- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted March 18, 2026 at 11:50 am

Refined academic research note (with charts, methodology, and references)

Data window: 2025-02-24 to 2026-02-20 • N=238 daily observations

Disclosure & limitations. This note is for educational/informational purposes. Results are computed from a single return series provided by the author and are not audited. Statistics are computed on daily returns with a zero risk‑free rate assumption unless stated otherwise; transaction costs, financing, slippage, taxes, and borrow costs are not included. Past performance is not indicative of future results.

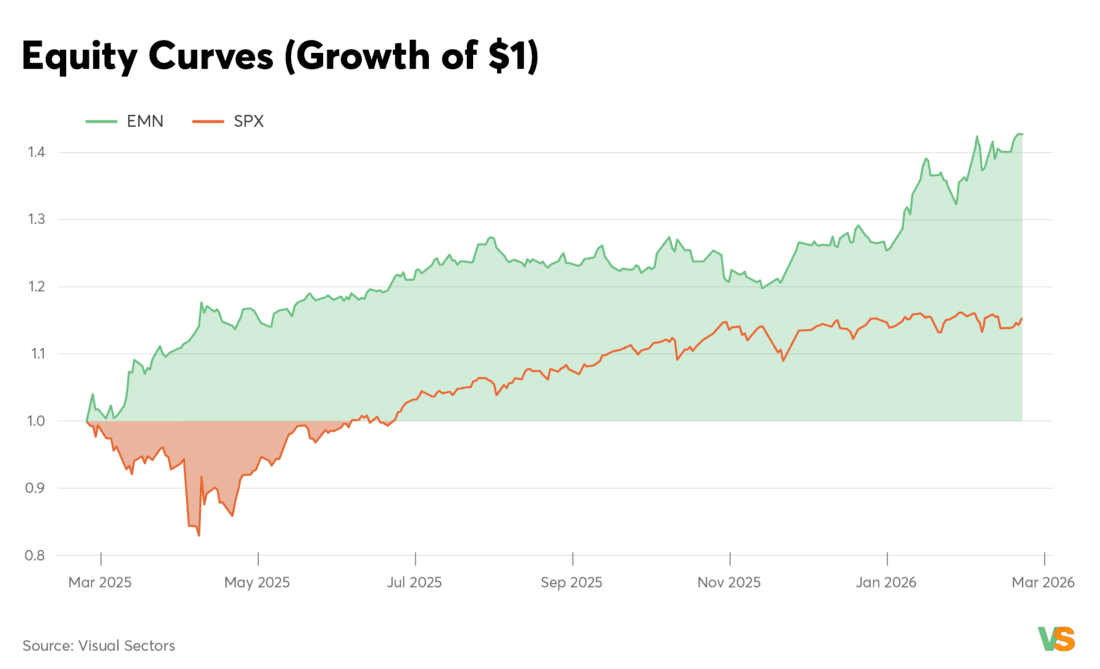

We evaluate an Equity Market Neutral (EMN) long/short portfolio against SPX using 238 daily observations from 2025‑02‑24 to 2026‑02‑20. Across the sample, EMN exhibits higher risk‑adjusted performance and lower drawdown than the equity benchmark. EMN achieves an annualized Sharpe ratio of 2.54 versus 0.83 for SPX, with cumulative returns of 42.8% versus 14.9%. Path and tail risk metrics are also favorable: EMN’s maximum drawdown is −6.0% versus −16.9% for SPX, and its historical 1‑day VaR95 is −1.27% versus −1.70%. At lower frequency, EMN wins 69.2% of weeks and 69.2% of months (SPX: 53.8% and 61.5%). Diagnostics show low market dependence (beta≈0.16, correlation≈0.21) and no statistically significant daily return autocorrelation over 20 lags.

Equity market neutral strategies are typically evaluated not primarily on raw returns, but on their ability to deliver diversifying, risk-efficient performance with limited dependence on equity market direction. This note therefore emphasizes (i) risk-adjusted performance (Sharpe, information ratio), (ii) downside and tail risk (drawdown, VaR and CVaR), and (iii) time-series diagnostics (autocorrelation and rolling behavior).

The specific hypothesis examined is that an EMN portfolio built from DEX-derived support/resistance levels and additional options-flow confirmation can produce (a) attractive risk-adjusted returns and (b) a smoother path than long-only equity exposure, while maintaining low beta to SPX.

Because performance metrics can be sensitive to sampling window, parameter choices, and market regimes, the results should be interpreted as a descriptive analysis of the provided period. The natural next step in a formal due diligence process would be multi-year analysis and out-of-sample validation.

