- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted July 8, 2024 at 10:15 am

Tyler Wood examines the technical health of the US equity markets and sees reasons to be cheerful in cruise liners, biotech, healthcare and news media industries.

The following is a summary of a live audio recording and may contain errors in spelling or grammar. Although IBKR has edited for clarity no material changes have been made.

Welcome to this week’s episode, my name is Andrew Wilkinson. We’re here at the end of the first half of 2024. We’re heading into elections in France and the UK as we take a 4th of July break here in the United States. And joining me to assess the stock market is technical analyst, Tyler Wood from the Chartered Market Technicians Association or CMT. Welcome, Tyler. How are you?

I’m doing great, Andrew. Thanks so much for having me back. Nice to see you.

Always a pleasure, mate. Always a pleasure. So how would you frame the US markets right now? We’ve seen repeated new highs for the S&P 500 and the tech heavy NASDAQ. Can we expect things to keep ascending into uncharted territory? Is everything as it seems?

Well, we’ve seen 30 daily closing highs at new records for the S&P 500 so far in 2024. For the record, Andrew, most investors might categorize that as bullish. We haven’t found a lot of all time highs during bear markets and I think there’s a quote from Jesse Livermore that’s really helpful to all of us trend followers, which is, it’s a bull market, you know.

And what he meant behind that quote was that it is human nature. For all of us to second guess a good thing, to want to call the top, to get out before you give back any gains, to be the first one to spot the, the potential free fall that will come next.

It’s kind of I told you so, isn’t it?

Exactly. The smartest people in the room are always the short sellers, right? Even when they’re, losing money hand over fist, as markets climb a wall of worry. I’m not in any position to tell you what happens beyond the right side of the chart, and I think one of the great gifts that technical analysis gives investors is the idea of focusing your attention on what is happening in the here and now, observing correctly, what is actually taking place?

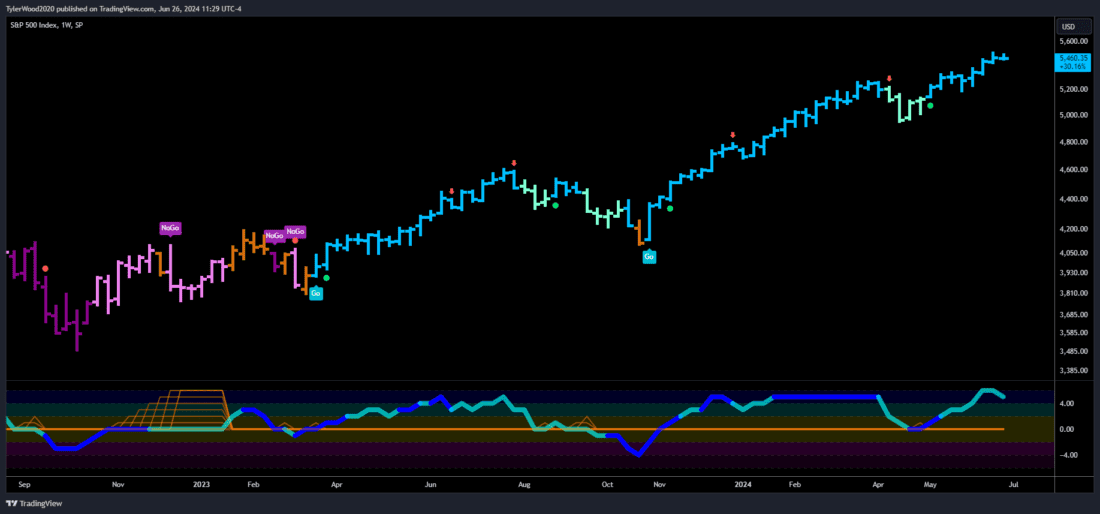

And if investors simply recognize what’s right in front of them, that helps you make decisions reacting responsibly to what the market is telling you. So, you mentioned tech versus the rest of the market, the information technology sector, industry groups such as semiconductors, computer hardware, and even, renewable energy equipment have been really strong, absolute performers, but also relative performers. Those industry groups relative to the sector, that sector relative to the rest of the market. and lots of analysts have been commenting that market breadth has been very narrow, right? We know that, a deeper bench strength makes a better championship team. So when we see equities closing out at all time highs, you want to know if, that’s just a few star performers or if the rest of the market is participating in that move.

