- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted March 26, 2025 at 1:28 pm

The post “Understanding Financial Inclusion in the United States” first appeared on Alpha Architect blog.

This article explores how many American households have retirement and bank accounts, focusing on those with lower incomes. It highlights the challenges faced by low-income families in accessing financial services and discusses how policies like automatic enrollment in retirement plans could improve financial inclusion.

Targeted Outreach: Focus efforts on low-income communities to educate and encourage participation in retirement and banking services.

Employer Collaboration: Work with employers to establish or enhance retirement plans, especially those featuring automatic enrollment, to boost employee participation.

Customized Solutions: Develop financial products tailored to the needs of low-income households to promote greater financial inclusion.

“I understand that saving for the future can feel overwhelming, especially when money is tight. But even small steps can make a big difference. If your job offers a retirement plan, I can help you enroll and explain how employer contributions can boost your savings. If you don’t have a plan at work, we can explore low-cost retirement options that fit your budget. I can also help you find a bank account with no or low fees to keep more of your money working for you. My goal is to make managing your money easier and set you up for a more secure future—one step at a time.“

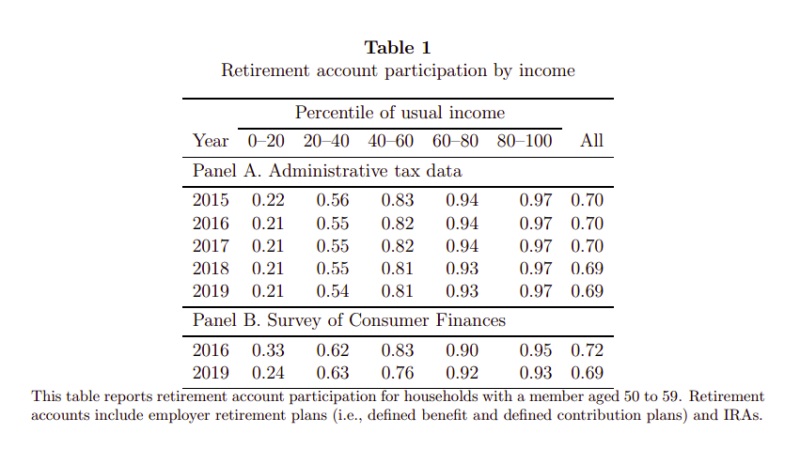

This table reports retirement account participation for households with a member aged 50 to 59. Retirement accounts include employer retirement plans (i.e., defined benefit and defined contribution plans) and IRAs.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

We study retirement and bank account participation for the universe of U.S. households with a member aged 50 to 59 in the administrative tax data. ZCTA-level average income, income inequality, and racial composition predict retirement account participation for low-income households, conditional on household income and regional price parities. Income inequality also predicts bank account participation for low-income households. We estimate the causal effect of access to an employer retirement plan on participation. Recent policy proposals for universal access with automatic enrollment could increase participation by 19 percentage points in the lowest income quintile over ten years.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

This site provides NO information on our value ETFs or our momentum ETFs. Please refer to this site.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Alpha Architect and is being posted with its permission. The views expressed in this material are solely those of the author and/or Alpha Architect and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Que puedo generar ingresos

Hola, gracias por contactarnos. ¿Podrías aclarar tu pregunta? Ten en cuenta que IBKR no ofrece asesoramiento en materia de inversiones.