The EMN portfolio is a systematic long/short equity strategy that combines (i) dealer-exposure-derived (DEX) support/resistance levels and (ii) signed options-flow information to select and size positions. The design goal is to reduce directional market exposure while extracting alpha from microstructure-linked flows and price-level effects.

Positions are selected and sized using the following rules:

Volatility-based sizing can be implemented in many ways. A common approach is inverse-volatility weighting:

w_i ∝ 1 / σ̂_i

where σ̂_i is an estimate of recent realized volatility (e.g., 20–60 trading days). This targets a more uniform risk contribution across positions and helps prevent a small subset of high-volatility names from dominating portfolio risk. From a practical standpoint, volatility sizing also tends to ‘auto-delever’ during turbulence if volatility estimates react quickly.

“Managed portfolios that take less risk when volatility is high … increase Sharpe ratios.”

— Moreira & Muir (2017), Volatility‑Managed Portfolios

DEX levels are derived from options positioning and the hedging mechanics of dealers/market makers. Large concentrations of options exposure at particular strikes can induce hedging flows that influence price dynamics as the underlying approaches those levels. When dealers are net long gamma, hedging flows can dampen price moves (range-like behavior); when dealers are net short gamma, hedging can amplify moves (trend/instability).

This mechanism has been studied in academic work linking dealer gamma imbalances to intraday momentum/reversal and volatility regimes. Although practitioners may compute DEX/GEX measures with different conventions (e.g., choice of maturities, dealer sign assumptions, or smoothing), the core intuition is consistent: delta-hedging flows are mechanical, and the sign of gamma changes the stabilizing vs destabilizing nature of those flows.

“We document a link between large aggregate dealers’ gamma imbalances and intraday momentum/reversal of stock returns.”

— Barbon & Buraschi (2021), Gamma Fragility

Options markets are not merely a derivative venue; they are a locus of informed trading and risk transfer. Signed options-flow measures attempt to capture the direction and intensity of demand for delta (directional exposure) or vega (volatility exposure). In EMN, these flows act as a confirmation filter: DEX supplies candidate levels; options flow supplies a directional/regime confirmation.

“Option volume contains information about the future direction of underlying stock price movements.”

— Pan & Poteshman (2006), referenced by Ni, Pan & Poteshman (2008)

“Market neutral” can mean different things operationally. Common implementations include dollar neutrality (equal long and short notional), beta neutrality (estimated beta to the market near zero), and/or sector neutrality (balanced exposures by sector). The 7-long/7-short structure primarily supports dollar neutrality and breadth. To the extent that names have heterogeneous betas, beta neutrality typically requires beta-aware weighting or constrained optimization.

Empirically, the realized beta of EMN vs SPX over the sample is low (≈0.16). This does not prove structural neutrality in all regimes—betas can rise in crises—but it is directionally consistent with the market-neutral objective.

The dataset contains daily simple returns for EMN and SPX over 238 trading days from 2025-02-24 to 2026-02-20. Weekly returns are compounded from daily returns within a Friday-to-Friday week. Monthly returns are compounded within calendar months at month-end.

Unless otherwise stated, the following conventions are used:

Sharpe ratio summarizes average return per unit of total volatility. It is a second-moment metric and therefore compresses the return distribution to mean and variance. Two practical issues arise: (i) fat tails and skew can make variance an incomplete risk descriptor, and (ii) serial correlation can bias standard errors and annualization.

Max drawdown captures path risk: the largest cumulative loss from a prior peak. Drawdown is particularly important for leveraged or capacity-constrained strategies, because a sufficiently deep drawdown can trigger forced deleveraging.

VaR summarizes a quantile of the loss distribution but is not subadditive and does not describe the magnitude of losses beyond the quantile. CVaR (expected shortfall) addresses this by averaging losses in the tail beyond VaR.

Table 1 summarizes the primary statistics computed directly from the supplied return series.

| Metric | EMN | SPX |

| Date range | 2025-02-24 to 2026-02-20 | 2025-02-24 to 2026-02-20 |

| Observations (daily) | 238 | 238 |

| Arithmetic return (ann.) | 38.92% | 16.74% |

| Volatility (ann.) | 15.30% | 20.23% |

| Sharpe (ann., rf=0) | 2.54 | 0.83 |

| Cumulative return | 42.82% | 14.92% |

| Max drawdown | -6.02% | -16.87% |

| VaR 95% (1-day, hist.) | -1.27% | -1.70% |

| Weekly win rate | 69.23% | 53.85% |

| Monthly win rate | 69% | 61.54% |

| Avg rolling 3M return (month-end) | 7.43% | 4.71% |

| Autocorrelation lag-1 (daily) | 0.03 | -0.17 |

EMN’s annualized Sharpe ratio (2.54) materially exceeds SPX’s (0.83). Under a simple mean-variance lens, this indicates that EMN delivered substantially more average daily return per unit of realized volatility.