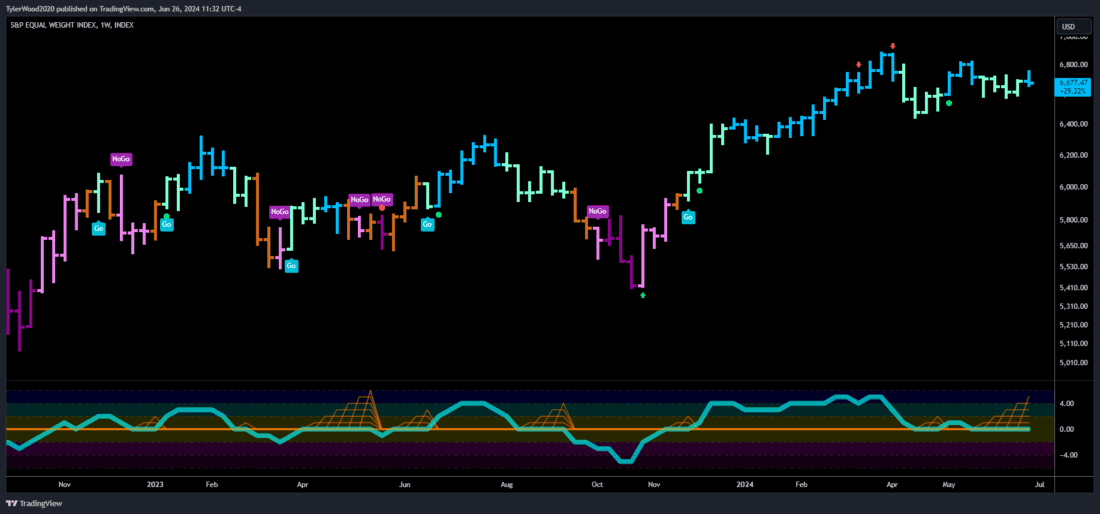

So as recent as just this last week of June, We’ve seen some signs of rotation in that leadership. A day down for information technology and a lot of outperformance from sectors, in the cyclical areas like energy and financials. but one tool that a lot of investors, might get a different view on the market health, is to just look at the equal weighted index, so that strips out the influence of mega cap names that have been performing so well.

That equal weighted index of the S&P 500 is not an all bad story. It certainly, doesn’t, boast the incredible bull market that we have seen, for the top line index, like the S&P 500. But if you’re looking at it on an equal weight basis, things are pretty healthy and in very early innings for the average stock within the index. So that’s, how I’d answer your question. I think we’re, just beginning, to see some breakouts across the average stock.

I wanted to ask you about Nvidia? Is this artificial elephant in the room? It’s an interesting story and you just answered that initial question talking about equal weighting. So, NVIDIA’s got so large, a lot of people worried about what happens to it. You know, maybe where goes NVIDIA goes the market, perhaps? I don’t know. What can you tell us?

Right to be, shocked by the size of this company, 3.4 trillion dollars. I think I read the other day, the single security NVIDIA is actually larger than the stock markets of Germany, France and the UK. The only stock markets that are larger by market cap than NVIDIA are China, Japan, India, and of course the US. So that’s record breaking, it’s noteworthy, it’s newsworthy, but I guess I would draw people’s attention, that NVIDIA has had an incredible run, not just as a high performing company in the semiconductor space, but perhaps also fueled by investor sentiment around this AI revolution. I’m not here to comment on whether human nature is a good thing or a bad thing, but it’s pretty consistent and you can go back to, you know, the 1920s. RCA stock rose from $5 and 80 cents in 1921 to $420 in 1928. Split five for one in March of ’29, and peaked at a $114.75 per share in September of 1929. And that was right before beginning its 98 percent decline to 2.50 a share in May 1932. Now, does NVIDIA follow the same path? That’s for anybody to guess at.

What we would think about as technical analysts is how do you react responsibly? I, use some trend models, a blend of lots of indicators, and they show on a weekly timeframe that this recent decline. Is registering simply as a pullback with an otherwise healthy uptrend. So if we’re looking at a weekly time frame, this is all fair and orderly in an otherwise, healthy uptrend. And I look to a blend of momentum tools to understand any leading indication of trend exhaustion. That’s the other aspect of technical analysis and something that investors learn through the CMT program is, how you blend a mosaic of tools. Obviously, we want to identify trend when it breaks specific levels, when price falls below a historic moving average. Those are telltale signs that trend has, reached some exhaustion and, perhaps even, corrected or counter trend action. But momentum provides a leading indication of trend exhaustion before it begins to really roll over. So when you hear TikTok traders or newbies to the market talking about, just buy the dip, you know, that’s very irresponsible.

