- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted June 11, 2025 at 12:29 pm

Markets are soaring following a lighter-than-anticipated CPI report that is quelling fears about tariff-related inflation and boosting enthusiasm that the Fed will cut rates in the next two or three meetings. Bulls are also energized by a de-escalation in trade tensions between Washington and Beijing with President Trump taking somewhat of a victory lap this morning while remarking that the relationship of the world’s two largest economies is excellent. He also said the trade deal is done.

The bullish one-two combination has economists dialing growth projections north while adjusting price pressure expectations south, which is supporting an outlook for continued corporate earnings buoyancy. Furthermore, the yield curve is shifting in bull-steepening motion led lower by the short-end, as robust GDP forecasts contain duration ahead of auctions today and tomorrow amounting to $61 billion worth of 10- and 30-year government debt. Optimism will likely be bolstered if the offerings see satisfactory demand, like yesterday’s showing for 3-year notes. Traders are high fiving each other and are picking up stocks in all sectors minus consumer staples and materials, Treasuries along the maturity structure, forecast contracts, and futures tied to crude oil, lumber and gold commodities. Meanwhile, investors are unwinding volatility hedges and reducing exposures to the greenback, bitcoins and copper, silver and natural gas commodities.

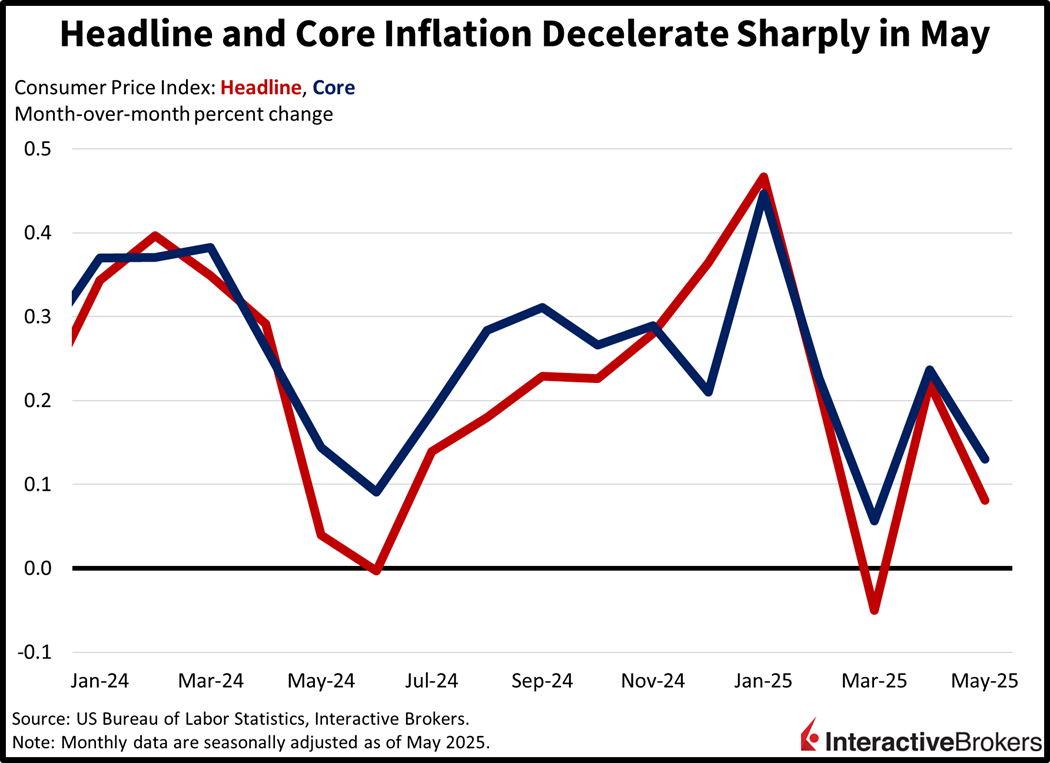

We saw barely any inflation last month with this morning’s Consumer Price Index featuring a long list of declines across categories. May’s CPI rose just 0.1% month over month (m/m) and 2.4% year over year (y/y), softer than estimates by a tenth of a percent. In the preceding month, the gauge was up 0.2% m/m and 2.3% y/y. In May, the core version of the indicator, which excludes food and energy due to their volatile characteristics, increased 0.1% m/m and 2.8% y/y, lighter than the 0.3% and 2.9% projections and similar to April’s 0.2% and 2.8% results.

The following items and the amount of their sticker declines kept price pressures in check:

Items that moved the other way and the amount of their increases included the following:

With the S&P 500 a little more than 1% off its all-time high, this morning’s CPI print is widening the path for a momentous second-half rally. Moreover, a burst of illumination in the once gloomy Trump trade tunnel has traders and economists alike throwing on their sunglasses in preparation for rate cuts, robust profitability and activity. While things are positive, for the time-being, the greatest risk on the horizon is the national debt load and the potential for heavier term premiums to weigh on Treasury prices. But in recent sessions, bond vigilantes have stepped up and reversed course at the critical levels across 2s, 10s and 30s at 4%, 4.50% and 5%, respectively.

Central Bank President Christine Lagarde yesterday warned that tariffs could threaten economic well-being and are an unsustainable solution to trade tensions. During a speech at the People’s Bank of China, she explained that countries are strongly connected through global supply chains and the decline in geopolitical alignment is creating risks to the foundations of global prosperity.

Regarding the European economy, ECB Chief Economist Philip Lane this morning opined that the latest rate cut will help prevent inflation from falling below the central bank’s 2% target. Last week, the organization lowered its benchmark rate for the eighth time in 12 months. Lane also expressed support for issuing Europe backed debt, a change that could increase the role of the euro as a global reserve currency.

South Korea’s low unemployment rate of 2.7% was unchanged in May and matched the consensus forecast. On a y/y basis, the number of unemployed dropped by 32,000 to 853,000 while employment jumped by 245,000 to 29.16 million. During the one-year period, payroll expansion was led by the elderly with approximately 370,000 individuals older than 60 joining the workforce. Conversely, payrolls for South Koreans in the age range of 15-29 fell by 67,000. Manufacturing and construction industries contracted but health and social welfare services, science and technology, and the insurance and finance category added positions.

Input costs for Japanese businesses dropped 0.2% m/m in May after climbing 0.3% in the preceding month, according to the Corporate Goods Price Index (CGPI), which is also referred to as the Producer Price Index. On a y/y basis, furthermore, prices headed north by only 3.2%, below the economists forecast of 3.5% and lower than 4.1% in April.

Certain energy items kept price pressures in check with the petroleum and coal products group being 4.85% less expensive than in April. Business-oriented machinery fell 0.7% followed by the 0.4% drop for chemicals and related products. Among items that became more costly, electric power, gas and water jumped 2%, agriculture, forestry and fishery products gained 1.1% and electrical machinery and equipment was 0.6% loftier. Export prices fell 0.7% m/m and 6.4% y/y on a yen basis while imports stickers declined 1.1% and 10.3% during the reporting periods.

Plans for construction fell for a second-consecutive month in Canada with the number of building permits issued in May falling 6.6% m/m, according to Statistics Canada. A consensus of economists predicted a 1.9% gain, which would have been a reversal from April’s 5.3% decline.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Related Articles

")

wow…those glasses you are wearing are truly rose-colored…love the absence of any semblance of objectivity in your piece.