However, Sharpe should not be interpreted as a complete risk measure. If returns are fat-tailed or negatively skewed, a high Sharpe can coexist with large tail losses. This note therefore pairs Sharpe with drawdown, VaR/CVaR, and distribution diagnostics (skewness and kurtosis).

Cumulative return measures total growth over the sample, while CAGR annualizes this growth geometrically. Over the sample, EMN’s cumulative return is 42.82% with a CAGR of 45.84%. SPX’s cumulative return is 14.92% with a CAGR of 15.86%. CAGR is especially relevant for allocators evaluating long-run compounding.

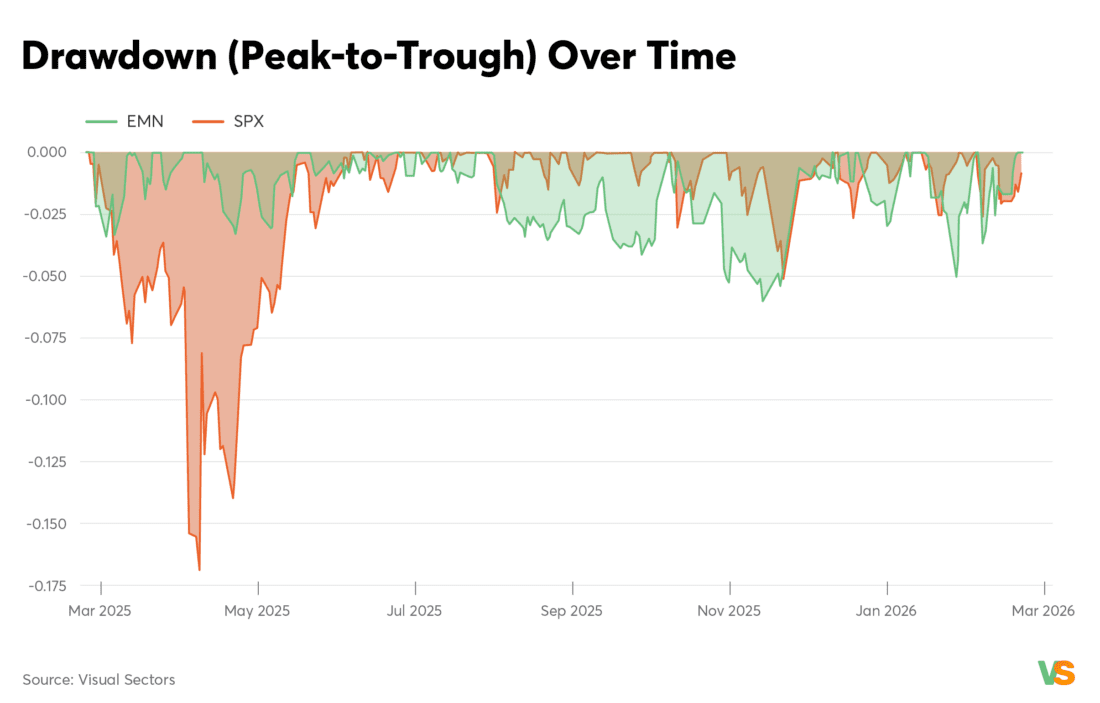

Maximum drawdown captures the worst capital impairment experienced during the sample. EMN’s max drawdown is −6.0% compared with −16.9% for SPX.

Drawdown matters because recovery is nonlinear. A drawdown of d requires a gain of d/(1−d) to recover. For example, a 6% drawdown requires ~6.4% gain to recover, while a 16.9% drawdown requires ~20.3% gain. Strategies with smaller drawdowns can therefore compound more efficiently even if average returns are similar.

EMN’s historical 1-day VaR95 is -1.27%, while SPX’s is -1.70%. Expected shortfall (CVaR95) is -1.75% for EMN and -3.01% for SPX. CVaR is more tail-sensitive because it averages outcomes beyond the VaR quantile.

“Conditional value‑at‑risk … has significant advantages over value‑at‑risk.”

