- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted July 28, 2021 at 1:18 pm

This post explains how to calculate delta sensitivities or delta vector of interest rate swap. Delta can be calculated by either 1) zero delta or 2) market delta. To the best of our knowledge, FRTB can use these two methods but SIMM use the market Greeks. We implement R code for two approaches.

For detailed information about the Libor IRS swap pricing and zero curve bootstrapping, refer to the following posts.

In previous posts, we have priced a 5Y Libor IRS swap and generated a zero curve from market swap rates by using bootstrapping. Based on these works, we calculate Greeks of IRS. Since IRS does not have any option characteristics, our focus is to calculate the delta sensitivities or delta vector. And for convenience, swap value is defined as (floating leg – fixed leg).

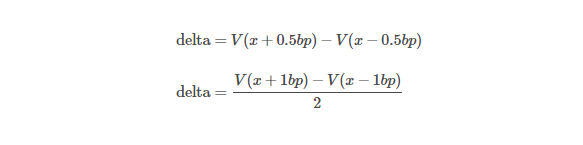

ISDA SIMM uses the following definitions of interest rate risk delta (xx is a risk factor). There are, of course, several versions of it but they are all essentially the same.

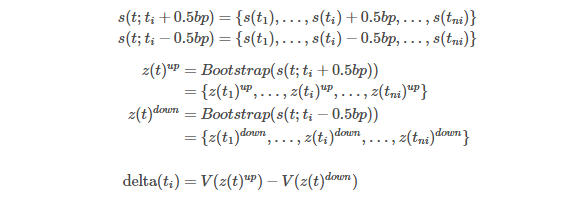

For ease of notation, let z(t) and s(t) denote the (bootstrapped) zero rates or zero curve and (market observed) swap rates or swap curve at time t respectively.

There are two approaches for the calculation of delta: 1) zero delta, 2) market delta.

Zero delta approach calculates delta sensitivities by bumping up or down zero rates one by one in order.

Once the zero curve (z(t)) is generated from market swap rates (s(t)),

Bumping up (z(t; ti + 0.5bp) or down (z(t; ti−0.5bp)), delta(ti) is calculated and this process is applied for all ti.

Here, ti, i = 1, 2,…, ni = 1, 2,…, n i are maturities or dates of market swap rates at which the corresponding zero rates are bootstrapped.

Market delta approach calculates delta sensitivities by bumping up or down market swap rates one by one in order. Unlike the zero delta, every time we bump one market swap rate of a selected maturity, we should run a bootstrapping for finding new zero curve. Using this newly generated zero curve, we can calculate delta sensitivity at time ti as follows.

The following R code calculates delta sensitivities of IRS using these two approaches.

#=========================================================================#

# Financial Econometrics & Derivatives, ML/DL using R, Python, Tensorflow

# by Sang-Heon Lee

#

# https://kiandlee.blogspot.com

#————————————————————————-#

# Calculate Delta Sensitivities of Libor IRS

#=========================================================================#

graphics.off() # clear all graphs

rm(list = ls()) # remove all files from your workspace

#=========================================================================

# Functions – Definition

#=========================================================================

#————————————————————–

# Calculation of IRS swap price

#————————————————————–

f_zero_prr_IRS <– function(

fixed_rate, # fixed rate

vd.fixed_date, vd.float_date, # date for two legs

vd.zero_date, v.zero_rate, # zero curve (dates, rates)

d.spot_date, no_amt, # spot date, nominal amt

save_cf_yn) { # “y” : CF save

#———————————————————-

# 0) Preprocessing

#———————————————————-

# convert spot date from date(d) to numeric(n)

n.spot_date <– as.numeric(d.spot_date)

# Interpolation of zero curve

vn.zero_date <– as.numeric(vd.zero_date)

f_linear <– approxfun(vn.zero_date, v.zero_rate,

method=“linear”)

vn.zero_date.inter <– n.spot_date:max(vn.zero_date)

v.zero_rate.inter <– f_linear(vn.zero_date)

# number of CFs

ni <– length(vd.fixed_date)

nj <– length(vd.float_date)

# output data.frame with CF dates and its interpolated zero

df.fixed = data.frame(d.date = vd.fixed_date,

n.date = as.numeric(vd.fixed_date))

df.float = data.frame(d.date = vd.float_date,

n.date = as.numeric(vd.float_date))

#———————————————————-

# 1) Fixed Leg

#———————————————————-

# zero rate for discounting

df.fixed$zero_DC = f_linear(as.numeric(df.fixed$d.date))

# discount factor

df.fixed$DF <– exp(–df.fixed$zero_DC*

(df.fixed$n.date–n.spot_date)/365)

