- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted November 20, 2019 at 9:45 am

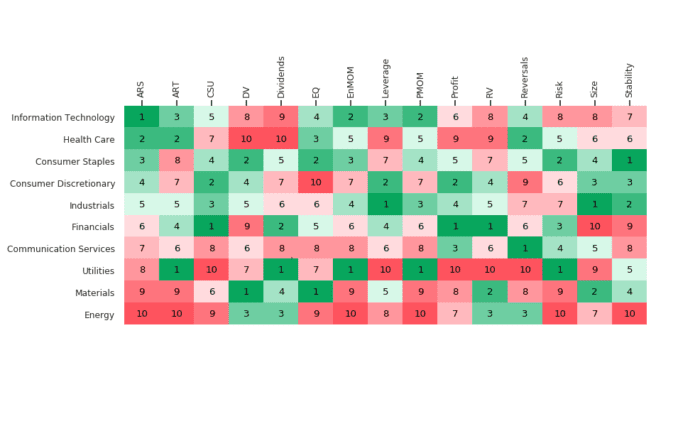

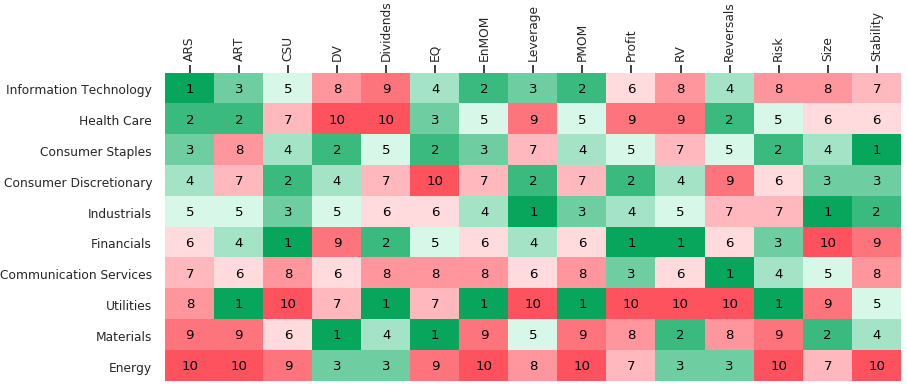

The Sector ranks table (based on bottom up aggregation of QMIT Enhanced Smart Betas within sectors) allows for sector rotation based on factors. The cross-sectional factor rank correlations tell us how correlated the factors are at this juncture vs recent 3y return correlations vs LTD (20y) return correlations. It’s worth noting that cross sectional factor rank correlations are based on today’s alphas across the entire universe while the historical return correlations are only based on the information in the tails (i.e., the 5%-tile spread returns). Further, as the astute may surmise, one can extract a risk model from our factor covariance matrix which should better align one’s alphas with the risk optimization.