— Rockafellar & Uryasev (2000/2002)

A practical interpretation is that VaR answers “how bad is a typical bad day,” while CVaR answers “how bad are the worst 5% of days on average.” For strategies exposed to gap risk or option-like payoff convexities, CVaR and stress tests are generally more informative than VaR alone.

EMN is positive in 69.2% of weeks and 69.2% of months. SPX is positive in 53.8% of weeks and 61.5% of months. Because win rate ignores magnitude, it is best interpreted together with tail metrics and distributional asymmetry.

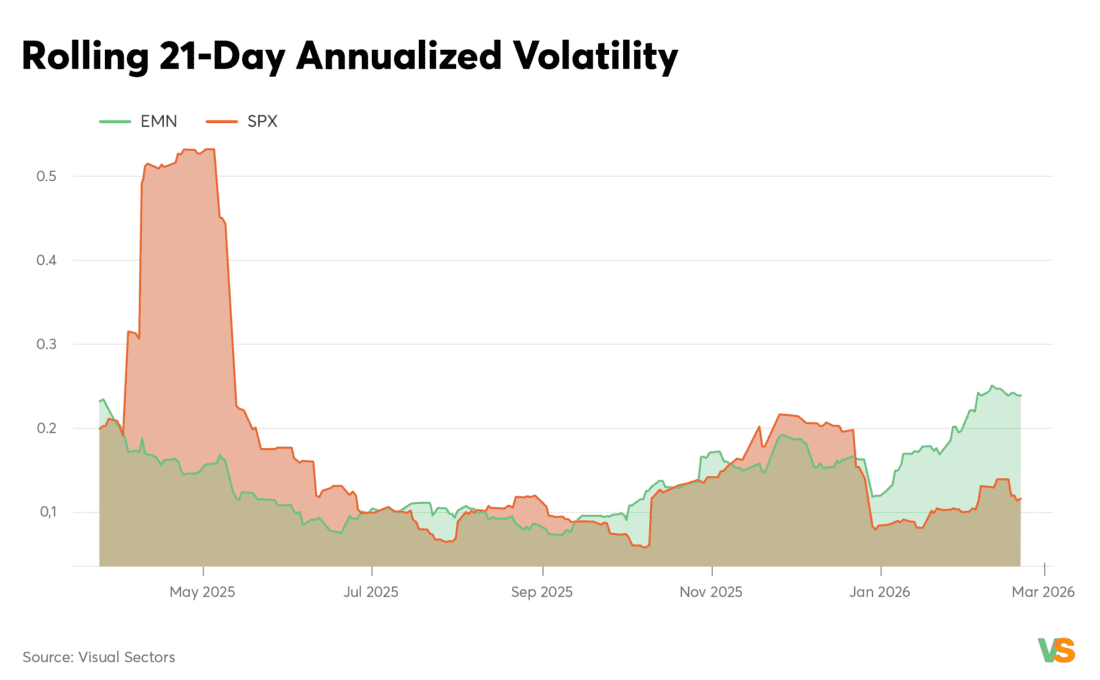

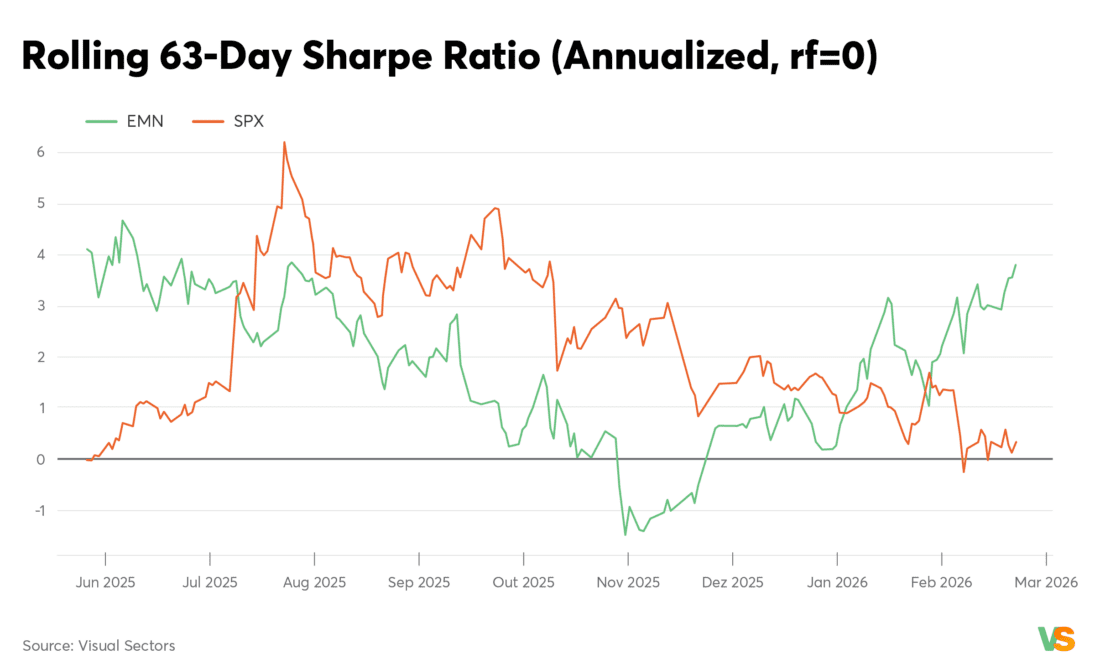

Rolling quarterly returns help reveal whether performance is concentrated in a single short episode or distributed across sub-periods. Rolling volatility and rolling Sharpe provide diagnostics on whether returns were achieved by taking time-varying risk or by maintaining stable risk through time.

Figure 1. Equity curves (growth of $1).

Figure 2. Drawdown paths (peak-to-trough over time).

Figure 3. Rolling 3-month compounded returns (month-end).

Figure 4A. Rolling 3-month return heatmap (EMN, by ending month).

Figure 4B. Rolling 3-month return heatmap (SPX, by ending month).

Figure 5. Rolling 21-day annualized volatility (risk regime).

Figure 6. Rolling 63-day Sharpe ratio (annualized, rf=0).

Table 2 reports additional distribution and downside-risk statistics (computed from the same return series).

