- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted January 16, 2026 at 1:00 pm

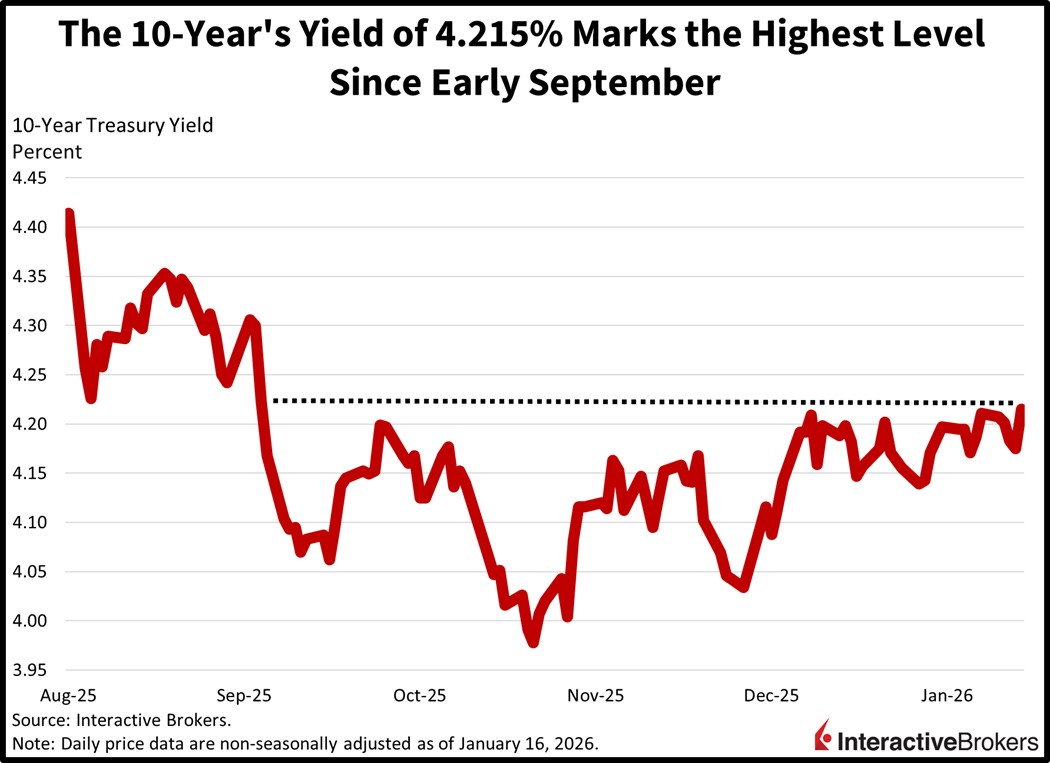

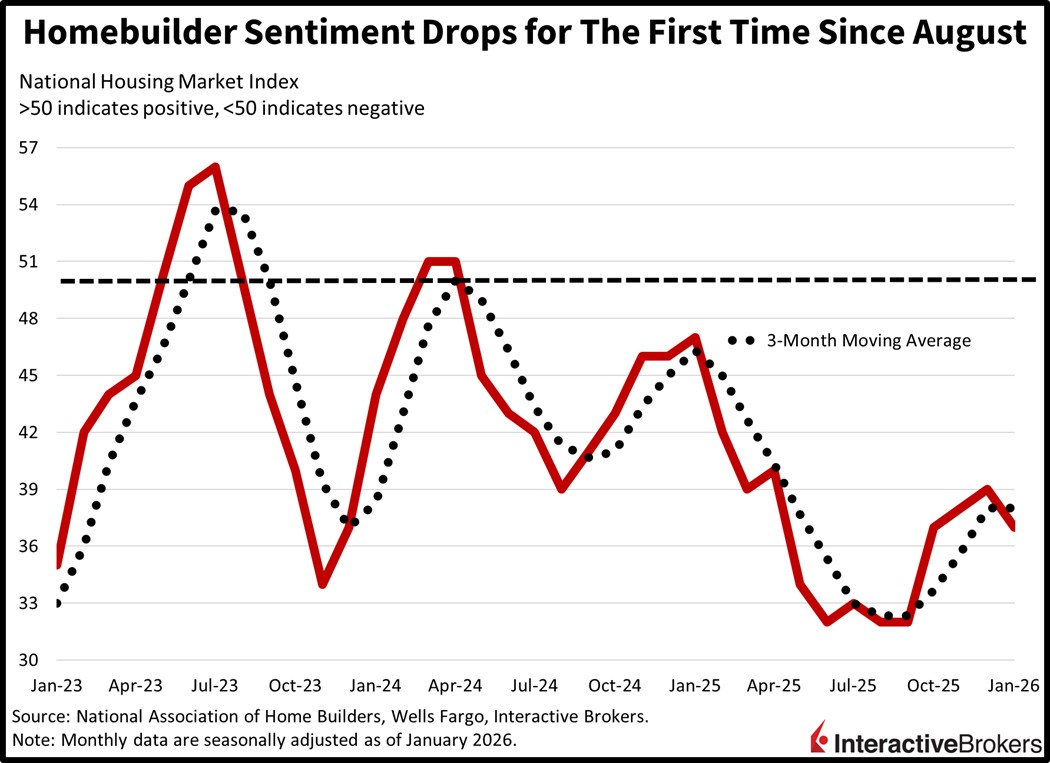

The 10-year yield jumped to a four-month high this morning as fixed-income watchers braced for potential geopolitical risk over the weekend in Tehran. A possible adverse impact of rising tensions is the threat of a reduction in energy supplies, which is sending oil prices and tightly correlated inflation expectations north. Another factor in consideration is soaring odds of former Fed Governor Kevin Warsh being nominated to the helm of the central bank after President Trump told National Economic Council Director Kevin Hassett that he’d prefer to keep him where he is. Warsh, meanwhile, is perceived as increasingly likely to be influenced by the commander in chief rather than prioritizing the monetary policy authority’s independence, and that too is lifting interest rates, particularly at the long-end as the curve ascends in bear-steepening fashion. Additionally weighing on Treasury performance is the head of state threatening new tariffs to nations that don’t go along with Washington’s quest to acquire Greenland in the name of sovereign security, which is generating cost pressure and military spending uncertainties, raising term premiums as a result. The economic calendar was mixed though, as a big beat on industrial production coincided with an enormous miss on homebuilder sentiment. Elsewhere, stocks are near their flatlines, commodities are mostly lower and Bitcoin and Ethereum are down. Forecast contracts, however, are catching bids.

Homebuilder sentiment started the year off on the wrong foot with January featuring the first drop since August. Labor shortages, regulatory hurdles, high materials costs and an overreliance on sales incentives offset the tailwind of lighter mortgage rates, with the headline figure dropping to 37. The print was a surprise to the consensus, which projected an increase to 40 from the 39 reported in December. The three major components fell, with current transactions, the expected pace of closings in 6 months, and the traffic of prospective buyers slipping from 42, 52 and 26 to 41, 49, and 23. From a regional perspective, meanwhile, an improvement in the Northeast from 42 to 48 wasn’t enough to counter decreases in the Midwest, South and West which declined from 47, 35 and 36 to 42, 34 and 34.

December industrial production delivered a significant beat, carried by strong capital expenditure momentum that is likely a result of President Trump’s 2025 signature taxation package that provides 100% first-year depreciation write-offs for many new investment categories. The headline figure rose 0.4% month over month (m/m) despite the consensus expecting growth of just 0.1%. Output expansions in the utilities and the manufacturing sectors amounting to m/m gains of 2.6% and 0.2%, were partially countered by weakness in mining, which fell 0.7% during the period. Among major market groups, activity across business equipment, consumer goods and materials increased 0.8%, 0.7% and 0.2% m/m, but construction sank 0.3%.

