- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted August 14, 2024 at 10:15 am

Given the recent instability of the market, now is the perfect time to share a universal law that most investors don’t know, but need to know if they want to enjoy any sort of long-term success. It’s a secret I got from my time on Wall Street about the nature of investing. The secret is based on the second law of thermodynamics. Please don’t tune out just because I got super geeky there, I promise you will be a better and smarter investor when you finish reading this letter. You’ll also get free research on 3 mega cap stocks and a link to join our next live podcast.

I think it’s time to come back to some basic principles about life and investing. First, a little background. The market has been on an incredible run for the last 20 years. Sure, we’ve seen a few downdrafts, but take a look at Figure 1. Tech stocks over the last 10 years have crushed it. Note how small a blip the late 1990s’ tech bubble is compared to the last several years. True, a logarithmic chart of the Nasdaq-100 is probably more appropriate. I looked at that version, and it doesn’t change the message. The market feels a little too good to be true to me…and you won’t hear many other people admit that.

Figure 1: Nasdaq-100 Performance Since June 1995

Sources: Google Finance

Considering the huge amount of both Fiscal and Monetary stimulus poured into our economy over the last 10 years (detailed in a prior letter here) , no one is surprised that we have an inflation problem, a very stubborn one. That inflation applies to the stock market, too. I’m sure you could name a lot of other problems as well as some very promising trends.

But, the one problem we need to keep top of mind is “entitlement”. Specifically, entitlement to double digit returns on stocks in the short, medium and long term. Too many investors have grown up in a world where “buy the dip” literally works every time. They do not care why it works, just that it works. And, they do not care why stocks go up, just that they go up. If you don’t believe me, just ask any meme stock investor.

The problem here is not that stocks are going up. Many stocks deserve to have gone up and to go up much more. We provide many lists of such stocks to our clients. I’m also hosting a live show on August 15, 2024 to show investors how to perform due diligence to find the best stocks – sign up here.

The problem, as shown in Figure 1, is the disproportionate outperformance of certain stocks, like the “Magnificent 7”. There are too many stocks that have gone up way too much. They are priced for perfection, an impossible perfection according to our reverse DCF models. But, no one else wants to talk about that.

Unless this is your first time reading my letters, you’re well aware that New Constructs is different from other research firms. We’re in the business of making our clients smarter. We want you to win. And, as I will show below and have shown with empirical evidence in prior letters, most other research firms are looking out for themselves not you.

That fact is central to my message (and secret) today. Wall Street firms and advisors like to make you think everything is taken care of. Perfection is possible. They’ve done their diligence and scrubbed the numbers. Their ratings are reliable. And, they keep telling us that we can trust them when they say perfection is possible even though time and again, we learn that we can’t trust them. Remember this scene from the movie The Big Short – more details in my last letter.

Now, here’s where the second law of thermodynamics comes in. It states that

“as one goes forward in time, the net entropy (degree of disorder) of any isolated or closed system will always increase (or at least stay the same).” Source.

Entropy is a measure of disorder and affects all aspects of our daily lives.

The stock market is not immune to the law on entropy or the second law of thermodynamics. Constant work is required to maintain order. Order is not free. Things are changing all the time. Perfection is not possible.

This law applies to the stock market and every single stock. Constant work is required to maintain good analysis of every single company. Prices change every day, new filings come out nearly every day. Yet, so many financial advisors want to portray the illusion that they’ve got it all under control. You can trust them. They and their firm have so many smart people, and they’ve covered all the bases. They have all the answers, that’s why you should trust them and give them all your money.

Well, I will be the first to tell you that neither I nor New Constructs have all the answers. That’s impossible. We’re not perfect. We are not right all the time. No one has all the answers. We’re modest enough to admit that. At New Constructs, we understand our limitations, which allows us to also understand our strengths. We will tell you what we can do and cannot do. For example, at 3 minutes and 30 seconds into my CNBC interview last Thursday, Tyler Mathisen asks me to explain why the market was down that day. My answer: “my crystal ball is in the shop.” After giving Tyler and Kelly Evans some very specific answers about Intel (INTC), Meta (META) and Amazon (AMZN), I abruptly refused to pretend I could explain what was happening in the overall market. I made a few jokes at my own expense and noted that trying to explain what’s happening in a market where a character like Roaring Kitty can move markets is a fool’s errand.

Figure 2: Clip from My CNBC Interview

Sources: CNBC: Three Stock Lunch

Try finding an advisor or Wall Street insider who won’t take every opportunity to prognosticate on the state and future of the market. They even have a special name for Wall Street’s market prognosticators. They call them strategists. Guess what percentage of them are bullish at any given time? How many research firms have a Zombie Stock list?

Now, as you think about your money and your research, I have a few more questions for you.

Can you put a price on honesty?

Can you put a price on humility?

I think humility is absolutely essential to being a successful investor and analyst. It’s as important to know what you don’t know as what you do know. But, that’s not how most investors think.

I will never forget the meeting I had with a portfolio manager of a $50+ billion fund back around 2005. After explaining to him what New Constructs offered, he replied with:

“Your data probably is better. But, as long as everybody’s using the same bad data, I’m OK with that.” Source: Harvard Business School Case #118068

Not a lot of humility there. To say he does not care about having the best data means that he believes he can outperform with inferior data. That’s pretty cocky. Either that or he doesn’t care about outperforming. I’m not sure which is worse.