| Metric | EMN | SPX |

| CAGR (annualized, geometric) | 45.84% | 15.86% |

| Sortino (ann., MAR=0) | 5.11 | 1.36 |

| Calmar (CAGR / |MaxDD|) | 7.61 | 0.94 |

| CVaR95 (1-day, hist.) | -1.75% | -3.01% |

| Skewness (daily) | 0.47 | 1.43 |

| Excess kurtosis (daily) | 1.28 | 21.06 |

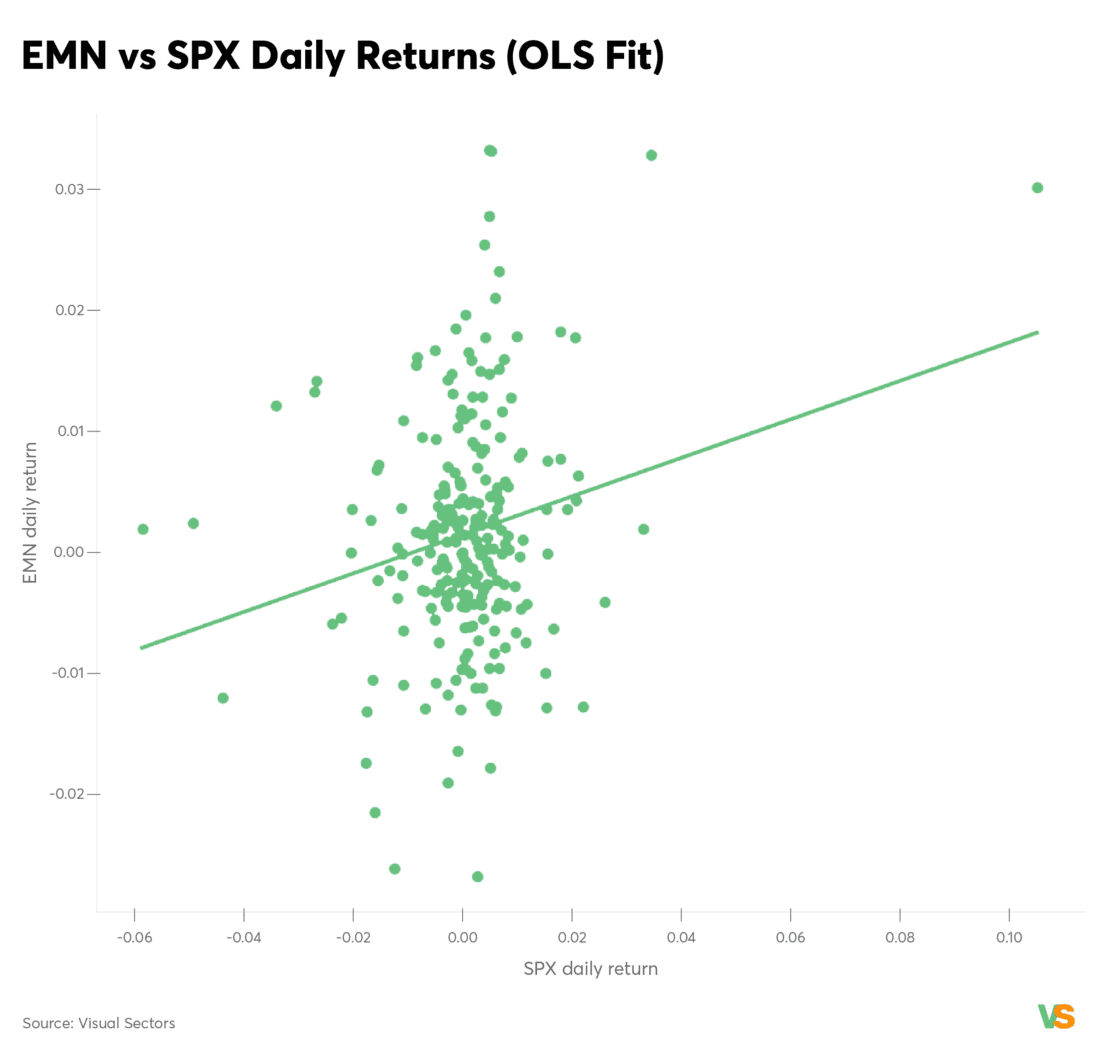

Market-neutral strategies are often assessed by (i) how much market exposure they carry and (ii) how efficiently they generate active returns. We estimate beta and correlation of EMN to SPX on daily returns, and compute the information ratio of EMN relative to SPX.

Estimated beta (EMN vs SPX) is 0.16 and correlation is 0.21. Active returns (EMN − SPX) exhibit an annualized tracking error of 22.66%, an annualized active (geometric) growth rate of 21.68%, and an information ratio of 0.98.

Interpretation: low beta reduces vulnerability to broad market selloffs; the information ratio translates this into an efficiency metric—active return per unit of active risk.

Figure 7. EMN vs SPX daily returns with OLS fit.

Figure 8. Active return (EMN − SPX): growth of $1.

Figure 9. Rolling information ratio of active returns (63 trading day window).

Serial correlation in returns can indicate regime persistence, microstructure effects, or return smoothing. We analyze the autocorrelation function (ACF) up to 20 lags and perform Ljung–Box tests for joint significance.

EMN: no statistically significant autocorrelation is detected (Ljung–Box p‑values: 0.810 at lag 10; 0.848 at lag 20). SPX: autocorrelation is statistically significant over the same horizon (p‑values: 0.002 at lag 10; 0.004 at lag 20).

One interpretation is that SPX exhibits short-horizon mean reversion and volatility clustering, which can generate statistically detectable autocorrelation at daily lags. In EMN, the absence of significant autocorrelation is consistent with a return stream driven by many idiosyncratic moves that do not mechanically repeat day-to-day.

For risk estimation, this matters because serial correlation can bias naïve annualization and understate true uncertainty. Allocators often complement these diagnostics with block bootstrap methods or Newey–West standard errors when formal inference is required.

Figure 10. Autocorrelation of daily returns (ACF) with 95% confidence band.