Dips become corrections, which become counter trend moves and reversals, over time. What we would look for is a way to quantify whether or not, a correction or a dip is a viable opportunity and so we looked at momentum. Right now that’s cooling from overbought levels down towards a neutral zero level. And that’s the, leading indicator that I pay most close attention to is when that oscillator comes to the zero line and finds support, moves back into positive momentum. That’s a healthy opportunity to re enter or to add to position size, you know, whatever your risk tolerance and timeframe is, but that’s the indication that trend is healthy enough to continue. It’s a confirmation of trend continuation for me and my team.

So let’s go from the elephant to the other end of the spectrum. What about the small caps? We talked about this last time round, and I think you were pretty constructive on small caps. Tell us about the Russell.

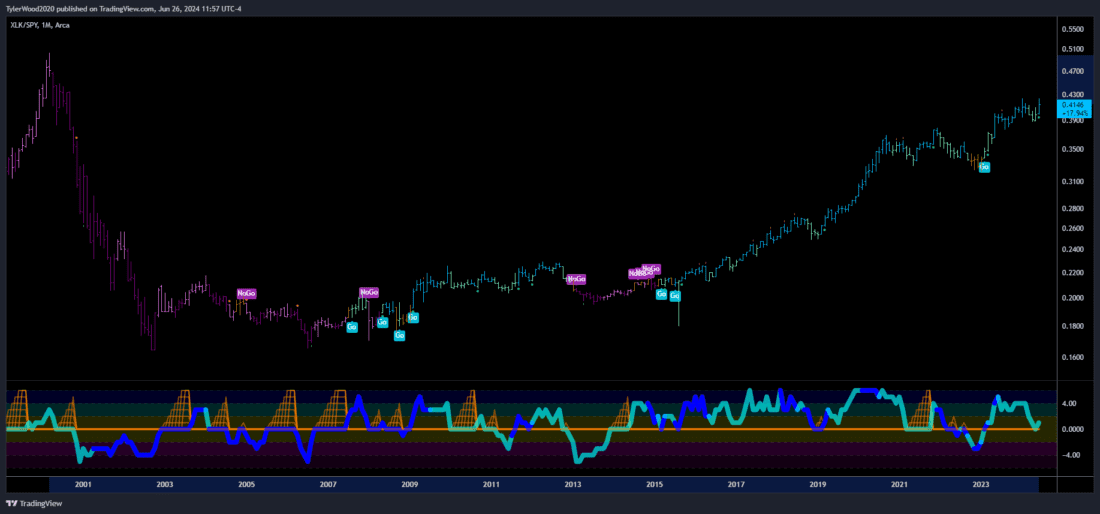

Yeah, and just before we go to, the Russell 2000, I think there are a lot of commentators, trying to capture what could be a repeat of the 1999 tech bubble, right? Everybody is seeing technology outperform and that’s kind of where our conversation started. I would just point out that relative to the S&P 500, the technology sector has yet to reclaim the peaks from March of 2001.

That peak in 2001 is roughly 20 percent higher from where we are now. So, it’s expensive to be early, and I think we should all keep in mind that markets can stay irrational a lot longer than we can stay solvent. So, whether we’re just talking about semiconductors or NVIDIA specifically, or the wider information technology sector, I don’t think it’s a bad thing that large caps have been leading. I don’t think it’s a bad thing that, growthy areas of the market, you know, if it’s a risk on, behavior, then you would like to see communications, technology, consumer discretionary, kind of leading the charge. but now onto small caps, Andrew. I saw, you know, as most people did that those lows in October of ’23, as an opportunity for. the reemergence of a bullish market regime. And so, small caps have underperformed relative to their large cap, counterparts. But, the Russell right now is out of this, sort of sideways, range bound, choppy channel that we saw from, you know, roughly, the beginning of 2022 through those October lows in 2024. So we’re elevated above that trend channel, all of our trend models put those in a positive category. It’s trending, trending higher and we see positive momentum continuing to find support at zero. We’re not seeing divergences to negative momentum, at least on that weekly timeframe.

What I would like to see, to, really get bullish on small caps is for the Russell to, get back to those 2021 highs. And remember there was that. really dramatic channel in 2021, we had a fake out to the upside in October. It caught a lot of investors off guard, because we all got bullish. We all saw the breakout. And then of course it, it reversed and trended lower, substantially. So think about what that does to sentiment. If people have been burned, their portfolios have seen, dramatic reductions in the, accuracy curve because of bad bets on small caps, they’re, reticent to participate, right?

Bull markets are born on a lot of pessimism. People don’t believe that it can happen. So, getting above this, you know, these current levels getting back to those highs in 2021 and a proper follow through of the breakout would be incredibly bullish for small caps, but also that’s going to be breadth expansion for equities broadly in the US.

Tell us about what’s doing well and what’s doing badly. What’s stalling in the current lull?

