- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted December 29, 2025 at 1:02 pm

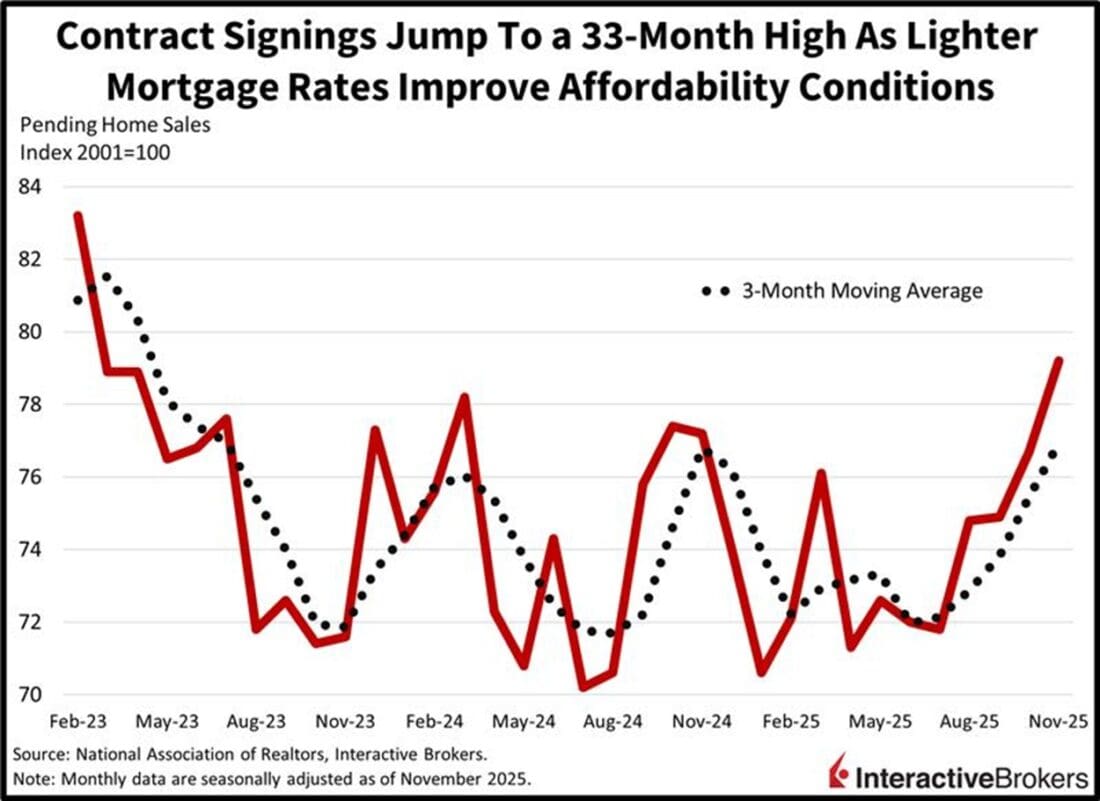

Stocks are failing to sustain the enthusiasm from last week, with investors reducing their risk exposures following two consecutive trading days of fresh records on the S&P 500 amidst fragile geopolitical situations in Caracas and Kyiv. The safe-haven silver and gold commodities reached all-time highs earlier in the morning as participants gravitated to precious metals before they aggressively sold off in U-turn fashion; they are now retreating 9% and 5%, respectively. Treasuries are catching bids due to their defensive nature though and are continuing to advance alongside crude oil, as are shares in the consumer staples, healthcare and utilities sectors. Real estate is also gaining and countering selling pressure on Wall Street, helped by the strongest level of pending home sales in 33 months. The significant beat was driven by softer mortgage rates and heavier inventories that are improving affordability, propelling transactions as a result. Thankfully for fixed-income and for the hopes of an intraday recovery, however, the robust print didn’t raise yields since the statistics are lighter-impact. Meanwhile, a lack of speculative energies has folks reaching for volatility protection instruments in case there’s turbulence around the corner. The greenback and forecast contracts are also seeing interest. Conversely, bitcoin and commodities ex crude are declining.

Pending home sales improved for the fourth consecutive month in November, reaching the highest level since February 2023, according to this morning’s National Association of Realtors’ (NAR) release. Pending sales, furthermore, strengthened in all four of the country’s regions. The NAR attributes the strong results to lighter borrowing costs improving affordability, wages increasing at a faster pace than house stickers and more inventory. The results are additional evidence that the residential real estate market had bottomed in recent months. Contract signings climbed 3.3% month over month (m/m) and 2.6% year over year (y/y), compared to the 2.4% m/m gain and 0.4% y/y decline results in the preceding month. Economists anticipated a 1% m/m print. Transactions grew 9.2%, 2.4%, 1.8% and 1.3% across the West, South, Northeast and Midwest regions.

Market bulls appear like they needed a break today as Friday’s record brought the S&P 500 to an approximate year-to-date gain of 18%. The three-year run in stocks has been terrific and annual appreciation rates near 20% would certainly be something that the investing community could get used to. Indeed, 2023 and 2024 both delivered returns north of 23%, and after a stellar 2025, participants are geared up for another sprint in 2026. But there’s good reason to believe that performance could be more tempered going forward, as valuation expansion has its limits and the setup is conducive to a period of muted gains or a so-called flat year, in order for Wall Street to digest the advances of preceding periods. The economy is healthy overall and there is fuel in the tank for further upside, however, the longer we extend earnings multiples, the higher the bar is for corporates to meet expectations, the slimmer the margin for error gets and the incrementally riskier it is to remain long.

Strong demand for electrical equipment, machinery and appliances helped push Hong Kong’s November exports up 18.8% year over year (y/y), the strongest gain since January 2024’s 33.6% ascent. In October, the special administrative district’s exports grew 17.5%. November purchases from foreign markets also climbed but the 18.1% rate eased slightly from 18.3% in the preceding print.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!