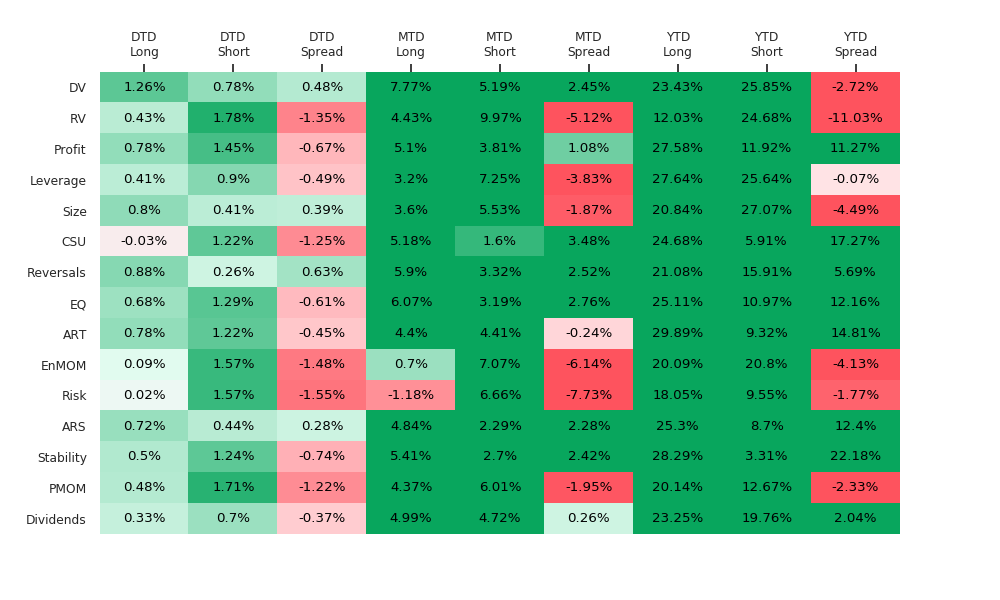

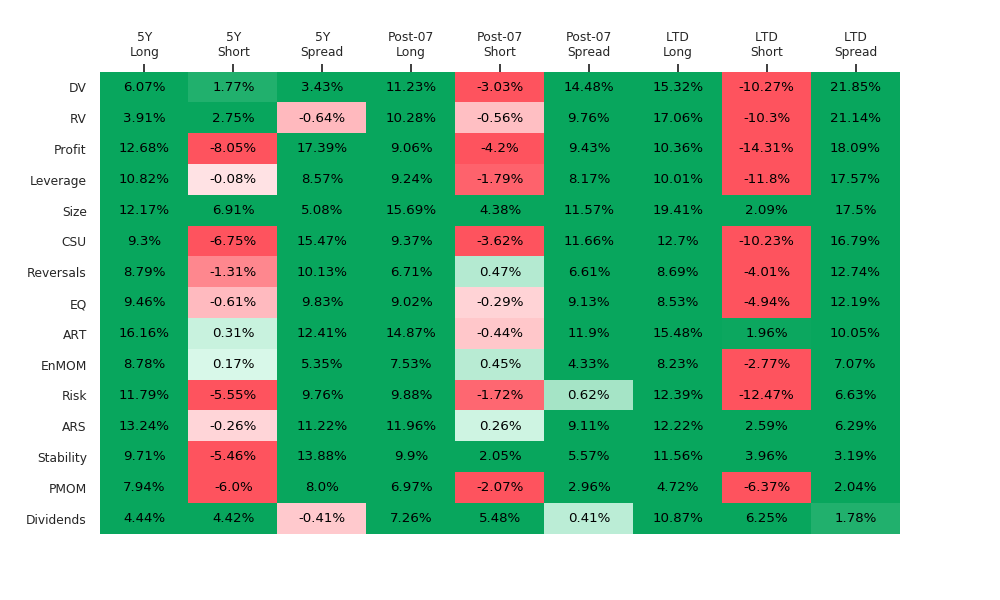

Please find below heatmaps with the DTD, MTD, YTD, 5 year, Post-07 & LTD returns for our ESBs as of last night’s close. Stay tuned for more composite signals on our ESBs which will continue to be added. These spreads are based on the best methodology (defined as highest cumulative return LTD) out of five that are available to clients for each of the ESBs as regards aggregation of factors within the Smart Beta cohorts. Customized heatmaps may be available based on all five methodologies:

Sector ranks based on QMIT Enhanced Smart Betas:

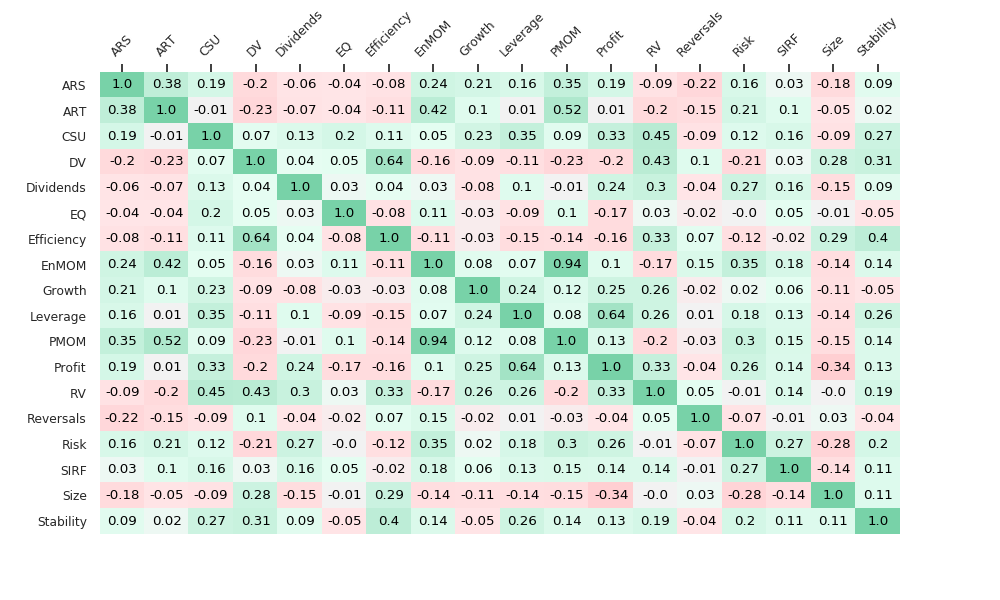

C-S Rank correlations for QMIT Enhanced Smart Betas:

