- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted March 6, 2026 at 11:00 am

As the global economy moves into 2026, it is firmly in the late stage of the post-pandemic business cycle. More than five years on from the COVID-19 recession, growth has moderated but remains resilient. Labour markets are still relatively tight, inflation pressures have eased without fully disappearing, and financial conditions, while no longer loosening aggressively, remain broadly supportive. Importantly, neither market consensus nor WisdomTree’s central scenario anticipates an imminent recession.

This matters for commodities. Historically, late-cycle environments have been among the most constructive phases of the business cycle for real assets. As spare capacity diminishes and supply constraints become more binding, commodity prices have tended to outperform traditional financial assets, even as equity markets become more sensitive to slowing growth and earnings risk.

Late cycle does not mean late game

Although commodities and equities are both cyclical, their cycles are not synchronised. Equities respond primarily to earnings expectations and financial conditions. Commodities, by contrast, respond more directly to physical supply-demand balances. As expansions mature, underinvestment in new supply and rising marginal production costs often become more apparent, conditions that historically favour commodities.

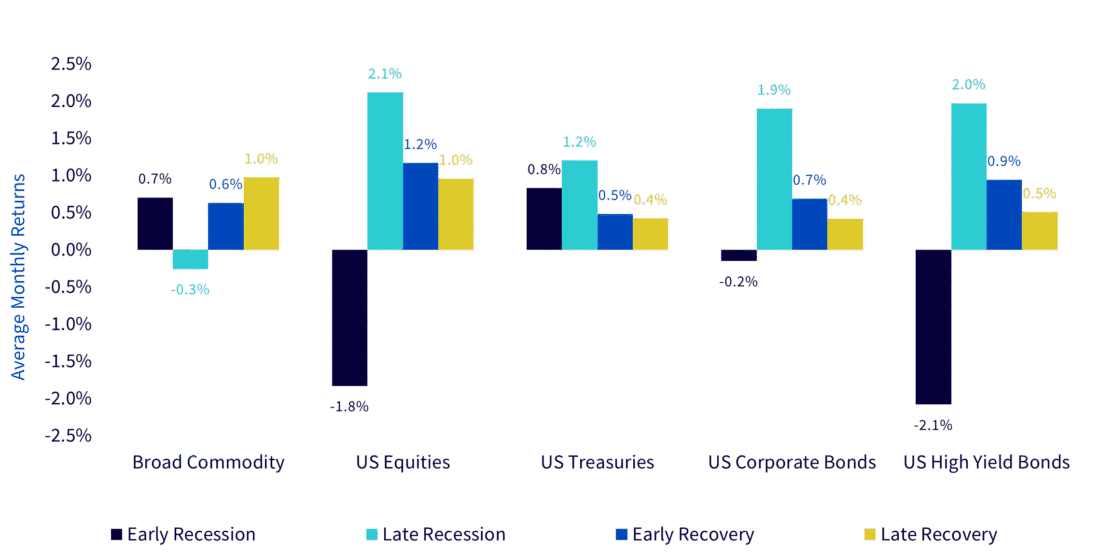

Figure 1: Performance across different stages of the business cycle

Source: WisdomTree, Bloomberg, S&P. From January 1960 to December 2025. Calculations are based on monthly returns in USD. Broad commodities (Bloomberg commodity total return index) and US Equities (S&P 500 gross total return index) data started in Jan 1960. US treasuries (Bloomberg US treasury total return unhedged USD index) and US corporate bonds (Bloomberg US corporate total return unhedged USD index) data started in Jan 1973. US high yield bonds (Bloomberg US corporate high yield total return unhedged USD index) data started in July 1983. Expansion and Recession phases are defined using the NBER website. To define early and late expansion/recession, the periods are split in half time-wise. Historical performance is not an indication of future performance, and any investments may go down in value.

History also suggests that commodities offer asymmetric protection if growth deteriorates unexpectedly. While equities have typically struggled in the early stages of recessions, commodities have often delivered returns comparable to US Treasuries, reflecting currency effects, policy responses and the tendency for supply adjustments to lag demand slowdowns.

Whether the global economy remains in a prolonged late-cycle expansion or transitions into recession during 2026, the macro backdrop remains supportive for commodities relative to traditional risk assets.

