- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted December 2, 2020 at 11:10 am

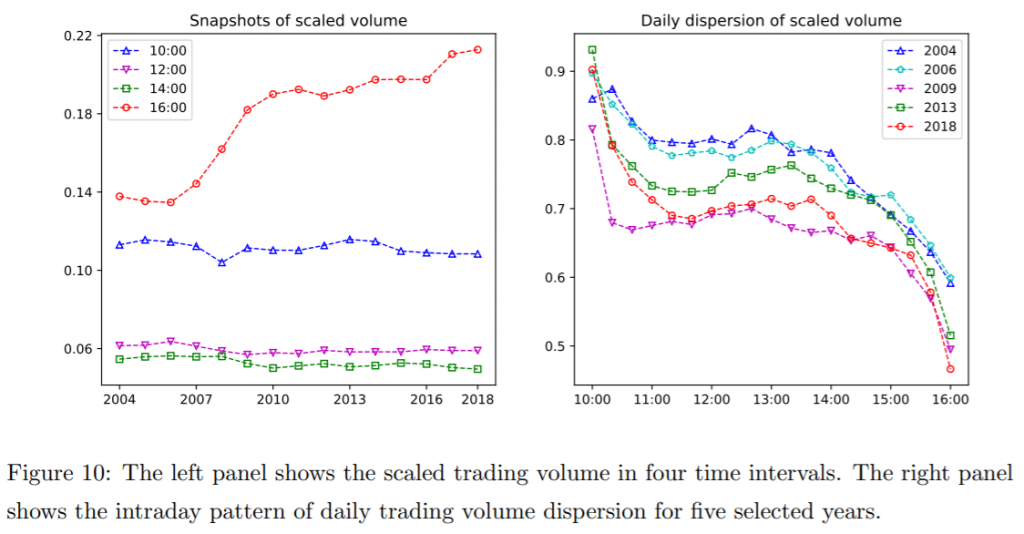

In recent years, financial markets have experienced a boom in passive and index-based strategies, which could have caused a change in the trading volume, volatility, beta or correlations. The reason is straightforward: the index investing causes a lot of stocks to move in the same direction. A novel research Shen and Shi (2020), using high-frequency data, suggests that over the last two decades, the patterns mentioned above have changed and the index investing is the cause. Both the trading volume and stock correlations are increased at the end of trading sessions. Betas are firstly dispersed, but in general, converge to one during the rest of the day. Trading volume has high dispersion at the market open, but low dispersion at the market close. Overall, the paper has many important implications for portfolio managers, risk managers and traders as well since it is closely related to the transaction costs, intraday price fluctuations, correlations or liquidity. Moreover, it is full of exciting charts that are worth seeing.

Authors: Yiwen Shen and Meiqi Shi

Title: Index-based Investing and Intraday Stock Dynamics

Link: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3696124

Abstract:

We investigate how the growth of index-based investing impacts the intraday stock dynamics using a large high-frequency dataset, which consists of 1-second level trade data for all S&P 500 constituents from 2004 to 2018. We estimate intraday trading volume, volatility, correlation, and beta using estimators that are statistically efficient under market microstructure noise and observation asynchronicity. We find the intraday patterns indeed change substantially over time. For example, in the recent decade, the trading volume and correlation significantly increase at the end of trading session; the betas of different stocks start dispersed in the morning, but generally move towards one during the day. Besides, the daily dispersion in trading volume is high at the market open and low near the market close. These intraday patterns demonstrate the implication of the growth of index-based strategies and the active-open, passive-close intraday trading profile. We theoretically support our interpretation via a market impact model with time-varying liquidity provision from both single-stock and index-fund investors.

As always, the results can be presented through interesting charts:

Visit Quantpedia to read Notable quotations from the academic research paper:

https://quantpedia.com/novel-market-structure-insights-from-intraday-data/

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Quantpedia and is being posted with its permission. The views expressed in this material are solely those of the author and/or Quantpedia and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!