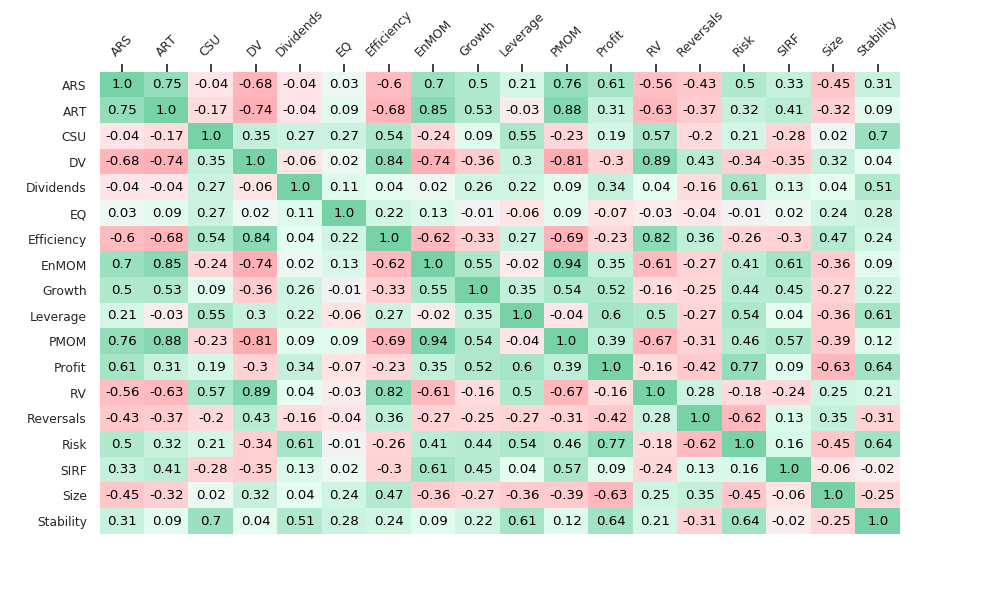

3y Return correlations for QMIT Enhanced Smart Betas:

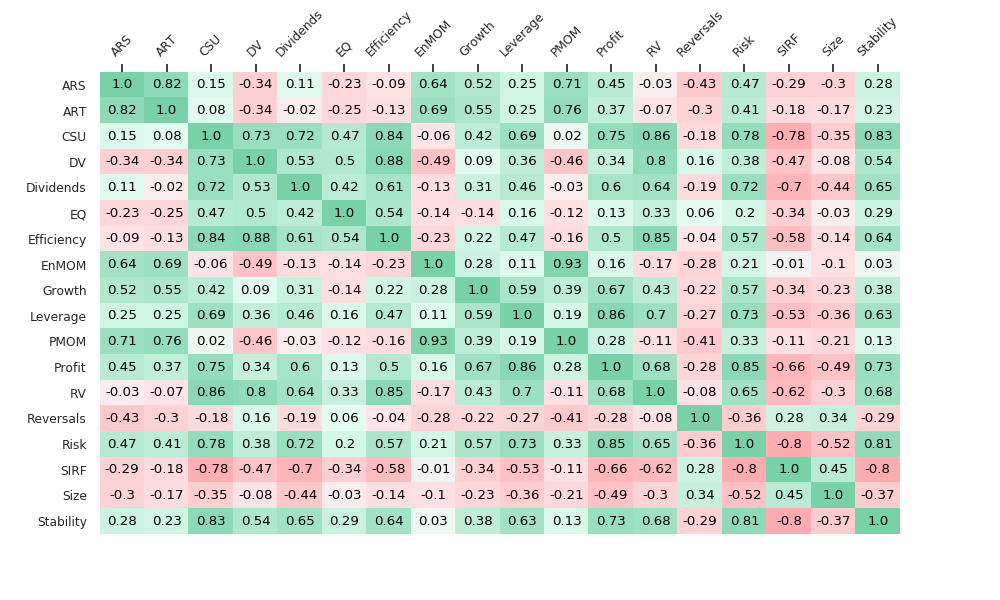

20y Return correlations for QMIT Enhanced Smart Betas:

EXPLANATORY FOOTNOTES:

Enhanced Smart Beta Definitions

ARS: This smart beta composite shows our Analyst Revisions cohort based on

measures of estimate revisions, dispersion, Standardized Unexpected Earnings

surprise (SUE score) & consensus change in both earnings as well as

revenues which can outperform traditional metrics like a 1mo consensus change.

ART: This smart beta composite shows our Analyst Ratings & Targets cohort based on measures of analyst recommendations, target price, changes

& diffusion which can outperform traditional metrics like a 1mo consensus

change.

