- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted November 20, 2024 at 11:11 am

The article “Rethinking Asset Growth in Asset Pricing Models” first appeared on Alpha Architect blog.

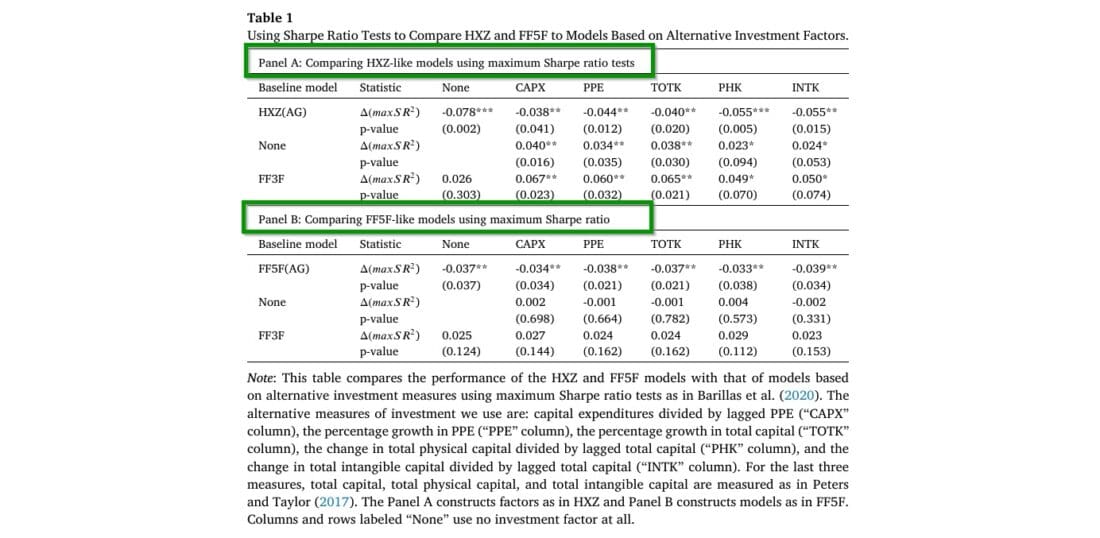

Measures of asset growth add considerable explanatory power to asset pricing models, but wait, there’s a twist. The formulation for measuring asset growth in risk models, such as the 5-Factor Fama-French (FF5F) or the Hou-Xue-Zhang (HXZ), do not necessarily align with traditional measures of firm investment even though they seem to be a good statistical fit. Accordingly, there is one central question in this research: Is asset growth an appropriate and persuasive indicator for investment activity in asset pricing models? The authors argue persuasively that the asset growth factor widely adopted in risk/return models likely misses the mark. Indeed, the performance of the factor models developed by Hou et al. (2015) and Fama and French (2015) were found to be critically dependent on how each constructs the investment factor.

The contribution of this research lies in the examination of the theoretical foundations of widely used risk models that explain the cross-sectional behavior of stock returns. If asset growth is an inappropriate proxy for investment, then it is reasonable to assume that other measures will better reflect the underlying growth characteristics in equity securities. Will those measures be identified?

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

We show that the performance of the new factor models of Hou et al. (2015) and Fama and French (2015) depends crucially on how their investment factor is constructed. Both models use growth in total assets to measure investment. Their ability to price the cross-section of returns decreases significantly when the investment factor is constructed using traditional investment measures, or measures that also account for investment in intangibles. In contrast, we find that factors based on growth in inventory and accounts receivable contain the bulk of the pricing information in the asset growth factor. We show evidence that the superior performance of the asset growth factor seems to be attributable to its ability to capture aggregate shocks to equity financing costs.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

This site provides NO information on our value ETFs or our momentum ETFs. Please refer to this site.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Alpha Architect and is being posted with its permission. The views expressed in this material are solely those of the author and/or Alpha Architect and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!