- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted March 2, 2026 at 12:56 pm

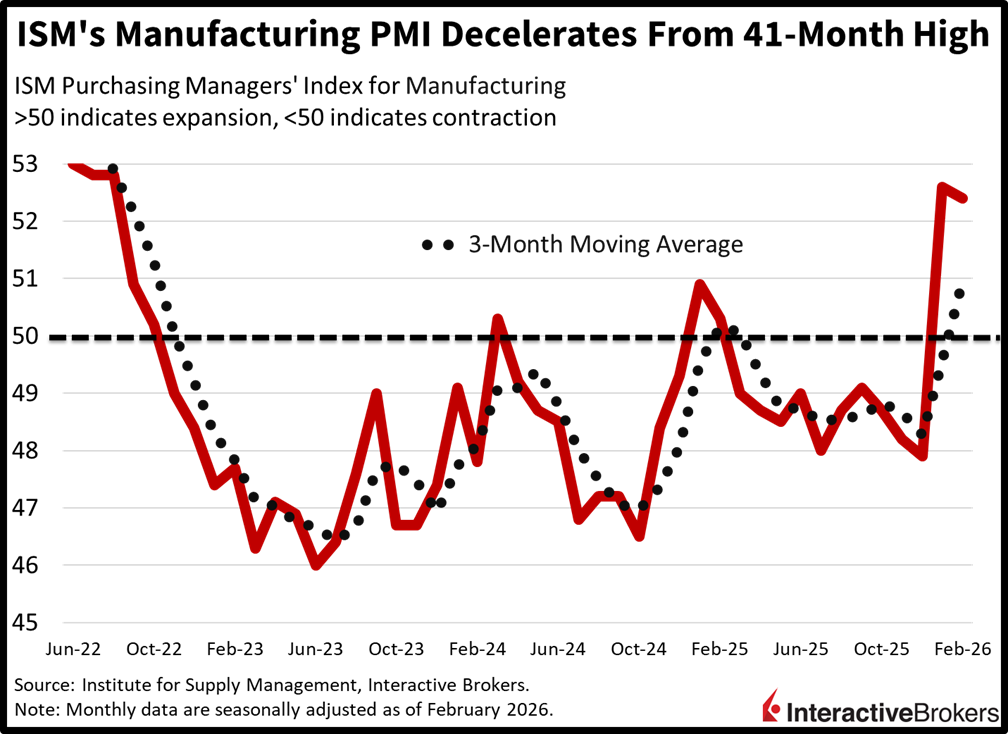

Markets are off to a rough start to initiate this new month as US military strikes in Iran spark turbulence on Wall Street. Energy prices are jumping as a prolonged clash threatens to raise inflationary pressures immediately following a week in which participants were increasingly pricing in several rate cuts this year. Yields and the greenback are surging on that heavier geopolitical premium in consideration of the Middle East housing one third of the world’s crude supplies. Additionally, the conflict’s threat to shipping in the Strait of Hormuz is lifting risks of insufficient barrels just a few weeks after analysts were worried about a glut. But stocks have turned positive, as WTI declined from a daily high of $75.33 to $70.16, helping to quell concerns of margin compression generated by a potential acceleration in cost forces that could lift corporate expenses while revenues could be adversely impacted by consumers facing pain at the pump. This morning’s economic calendar was somewhat supportive of a rebound in risk sentiment, with ISM-manufacturing posting a sizeable beat although it was accompanied by the strongest price momentum in 44 months, which executives blamed on tariffs. Elsewhere, non-energy commodities are lower and volatility levels are increasing while cryptocurrencies and forecast contracts catch bids.

Manufacturing activity has continued to expand this year as incentives from 2025’s passage of the Big Beautiful Bill helped deliver a beat for this morning’s February ISM report. But survey respondents complained that tariff effects are negatively affecting prices and margins, with the cost aspect of the print arriving at an elevated 70.3, the loftiest since June 2022’s 78.5. The Institute for Supply Management’s headline number of 52.4 was slightly beneath January’s 41-month high of 52.6 although it exceeded the projected 51.8. Demand was stellar with new orders, backlogs and exports growing at 55.8, 56.6 and 50.3. Employment was a drag, however, coming in at 48.8 even with production at 53.5, as factories increased their use of AI and automation to reduce headcounts.

The call of being long duration has worked well so far in 2026 as the 10-year started January near 4.20% and dropped to as low as 3.92%. But with geopolitical tensions flaring and energy supplies potentially being compromised, yields could rise significantly from here as inflation threatens to accelerate. The pivotal factors to watch are where oil prices reach from a level perspective as well as how much time they stay there, because that would directly raise cost forces and materially impact economic reports in April and May, similar to what Russia’s invasion of Ukraine did to inflation pressures. Such a development would extend the hold-up for the first reduction from a Warsh Fed and policy easing is an occurrence that bullish participants have been counting on. This would especially be an adverse situation for equity investors, as the cyclically oriented, rate-sensitive aspects of the market have been offsetting weakness in tech, and those areas need monetary accommodation to resume their climb. For now, a quick resolution and peace in the Middle East would be tremendously beneficial to Wall Street.

South Korea’s trade surplus doubled in February as strong demand for artificial intelligence products (AI) helped the country boosts its exports. The news comes shortly after Singapore announced that the manufacturing of AI semiconductor products in January caused industrial output growth to accelerate and exceed expectations. South Korea’s February trade surplus of $15.51 billion nearly doubled from the preceding month’s $8.72 billion and surpassed the $10 billion level expected by a consensus of economists. Exports jumped 29% year over year (y/y) in February, which slowed from the 33.8% gain in January but significantly outperformed the economist consensus estimate for a 24% climb. The strength was driven by semiconductor exports soaring 160.9% to a new monthly record. Imports, meanwhile, were only 7.5% higher than in the year-ago period, a deceleration from the 11.6% y/y expansion in January. Economists anticipated that purchases of items from foreign nations would be 13% above the level in February 2025.

The number of help-wanted advertisements in Australia climbed 3.2% month over month (m/m) in February after January’s 5.2% expansion, according to the Australian and New Zealand Banking Group. It marked the second monthly gain after four months of declines.

The Melbourne Institute Inflation Gauge depicted prices falling 0.2% m/m in February following the 0.2% gain in the first month of the year. The organization attributes the result to a decline in transportation costs due to lower fuel costs. On an annualized basis, inflation is elevated, exceeding the 2% to 3% target range.

Fourth-quarter gross profits in Australia were up 5.8% quarter over quarter (q/q) during the final three months of 2025, a strong acceleration from the 1.5% advance in the third quarter, according to the Australian Bureau of Statistics. Economists expected profits to be only 1.8% higher than in the three-month period ended in September. Transport, postal and warehousing earnings ascended by 8.9%, mining profits were up 8.1% and results for the wholesale sector were 6.5% stronger.

Net borrowing of consumer credit by individuals reached £1.8 billion in January following December’s £1.7 billion result. On an annualized basis, consumer credit grew at an unchanged rate of 8.3% while the growth rate of credit card borrowing eased slightly from 12.4% to 12.3%. Other forms of consumer credit, however, expanded at a 6.5% annualized rate following December’s 6.4% print. Also in January, mortgage volumes softened. The net value of approvals for housing financing slipped from December’s £4.5 billion to £4.1 and the number of approved loans fell from a six-month average of 64,100 to 60,000.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!