- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted June 26, 2024 at 9:44 am

The article “When Shorts Don’t Short” first appeared on Alpha Architect blog.

The important role played by short sellers, who, through their actions, keep prices efficient by preventing overpricing and the formation of price bubbles in financial markets, has received increasing academic attention in recent years. Research into the information contained in short-selling activity— for example the 2023 study, “Swim with Sharks: Are Short Sellers More Informed than their Competitors?”—has consistently found that short sellers are informed investors who are skilled at processing information (though they tend to be too pessimistic). That is evidenced by the findings that both stocks exhibiting a higher aggregate short interest ratio in the current month, compared to their counterparts, tend to experience relatively lower future returns and stocks with high shorting fees earn abnormally low returns even after accounting for the shorting fees earned from securities lending (loan fees provide information in the cross-section of equity returns).

Fund families that invest systematically, such as AQR, Avantis, Bridgeway, and Dimensional, have found ways to incorporate the research findings to improve returns over those of a pure index replication strategy. For example, a long-only fund could screen out from their eligible universe stocks with high short interest and/or shorting fees. This will likely become increasingly important as the markets have become less liquid, increasing the limits to arbitrage and allowing for more overpricing.

Xavier Gabaix and Ralph Koijen demonstrated in their 2021 study, “In Search of the Origins of Financial Fluctuations: The Inelastic Markets Hypothesis,” markets have become less liquid and thus more inelastic. Gabaix and Koijen estimated that $1 in cash flows results in an increase of $5 in valuations. One explanation for the reduced liquidity is the increased market share of indexing and passive investing in general. Reduced liquidity increases the risks of shorting.

Adding further to the risks is the now-demonstrated ability of retail investors to “gang up” against shorts (who might be right in the long term but dead before they reach it). The first GameStop episode (January 2021) in which retail investors banded together to engineer a short squeeze (which drove the price of the stock up almost 30 times) demonstrated just how risky shorting can be, with the potential for unlimited losses. A repeat short squeeze occurred in May 2024 with short sellers losing more than $2.2 billion as the stock rose 60% on the 13th and another 120% in premarket trading on the 14th. The result is that the limits to arbitrage have now increased, allowing for more overpricing of “high sentiment” stocks, making the market less efficient.

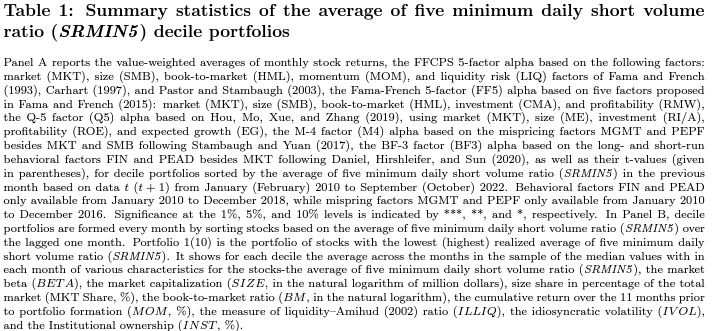

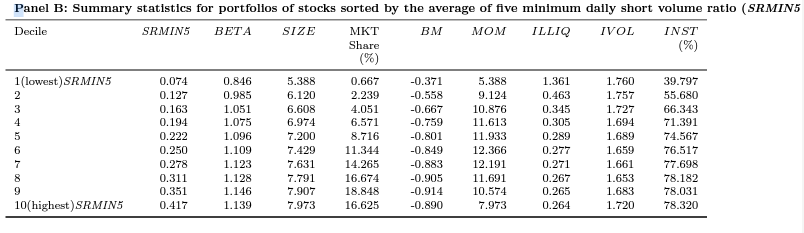

An interesting question is: What happens when the informed short sellers don’t short? Yifeng Zhu sought the answer to that question in his January 2024 study “When Short Sellers Do Not Short…” He introduced a metric for extremely low short volume for individual stocks based on the daily short volume of the month, denoted as SRMIN (the minimum daily short volume ratio) and SRMIN5 (the average of the five minimum daily short volume ratios for each stock in the month). Zhu collected public news data from Ravenpack, aggregated it on a daily level, and employed daily Fama-MacBeth regressions. He utilized short volume ratios as dependent variables and positive and negative news from the current and previous day as independent variables. He controlled for current and previous daily returns, realized firm size, book-to-market ratio, momentum, turnover ratio, illiquidity, and beta. His data sample covered the period January 2010 to October 2022. The dataset included all common stocks listed on the NYSE, AMEX, and NASDAQ, with a prerequisite of non-missing market capitalization. He also limited his analysis to stocks commencing the month with prices of $5 or more. Following is a summary of his key findings:

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged, do not reflect management or trading fees, and one cannot invest directly in an index.

However, Zhu also found that for the largest 20% of firms, or the most liquid 20% of firms, the alphas associated with the return difference became statistically insignificant.

His findings led Zhu to conclude:

“Stocks with low short volume levels typically coincide with positive public news about future returns. However, investors may underreact to this positive information due to illiquidity, contributing to the significant return difference observed between portfolios with SRMIN5 for at least two months.”

He added: “Only the five days when short sellers do not short carry informative value for future stock returns.” This is the main new finding from his research.

Zhu’s findings demonstrated that extremely low short positions come from positive public news, while negative news can drive average short or extremely high short positions. Consistent with the behavioral finance and momentum literature, his findings suggest that investors underreact to such news due to illiquidity contributing to the return pattern he found. Another key takeaway with implications for portfolio construction is that it is the minimum short volume that holds significance for expected returns. It will be interesting to see if investment firms incorporate these new findings.

Larry Swedroe is the author or co-author of 18 books on investing, including his latest, Enrich Your Future: The Keys to Successful Investing.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

This site provides NO information on our value ETFs or our momentum ETFs. Please refer to this site.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Alpha Architect and is being posted with its permission. The views expressed in this material are solely those of the author and/or Alpha Architect and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Trading on margin is only for experienced investors with high risk tolerance. You may lose more than your initial investment. For additional information regarding margin loan rates, see ibkr.com/interest

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

1000