29 billion.

The Bank of Canada (BoC) announced this morning that it decided to hold its current key interest rate at 2.25%. The outcome of the central bank’s meeting was widely anticipated by analysts. In a press release, the BoC said the economy, which recently hit a technical recession, or two consecutive quarters of declining GDP, is likely to rebound. In addition to showing signs of improvement, growth is picking up. The BoC also believes inflation will gradually ease.

Sales by Canadian wholesalers were flat in May when compared to April, according to Statistics Canada. The metric slowed considerably from 1.4% in April but still outpaced expectations for activity to sink 0.7%. Manufacturing sales, furthermore, slowed from the 3.9% m/m gain in April to 1.3% in May but exceeded expectations for growth to sink

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures, event contracts, and forecast contracts are not suitable for all investors. Before trading these products, please read the CFTC Risk Disclosure. For a copy, visit our Warnings and Disclosures Page.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!