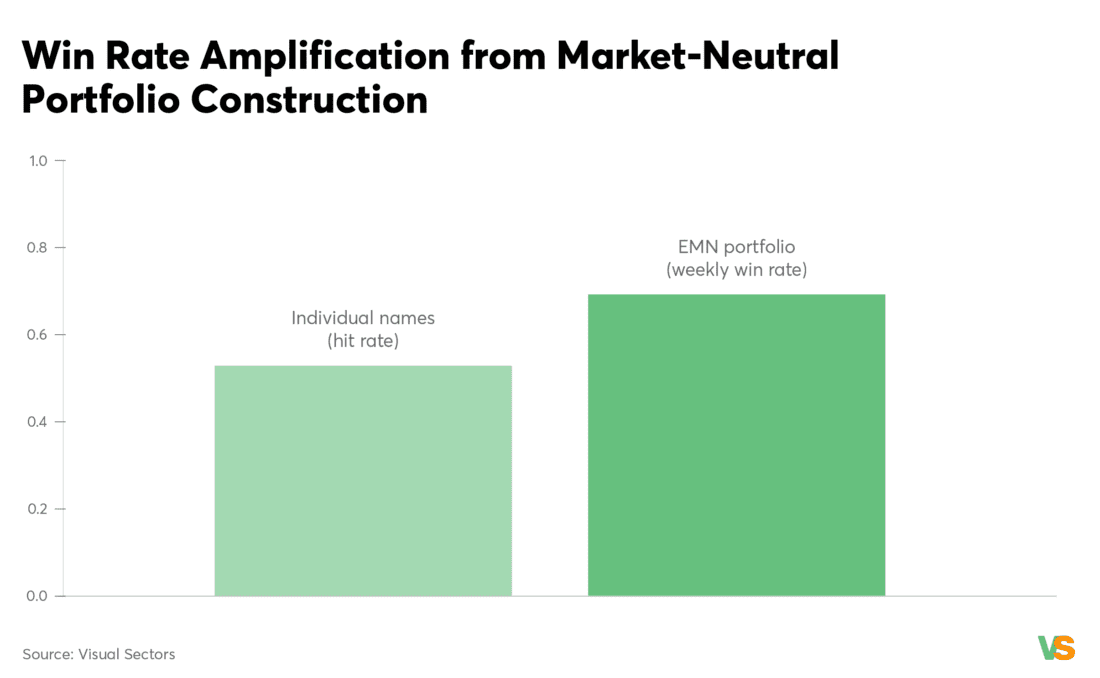

At the single-name level, signals often have modest directional accuracy (hit rate slightly above 50%). Portfolio construction can amplify this into a more stable return stream by reducing variance contributed by market direction and idiosyncratic noise.

The author reports a 52.91% hit rate at the individual-name level for the underlying selection process. In this sample, EMN’s weekly win rate is 69.2%. While the horizons are not identical, the direction is consistent with the hypothesis that market neutrality and diversification improve consistency.

Figure 11. Win rate amplification: individual-name hit rate (reported) vs EMN portfolio weekly win rate (observed).

Under a simple factor model, a stock’s return can be decomposed into market and idiosyncratic components. If the portfolio is constructed to target near-zero beta, then the market component is reduced, shrinking return variance without necessarily shrinking expected alpha. Because win probability for a given horizon increases with the mean-to-variance ratio, this can raise observed win rates at weekly and monthly frequencies.

The fundamental law of active management provides intuition for why breadth matters: risk-adjusted performance increases with both forecasting skill and breadth (the number of independent bets). A 7-long/7-short structure increases breadth relative to single-name trading and can mitigate concentration risk. This is not a free lunch—correlations can spike in crises—but it is a core mechanism behind market-neutral portfolio construction.

Modern toolchains (including large language models) reduce the cost of generating strategies from public price/volume features (moving averages, oscillators, breakouts, and other standard technical indicators). As a result, sustainable edge often shifts from implementation to information: unique datasets, superior labeling, and better microstructure understanding.

Empirical evidence suggests that widely disseminated predictors can attenuate as arbitrage capital learns and trades them. McLean and Pontiff document meaningful post-publication decay in return predictability, consistent with crowding in public signals. Related work on quant crowding emphasizes that when many investors hold similar trades, returns can compress and crash risk can rise.

“Portfolio returns are 26% lower out‑of‑sample and 58% lower post‑publication.”

— McLean & Pontiff (2016)

Options-flow and dealer-positioning measures are not simple functions of OHLC; they require specialized data and interpretation. Academic evidence supports their relevance: option volume and demand contain information about future stock price direction and volatility, and dealer gamma positioning can influence intraday momentum/reversal and volatility regimes. Taken together, this literature supports the claim that proprietary options-derived datasets can contain incremental information beyond OHLC.

In practice, building a durable edge around these signals requires:

These steps are difficult to commoditize and often determine whether a signal survives live deployment.

This note evaluates one return series over roughly one year. A thorough investment due diligence process would typically require:

A.1 Sharpe ratio (annualized, rf=0)

Sharpe = (mean(r_d) / std(r_d)) × √252, where r_d are daily returns.

A.2 Cumulative return and CAGR

Cumulative = ∏(1 + r_d) − 1. CAGR = (∏(1+r_d))^(252/N) − 1.

A.3 Max drawdown

Equity_t = ∏_{s≤t}(1+r_s). Drawdown_t = Equity_t / max_{u≤t}(Equity_u) − 1. MaxDD = min(Drawdown_t).

A.4 Historical VaR95 and CVaR95

VaR95 is the empirical 5th percentile of daily returns. CVaR95 is the mean of returns less than or equal to VaR95.