CSU: This smart beta composite shows our Capital Structure/Usage cohort

based on measures including Buybacks, Total yield, Capex, capital usage ratios

etc which can outperform traditional metrics like Cash/MC.

Dividends: This smart beta composite shows our Dividends related cohort based on

measures including Yield, payout, growth, forward yield etc which can

outperform traditional metrics like Dividend Yield.

DV: This smart beta composite shows our Deep Value (or intrinsic value)

cohort based on measures including tangible book & sales which can

outperform traditional Book yield.

Efficiency: This smart beta composite shows our Efficiency cohort based on

measures including Asset Turnover, Current Liabilities, Receivables etc which

can outperform traditional metrics like Asset Turnover.

EnMOM: This smart beta composite shows our Enhanced Momentum cohort which

can outperform traditional 12 month price momentum in both return & risk

adjusted terms particularly at market inflection points.

EQ: This smart beta composite shows our Earnings Quality cohort based on

a variety of Accrual measures which can outperform traditional metrics like

Total Accruals.

Growth: This smart beta composite shows our Historical Growth cohort based on

a variety of Earnings, Sales, Margins & CF related growth measures which

can outperform traditional metrics like 3yr Sales growth.

Leverage: This smart beta composite shows our Leverage related cohort based on

measures of Balance Sheet leverage which can outperform traditional metrics

like Debt To Equity.

PMOM: This smart beta composite shows our PMOM related cohort which can

outperform traditional 12 month price momentum using a variety of traditional

momentum factors.

Profit: This smart beta composite shows our Profitability cohort based on

measures like ROA, ROE, ROCE, ROTC, Margins etc which can outperform

traditional metrics like ROE.

RV: This smart beta composite shows our Relative Value cohort based on

measures of EPS, CFO, EBITDA etc which can outperform traditional Earnings

yield.

Reversals: This smart beta composite shows our Reversals cohort which is

comprised of metrics like short term reversals, RSI, DMA & other technical

factors which can outperform traditional metrics like a 1 month total return.

Risk: This smart beta composite shows our Risk/ Low Vol cohort which is

comprised of metrics like Beta, Low volatility etc.

SIRF: This smart beta composite shows our Short Interest cohort which is

comprised of metrics related to Short Interest and its normalization by Float,

trading volume etc.

Size: This smart beta composite shows our Size cohort which is comprised of

metrics related to firm size including market capitalization.

Stability: This smart beta composite shows our Stability cohort which is

comprised of metrics like Dispersion of EPS/ SPS estimates as well as the

stability of Margins, EPS & CFs etc.

QMIT is a data provider and not an investment advisor. This information has been prepared by QMIT for informational purposes only. This information should not be construed as investment, legal and/or tax advice. Additionally, this content is not intended as an offer to sell or a solicitation of any investment product or service. Opinions expressed are based on statistical forecasting from historical data. Past performance does not guarantee future performance. Further, the assumptions and the historical data based used could be erroneous. All results and analyses expressed are merely hypothetical and are NOT guaranteed. Trading securities involves substantial risk. Please consult a qualified investment advisor before risking any capital. The performance results for live portfolios following the screens presented herein may differ from the performance hypotheticals contained in this report for a variety of reasons, including differences related to transaction costs, market impact, fees, as well as differences in the time and price of execution. The performance results for individuals following the strategy could also differ based on differences in treatment of dividends received, including the amount received and whether and when such dividends were reinvested. We do not request personal information in any unsolicited email correspondence from our customers. Any correspondence offering trading advice or unsolicited message asking for personal details should be treated as fraudulent and reported to QMIT. Neither QMIT nor its third-party content providers shall be liable for any errors, inaccuracies or delays in content, or for any actions taken in reliance thereon. QMIT EXPRESSLY DISCLAIMS ALL WARRANTIES, EXPRESSED OR IMPLIED, AS TO THE ACCURACY OF ANY THE CONTENT PROVIDED, OR AS TO THE FITNESS OF THE INFORMATION FOR ANY PURPOSE. Although QMIT makes reasonable efforts to obtain reliable content from third parties, QMIT does not guarantee the accuracy of or endorse the views or opinions given by any third-party content provider. All content herein is owned by QuantZ Machine Intelligence Technologies and/ or its affiliates and protected by United States and international copyright laws. QMIT content may not be reproduced, transmitted or distributed without the prior written consent of QMIT.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from QMIT – QuantZ Machine Intelligence Technologies and is being posted with its permission. The views expressed in this material are solely those of the author and/or QMIT – QuantZ Machine Intelligence Technologies and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!