The US dollar: A structural headwind re-emerges

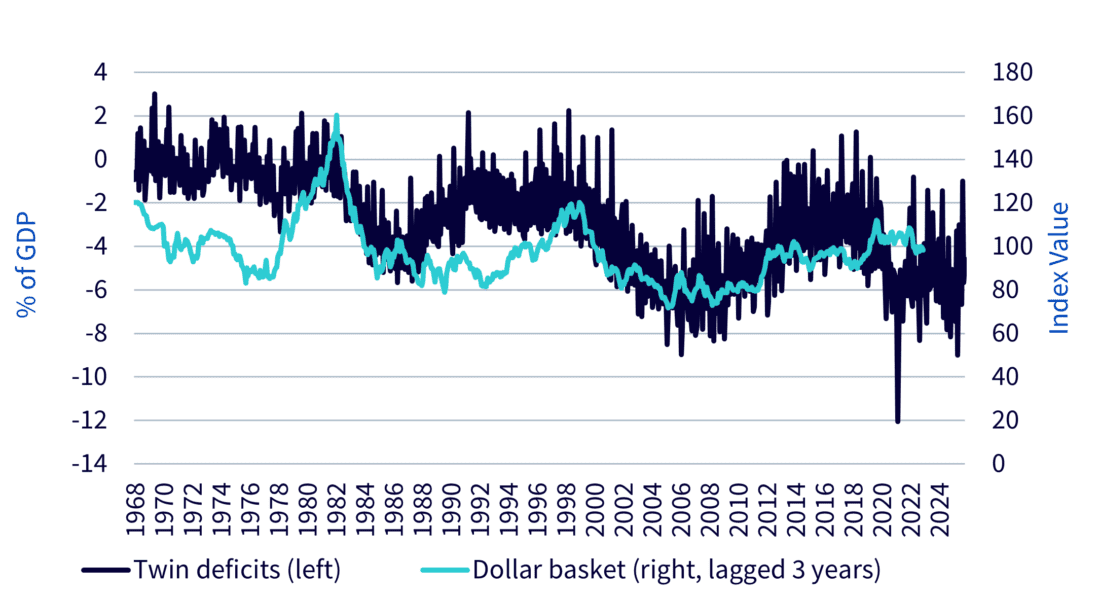

The outlook for the US dollar reinforces this constructive view. After a modest recovery late in 2025, the dollar resumed its downward trend in early 2026. While short-term moves continue to reflect interest rate expectations, the broader trajectory is increasingly shaped by structural pressures.

Persistent ‘twin deficits’, large fiscal and current-account shortfalls, remain central. The rising interest burden on US public debt is becoming more constraining, and history suggests that sustained deficit expansion is typically associated with currency depreciation, albeit with a lag.

Figure 2: US dollar and US twin deficits

Source: WisdomTree, Bloomberg, January 1968 – December 2025. Twin Deficit = Current Account + Budget Deficit as a % of GDP. Dollar Basket (DXY). Historical performance is not an indication of future performance, and any investments may go down in value.

Beyond macro fundamentals, confidence in the United States as a stable geopolitical anchor has weakened. Greater reliance on trade policy as a strategic tool and rising uncertainty around security commitments have encouraged gradual diversification away from US-centric assets. For commodities, most of which are priced in dollars, this environment is typically supportive, reinforcing their late-cycle appeal.

Metals: Where structure dominates cyclicality

Within commodities, metals stand out as the clearest expression of structural change.

Gold: From diversifier to pseudo-currency

Gold’s strongest annual performance since 1979 in 2025 was not simply a cyclical rally. The scale and persistence of the move increasingly point to a regime shift. Trade fragmentation, rising public debt burdens, pressure on central-bank independence and a reassessment of global security arrangements have collectively expanded gold’s role from portfolio diversifier to something closer to a pseudo-currency.

Crucially, this shift is being reinforced by structurally durable sources of demand. Central banks, Chinese insurance companies, Indian pension funds and non-traditional institutional buyers have all increased allocations. These forces suggest gold may be transitioning toward a higher long-term equilibrium than implied by models calibrated on the past three decades of relatively stable globalisation and monetary credibility.

Copper: Tight today, tighter tomorrow

Industrial metals tell a similar story of structural demand meeting fragile supply. Copper increasingly reflects long-duration investment cycles tied to electrification, renewable energy, grid expansion and data-centre infrastructure, rather than short-term fluctuations in global growth.

While China’s property-led commodity supercycle has ended, it has been replaced by sustained demand from the energy transition and digital infrastructure. On the supply side, long development timelines, declining ore grades, rising capital costs and growing concentration risk limit the scope for a rapid response. The result is a market where deficits are increasingly likely to persist, even if cyclical demand moderates.

Policy-managed metals and the exception of oil

Other metals, including aluminium, cobalt and nickel, increasingly behave as policy-sensitive assets. Production caps, power constraints and export controls have reduced supply elasticity, shifting price formation away from purely market-driven equilibria toward administratively managed outcomes.

Oil, by contrast, stands apart. Despite elevated geopolitical risk, the market enters 2026 with substantial inventories and robust non-OPEC1 supply growth. These buffers limit the scope for sustained upside in the base case, even as headline-driven volatility persists.

Conclusion: Commodities in a structurally changing world

The defining feature of the commodity outlook for 2026 is not cyclical recovery, but structural transformation. Across metals, supply has become more constrained, more concentrated and more politicised, while demand is increasingly shaped by electrification, strategic investment and institutional behaviour.

Precious metals have evolved from tactical hedges into strategic reserve assets. Industrial metals are increasingly linked to long-term infrastructure and energy security themes. Together, these dynamics argue for a strategic, rather than purely tactical, allocation to commodities.

In a world defined by late-cycle macro conditions, structural US dollar headwinds and growing policy intervention, commodities, particularly metals, offer diversification benefits and exposure to long-term structural change that are increasingly difficult to replicate elsewhere in portfolios.

1 The Organization of the Petroleum Exporting Countries.

—

Originally Posted March 4, 2026 – Commodities 2026: Late cycle, new regimes

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Please click here for our full disclaimer.

Jurisdictions in the European Economic Area (“EEA”): This content has been provided by WisdomTree Ireland Limited, which is authorised and regulated by the Central Bank of Ireland.

Jurisdictions outside of the EEA: This content has been provided by WisdomTree UK Limited, which is authorised and regulated by the United Kingdom Financial Conduct Authority.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from WisdomTree Europe and is being posted with its permission. The views expressed in this material are solely those of the author and/or WisdomTree Europe and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Investments in certain commodities (precious metals) may be subject to significant price volatility and often involve risks related to market fluctuations, liquidity constraints, geopolitical events, and changes in global economic conditions that could adversely affect their value.

U.S. Spot Gold trading through IB LLC accounts is only available to legal residents of the United States that do not reside in Arizona, Montana, New Hampshire, and Rhode Island.

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

There is a substantial risk of loss in foreign exchange trading. The settlement date of foreign exchange trades can vary due to time zone differences and bank holidays. When trading across foreign exchange markets, this may necessitate borrowing funds to settle foreign exchange trades. The interest rate on borrowed funds must be considered when computing the cost of trades across multiple markets.

Spot currencies are not available at IBKR Singapore.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!