# tau, CF

for(i in 1:ni) {

ymd <– df.fixed$d.date[i]

ymd_prev <– df.fixed$d.date[i–1]

if(i==1) ymd_prev <– d.spot_date

d <– as.numeric(strftime(ymd, format = “%d”))

m <– as.numeric(strftime(ymd, format = “%m”))

y <– as.numeric(strftime(ymd, format = “%Y”))

d_prev <– as.numeric(strftime(ymd_prev, format = “%d”))

m_prev <– as.numeric(strftime(ymd_prev, format = “%m”))

y_prev <– as.numeric(strftime(ymd_prev, format = “%Y”))

# 30I/360

tau <– (360*(y–y_prev) + 30*(m–m_prev) + (d–d_prev))/360

# cash flow rate

df.fixed$rate[i] <– fixed_rate

# Cash flow at time ti

df.fixed$CF[i] <– fixed_rate*tau*no_amt # day fraction

}

# Present value of CF

df.fixed$PV = df.fixed$CF*df.fixed$DF

#———————————————————-

# 2) Floating Leg

#———————————————————-

# zero rate for discounting

df.float$zero_DC = f_linear(as.numeric(df.float$d.date))

# discount factor

df.float$DF <– exp(–df.float$zero_DC*

(df.float$n.date–n.spot_date)/365)

# tau, forward rate, CF

for(i in 1:nj) {

date <– df.float$n.date[i]

date_prev <– df.float$n.date[i–1]

DF <– df.float$DF[i]

DF_prev <– df.float$DF[i–1]

if(i==1) {

date_prev <– n.spot_date

DF_prev <– 1

}

# ACT/360

tau <– (date – date_prev)/360

# forward rate

fwd_rate <– (1/tau)*(DF_prev/DF–1)

# cash flow rate

df.float$rate[i] <– fwd_rate

# Cash flow amount at time ti

df.float$CF[i] <– fwd_rate*tau*no_amt # day fraction

}

# Present value of CF

df.float$PV = df.float$CF*df.float$DF

# check for cash flows

if (save_cf_yn == “y”) {

# print(df.float); print(df.fixed)

write.csv(df.float, “CF_float.csv”)

write.csv(df.fixed, “CF_fixed.csv”)

}

return(sum(df.float$PV) – sum(df.fixed$PV))

}

#————————————————————–

# IRS swap zero curve generator

#————————————————————–

f_zero_maker_IRS <– function(

df.mt, # market information data.frame

# [d.date, swap_rate, source]]

v.unknown_swap_maty_all, # all unknown swap maturity

vd.fixed_date, # date for fixed leg

vd.float_date, # date for float leg

d.spot_date, # spot date

no_amt) { # nominal principal amount

# convert spot date from date(d) to numeric(n)

n.spot_date <– as.numeric(d.spot_date)

# for bootstrapped zero curve

df.zr <– data.frame(

d.date = df.mt$d.date,

n.date = as.numeric(df.mt$d.date),

tau = as.numeric(df.mt$d.date) – n.spot_date,

taui = as.numeric(df.mt$d.date) – n.spot_date,

swap_rate = df.mt$swap_rate,

zero_rate = rep(0,length(df.mt$d.date)),

DF = rep(0,length(df.mt$d.date)))

# tau(i) = t(i) – t(i-1)

df.zr$taui[2:nrow(df.zr)] <–

df.zr$n.date[2:nrow(df.zr)] –

df.# semi-annual date[1: (nrow(df.zr)–1)]

# divide rows according to its source or instrument type

rows_deposit <– which(df.mt$source==“deposit”)

rows_futures <– which(df.mt$source==“futures”)

rows_swap <– which(df.mt$source==“swap”)

#————————————————————–

# 3. Bootstrapping – Deposit

#————————————————————–

for(i in rows_deposit) {

# 1) calculate discount factor for deposit

df.zr$DF[i] <– 1/(1+df.zr$swap_rate[i]*df.zr$tau[i]/360)

# 2) convert DF to spot rate

df.zr$zero_rate[i] <– 365/df.zr$tau[i]*log(1/df.zr$DF[i])

}

#————————————————————–

# 4. Bootstrapping – Futures

#————————————————————–

# No convexity adjustment is made

for(i in rows_futures) {

# 1) discount factor from t(i-1) to t(i)

df.zr$DF[i] <– 1/(1+df.zr$swap_rate[i]*df.zr$taui[i]/360)

# 2) discount factor from spot date to t(i)

df.zr$DF[i] <– df.zr$DF[i–1]*df.zr$DF[i]