I’ve had many other similar meetings with “professional” investors. It’s not just the sell-side Wall Street folks that should worry you, but the big money managers on the buyside are not always doing their homework either. And, they are so arrogant that they will say out loud that they do not care about diligence sometimes.

My point is that a big part of humility is recognizing how hard it is to do proper research and diligence.

Ever notice how we talk about diligence a lot, especially compared to other firms. Other firms would prefer you keep thinking the music will never stop, perfection is possible, and stocks will just keep going because….well that’s what stocks do.

Are you the type to believe that stocks will just continue to go up forever? Do you think that fundamentals matter? If you’ve read this far, my guess is the answers to the last two questions are “no” and “yes”.

We’re very focused on one thing at New Constructs: delivering superior fundamental research. As I’ve mentioned before, there are few signs out there that we are good at what we aim to do:

Now, the biggest question I have for you is whether you’re ok with using the same bad data as everyone else?

Don’t think there’s bad data out there? Let me provide more examples.

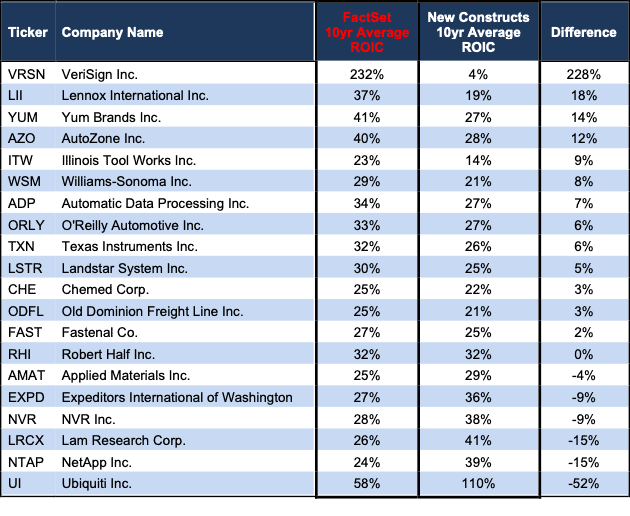

A recent MarketWatch article featured return on invested capital (ROIC) research from FactSet (FDS) and allows us another real-time opportunity to compare our research to a competitor’s. On July 16, 2024, we highlighted alarming differences between our research and Morningstar’s.

As with Morningstar, there are very large differences between our research and FactSet’s. For example:

More details in Figure 3.

Figure 3: 10-Year Average ROIC: New Constructs vs. FactSet

Sources: New Constructs, LLC and FactSet data from here

We also see very large differences in the 3-Year Average ROICs from FactSet compared to our research. For example:

See Figure 4.

Figure 4: 3-Year Average ROIC: New Constructs vs. FactSet

Sources: New Constructs, LLC and FactSet data from here

The main takeaways from these comparisons are:

Over the last several weeks, we’ve given out a lot of free data and stock picks because we hope to earn your business by showing the value we deliver. We also hope that you see the humility in our service to you and the betterment of the capital markets.

…

Diligence matters,

David

—

Originally Posted August 13, 2024 – Humility Matters, Too

Disclosure: David Trainer, Kyle Guske II, and Hakan Salt, receive no compensation to write about any specific stock, sector, style, or theme.

David Trainer, Kyle Guske II, Sam McBride, Matt Shuler, Alex Sword, and Andrew Gallagher receive no compensation to write about any specific stock, style, or theme.

The information and opinions presented in this report are provided to you for information purposes only and are not to be used or considered as an offer or solicitation of an offer to buy or sell securities or other financial instruments. New Constructs has not taken any steps to ensure that the securities referred to in this report are suitable for any particular investor and nothing in this report constitutes investment, legal, accounting or tax advice. This report includes general information that does not take into account your individual circumstance, financial situation or needs, nor does it represent a personal recommendation to you. The investments or services contained or referred to in this report may not be suitable for you and it is recommended that you consult an independent investment advisor if you are in doubt about any such investments or investment services.

Information and opinions presented in this report have been obtained or derived from sources believed by New Constructs to be reliable, but New Constructs makes no representation as to their accuracy, authority, usefulness, reliability, timeliness or completeness. New Constructs accepts no liability for loss arising from the use of the information presented in this report, and New Constructs makes no warranty as to results that may be obtained from the information presented in this report. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information and opinions contained in this report reflect a judgment at its original date of publication by New Constructs and are subject to change without notice. New Constructs may have issued, and may in the future issue, other reports that are inconsistent with, and reach different conclusions from, the information presented in this report. Those reports reflect the different assumptions, views and analytical methods of the analysts who prepared them and New Constructs is under no obligation to insure that such other reports are brought to the attention of any recipient of this report.

New Constructs’ reports are intended for distribution to its professional and institutional investor customers. Recipients who are not professionals or institutional investor customers of New Constructs should seek the advice of their independent financial advisor prior to making any investment decision or for any necessary explanation of its contents.

In-depth risk/reward analysis underpins our stock rating. Our stock rating methodology grades every stock according to what we believe are the 5 most important criteria for assessing the quality of a stock. Each grade reflects the balance of potential risk and reward of buying that stock. Our analysis results in the 5 ratings described below. Very Attractive and Attractive correspond to a “Buy” rating, Very Unattractive and Unattractive correspond to a “Sell” rating, while Neutral corresponds to a “Hold” rating.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from New Constructs and is being posted with its permission. The views expressed in this material are solely those of the author and/or New Constructs and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

")

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!