A.5 Information ratio

Active_t = r_EMN,t − r_SPX,t. IR = (mean(Active) / std(Active)) × √252.

A.6 Weekly/monthly returns and win rate

Weekly return: ∏(1+r_d)−1 within each week (Fri close). Win rate: fraction of weeks with return > 0. Monthly analog at month-end.

A.7 Autocorrelation and Ljung–Box

ACF(k) = corr(r_t, r_{t−k}). Ljung–Box tests joint significance of ACFs up to a chosen lag.

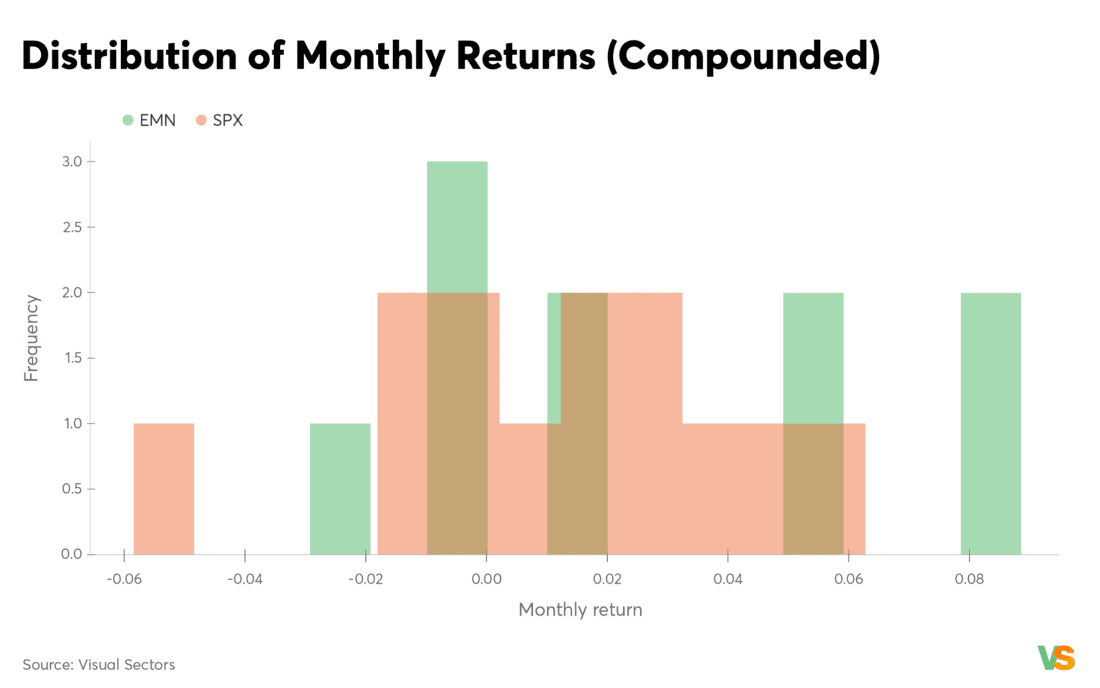

Return distributions are non-normal in this sample (Jarque–Bera rejects normality for both EMN and SPX), which motivates non-parametric tail metrics and stress testing beyond Gaussian assumptions.

Figure 13. Monthly return distributions (histograms).

All charts and statistics in this note are computed directly from the provided daily return series. Annualization uses a 252 trading-day convention. Weekly returns compound daily returns into Friday weeks; monthly returns compound to month-end. VaR and CVaR are computed historically from the empirical daily return distribution.

Moreira, A., & Muir, T. (2017). Volatility-Managed Portfolios. Journal of Finance.

Pan, J., & Poteshman, A. M. (2006). The Information in Option Volume for Future Stock Prices.

Ni, S. X., Pan, J., & Poteshman, A. M. (2008). Volatility Information Trading in the Option Market.

Gârleanu, N., Pedersen, L. H., & Poteshman, A. M. (2005/2009). Demand-Based Option Pricing.

Barbon, A., & Buraschi, A. (2021). Gamma Fragility.

Cahan, R., & Luo, Y. (2013). Measuring Crowding in Quantitative Strategies.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Visual Sectors and is being posted with its permission. The views expressed in this material are solely those of the author and/or Visual Sectors and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Options involve risk and are not suitable for all investors. For information on the uses and risks of options, you can obtain a copy of the Options Clearing Corporation risk disclosure document titled Characteristics and Risks of Standardized Options by going to the following link ibkr.com/occ. Multiple leg strategies, including spreads, will incur multiple transaction costs.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!