Yeah, I do, I do a lot of scanning and screening. Another beautiful element of technical analysis is you can, you can form an opinion. You can look for things, across thousands of securities, with relative ease. It’s, It’s very different than doing deep financial statement analysis on each of the companies. So, my belief is that the market is the best fundamental analyst , on the planet, compiling all the information that we know and all those things that we don’t know. So things that are breaking out that were surprising to me, just in the last week, seeing some cruise lines, moving a lot higher.

I myself am not a cruise line kind of a person with our family vacations but, certainly post COVID, they, they suffered dramatically and they are breaking out again. We’ve seen, some biotech names, really exploding to the upside. I think healthcare is in an interesting spot, given, how it has pulled back and, perhaps lower valuations than, what investors are seeing in the tech space and semiconductors, certainly. So, you know, I think the areas to be watching in this market are for that rotation. There’s a lot of, divergence, I guess, between leaders and laggards, even within sectors and industry groups. So taking a look at, a more concentrated portfolio, doing some individual work on stock picking, I think is going to benefit investors.

So those divergences between big names in the financial services industry. If you pick the right one that is trending higher, that adds a lot of value to the portfolio. So, there’s a wide range of and diversified stocks that are breaking out. Some of the areas where I’ve seen things really breaking down, in the industrials and materials space. You’ve got a lot of those, darlings of 2024, what we came into this year, seeing leadership from the cyclical sectors. They’ve really been beaten down. And within the communication space, I’m looking at a lot of publishing companies. News media, is an interesting one, particularly in an election year. Rishi Sunak coming out with a surprise, election next week. I think there’s just a lot more, gains happening in some of those publishing names.

Very good. So where, does that leave us for the rest of 2024? Are you seeing anything in the charts that will, that that are offering telltale signs for the next direction? Whether it’s continued strength across the broad market or you know, signs of worry?

I find myself agreeing with a lot of the technical analysts on the street, which are often saying that the overall, the primary trend of markets is higher, we’re in a bullish regime, that doesn’t mean, we couldn’t be entering a period of more volatility. And rotation itself, is volatile, right? We’re seeing pullbacks and things that were leadership and breakouts and things that have been beaten down.

What I, you know, the process that I follow and that most technical analysts, certainly all CMTs are following is this idea of a top down approach. So if we look first across the asset classes, Seeing what the fixed income market is telling us, where interest rates are at, what we might glean from the currency space and whether a strong US dollar is going to be a headwind or tailwind for equities, that’s where we would start. And on the interest rate side, you know, 10 year treasury yields, it looks like we have the opportunity to, move a bit lower, but within an overall structure of something that is, prepared to move a lot higher.

I just had a conversation earlier today with a very reputable, large bond manager and, their team is all looking at, over the next, few years, moving all the way back up to 7 or 8%, on the US 10 year. The timeliness of how we move that high in interest rates, if we move that high, and the nature of why we’re moving higher I think is, really a telltale sign for investors.

If it’s, rapid and violent in the way that it was in 2020, that’s delivering a lot of uncertainty. That’s runaway inflation, that’s a risk off environment, and rates are rising because, things are really, problematic. But if you look at periods like the 1940s and 50s, a rising interest rate environment is not necessarily the death knell for an equities rally. In fact, rates rose, as did the US stock market during that post war period, because growth was good and it made sense for things to be higher. so I think for me, looking at the back half of 2024, I keep a very close eye. On the, on US interest rates. I think, as everybody does, we can’t help ourselves, but wait on bated breath for more commentary from Chairman Powell and when, potential rate cut, might happen, if any, but I’m not holding out for a rate cut as a necessary, ingredient for the markets to continue to rally. I think we’ve seen strong earnings growth through the first two quarters of this year, and I think that’s helping us continue this upward trend.

Tyler Wood of the Chartered Market Technicians Association. Thank you very much for joining me today.

Thank you so much, Andrew. It’s great to see you. And, will you be back in the UK for, elections next week? Take a little vacation?

No, I’m, going to celebrate with the Americans.

Oh, well, welcome to the club, you know?

I’ve been doing that for 24 years now and I enjoy that holiday every, year.

Fantastic. I do as well. It’s a good time with family and friends.

Great to see you, Tyler, thank you for joining me. And to the audience, don’t forget if you liked today’s episode, please subscribe from wherever you download your podcasts from.

Shared content and posted charts are intended to be used for informational and educational purposes only. The CMT Association does not offer, and this information shall not be understood or construed as, financial advice or investment recommendations. The information provided is not a substitute for advice from an investment professional. The CMT Association does not accept liability for any financial loss or damage our audience may incur.

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Your most comforting Tyler. But … what about Putin?

You skipped the answer about the NVDA question… Hmm…