- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted May 12, 2026 at 11:12 am

The article “Institutional Investor Attention” was originally published on Alpha Architect blog.

Institutional investors are supposed to process information efficiently, read everything that matters, and adjust portfolios rationally. But in practice, attention is scarce. Funds must choose what to read, when to read it, and whether to focus on macro conditions or individual firms. This paper opens that black box. Using direct data on what institutional investors actually read online, it shows that attention is a real economic resource. Funds that reallocate attention toward macro news when volatility rises perform better. Funds also pay more attention to the stocks they own, and that attention helps them make more valuable position and trading decisions.

Funds shift attention toward macro news when uncertainty rises

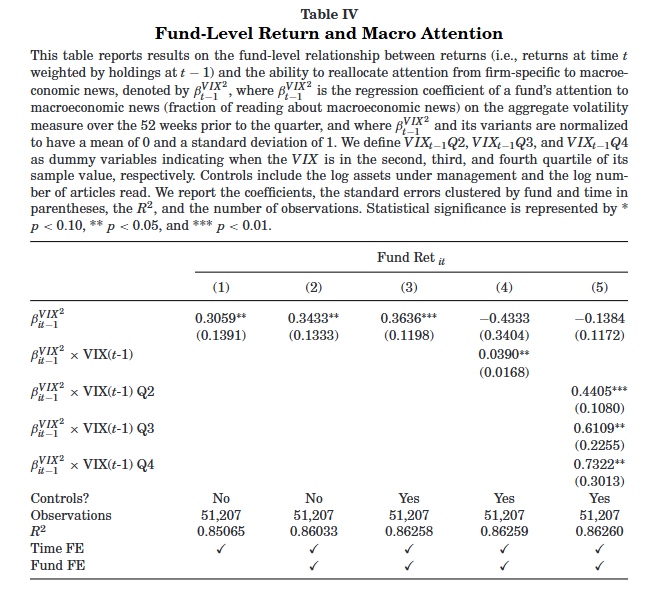

The paper shows that institutional investors reallocate attention toward macroeconomic and aggregate market news when aggregate volatility is high. This is consistent with limited-attention theories, which predict that macro information becomes more valuable during turbulent periods.

Funds that reallocate attention better earn higher returns

A fund’s ability to shift attention toward macro news when volatility rises predicts better future performance. Funds with higher macro-attention sensitivity outperform by about 0.48% per quarter, or roughly 1.9% annualized, and that outperformance is strongest when aggregate volatility is high.

Attention and portfolio holdings are closely linked

Funds pay much more attention to stocks they already hold than to stocks they do not hold. On average, they read about held stocks around five times more than non-held stocks, and within portfolios, larger positions receive more attention. This supports the idea that investors concentrate attention where they expect it to matter most.

Firm-specific attention adds value to positions

Attention to a stock predicts greater position-level value-add. Stocks that receive more attention contribute more to future portfolio performance, especially when the fund already holds a large position or is making a meaningful trade.

Attention improves trading decisions, especially buys

Fund attention to a stock is positively associated with trade-based value-add. In other words, attentive trading is more profitable. This effect is especially strong for buys rather than sells, consistent with the view that buying decisions require more information production than selling decision.

Attention from sophisticated investors predicts future returns

At the stock level, attention by buying funds predicts future returns, especially when the attention comes from hedge funds. Stocks that attract more attentive buying subsequently outperform, suggesting that investor attention helps move information into prices, but not immediately.

Treat attention as an investment resource

Investment skill is not just about security selection. It is also about where to allocate limited research capacity. The paper suggests that better managers direct attention toward the most decision-relevant information at the right time.

Watch process, not just outcomes

Managers who can shift focus toward macro conditions during high-volatility periods may have a more adaptive investment process. That flexibility appears tied to better performance.

Use conviction and attention together

The paper shows that attention is most valuable when paired with meaningful position size or meaningful trades. In practice, that suggests investors should focus deepest research effort where conviction and capital commitment are highest.

Separate useful information from noise

Attention to business and financial news creates more value than attention to retail-oriented or general news. That reinforces the importance of filtering signal from noise in portfolio management.

“Successful investing is not just about having access to information. It is about knowing where to focus limited attention. This research shows that better institutional investors shift their focus toward big-picture macro risks when markets become more volatile, and toward the individual stocks that matter most in their portfolios. That attention appears to improve both portfolio construction and trading decisions”

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Using data on Internet news reading, we measure fund-level attention to both aggregate and firm-specific news and relate it to fund portfolio allocation decisions. In the time series, we find that funds shift attention toward macroeconomic news during periods of high aggregate volatility. Those funds that exhibit stronger attention-reallocation patterns earn higher future returns. In the cross-section of fund portfolios, fund attention is positively related to stock holdings. Furthermore, fund attention to a stock increases the value-add of that position to the fund’s performance. This relationship is stronger using fund attention to more value-relevant news articles.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

This site provides NO information on our value ETFs or our momentum ETFs. Please refer to this site.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Alpha Architect and is being posted with its permission. The views expressed in this material are solely those of the author and/or Alpha Architect and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Hedge Funds are highly speculative, and investors may lose their entire investment.

Mutual Funds are investments that pool the funds of investors to purchase a range of securities to meet specified objectives, such as growth, income or both. Investors are reminded to consider the various objectives, fees, and other risks associated with investing in Mutual Funds. Please read the prospectus accordingly. This communication is not to be construed as a recommendation, solicitation or promotion of any specific fund, or family of funds. Interactive Brokers may receive compensation from fund companies in connection with purchases and holdings of mutual fund shares. Such compensation is paid out of the funds' assets. However, IBKR does not solicit you to invest in specific funds and does not recommend specific funds or any other products to you. For additional information please visit https://www.interactivebrokers.com/en/index.php?f=1563&p=mf

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!