Yields have been range bound since early September and that dynamic has fostered limited volatility in the stock market. But a 15-basis point breakout north across the curve that brings the 2-year to 3.75% and 10s to 4.35% would weigh on risk appetite throughout Wall Street. Those numbers would essentially signal that the easing cycle should end, considering that they’re much higher than the current Fed minimum on overnight funds of 3.5% and effectively eliminates one of the key motivators for continued bullishness which is more rate cuts. Meanwhile, large-cap equity benchmarks appear tired, with the S&P 500 and Dow Jones Industrial indices failing to break above the pivotal psychological milestones of 7k and 50k despite a robust broadening, good news from Taiwan Semi on AI and cooperative economic data including dropping unemployment, firm consumer spending and inflation stabilizing in the mid 2s. Conversely, the Russell 2000 has been on a role, however, its capacity to carry overall animal spirits is quite meager, as its constituents lack the notoriety and excitement of its big-tech counterparts to drive significant multiple expansion.

Singapore’s non-oil exports (NODX) last month slipped 9.4% m/m, a bigger drop than the economist consensus estimate calling for a 4.5% contraction following November’s 7.1% gain. Despite the monthly decrease, NODX was up 6.1% relative to the year-ago period, beneath the 10% expected and the 11.5% from the prior period, however.

Electronic products were 24.9% higher than in December 2024. Within this category, integrated circuits, disk media products and telecommunications equipment expanded 32.1%, 53.5% and 81.4%. Shipments of non-electronic products grew only 0.8% with non-monetary gold, specialized machinery and mechanical handling equipment up 73.3%, 5.4% and 415.8%. Demand from Taiwan grew 24.3% and was followed by the 17.9% and 13.3% ascents from China and Malaysia. Conversely, the US cut imports by 36.3% despite a 56% jump in purchases of electronics. Shipments to Indonesia, Japan, Thailand, Hong Kong and the European Union, furthermore, sank 27.9%, 26.4%, 17.9%, 17.7% and 5.4%.

Residential housing starts in Canada grew 11% m/m in December, reaching a seasonally adjusted annualized rate (SAAR) of 282,439 units, according to the Canada Mortgage and Housing Corporation. In November, starts occurred at a SAAR pace of 254,625. December results were slightly stronger in urban areas with a 12% m/m increase.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!