# 3) zero rate from discount factor

df.zr$zero_rate[i] <– 365/df.zr$tau[i]*log(1/df.zr$DF[i])

}

#————————————————————–

# 5. Bootstrapping – Swaps

#————————————————————–

k <– 1

for(i in rows_swap) {

# unknown swap maturity in year

swap_maty <– v.unknown_swap_maty_all[k]

# 1) find one unknown zero rate for one swap maturity

m<–optim(0.01, objf,

control = list(abstol=10^(–20), reltol=10^(–20),

maxit=50000, trace=2),

method = c(“Brent”),

lower = 0, upper = 0.1, # for Brent

v.unknown_swap_maty = swap_maty, # unknown zero maturity

v.swap_rate = df.zr$swap_rate[i], # observed swap rate

vd.fixed_date = vd.fixed_date, # date for fixed leg

vd.float_date = vd.float_date, # date for float leg

vd.zero_date_all = df.zr$d.date[1:i], # all dates for zero curve

v.zero_rate_known = df.zr$zero_rate[1: (i–1)], # known zero rates

d.spot_date = d.spot_date,

no_amt = no_amt)

# 2) update this zero curve with the newly found zero rate

df.zr$zero_rate[i] <– m$par

# 3) convert this new zero rate to discount factor

df.zr$DF[i] <– exp(–df.zr$zero_rate[i]*df.zr$tau[i]/365)

k <– k + 1

}

return(df.zr)

}

#————————————————————–

# objective function to be minimized

#————————————————————–

objf <– function(

v.unknown_swap_zero_rate, # unknown zero curve (rates)

v.unknown_swap_maty, # unknown swap maturity

v.swap_rate, # fixed rate

vd.fixed_date, # date for fixed leg

vd.float_date, # date for float leg

vd.zero_date_all, # all dates for zero curve

v.zero_rate_known, # known zero curve (rates)

d.spot_date, # spot date

no_amt) { # nominal principal amount

# zero curve augmented with zero rates for swaps

v.zero_rate_all <– c(v.zero_rate_known,

v.unknown_swap_zero_rate)

v.swap_pr <– NULL # vector of swap prices

k <– 1

for(i in v.unknown_swap_maty) {

# calculate IRS swap price

swap_pr <– f_zero_prr_IRS(

v.swap_rate[k], # fixed rate,

vd.fixed_date[1: (2*i)], # semi-annual date

vd.float_date[1: (4*i)], # quarterly date

vd.zero_date_all, # zero curve (dates)

v.zero_rate_all, # zero curve (rates)

d.spot_date, no_amt, “n”)

# concatenate swap prices

v.swap_pr <– c(v.swap_pr, swap_pr)

k <– k + 1

}

return(sum(v.swap_pr^2))

}

#=========================================================================

# Main

#=========================================================================

#————————————————————–

# 1. Market Information

#————————————————————–

# Zero curve from Bloomberg as of 2021-06-30 until 5-year maturity

df.mt <– data.frame(

d.date = as.Date(c(“2021-10-04”,“2021-12-15”,

“2022-03-16”,“2022-06-15”,

“2022-09-21”,“2022-12-21”,

“2023-03-15”,“2023-07-03”,

“2024-07-02”,“2025-07-02”,

“2026-07-02”)),

# we use swap rate not zero rate.

swap_rate= c(0.00145750000000000,

0.00139609870272047,

0.00203838571440434,

0.00197747863867587,

0.00266249271921742,

0.00359490949297661,

0.00512603194652204,

0.00328354999423027,

0.00571049988269806,

0.00793000012636185,

0.00964949995279312

),

source = c(“deposit”, rep(“futures”,6), rep(“swap”, 4))

)

#————————————————————–

# 2. Libor Swap Specification

#————————————————————–

d.spot_date <– as.Date(“2021-07-02”) # spot date (date type)

n.spot_date <– as.numeric(d.spot_date) # spot date (numeric type)

no_amt <– 10000000 # notional principal amount

# swap cash flow schedule from Bloomberg

lt.cf_date <– list(

fixed = as.Date(c(“2022-01-04”,“2022-07-05”,

“2023-01-03”,“2023-07-03”,

“2024-01-02”,“2024-07-02”,

“2025-01-02”,“2025-07-02”,

“2026-01-02”,“2026-07-02”)),

float = as.Date(c(“2021-10-04”,“2022-01-04”,

“2022-04-04”,“2022-07-05”,

“2022-10-03”,“2023-01-03”,

“2023-04-03”,“2023-07-03”,

“2023-10-02”,“2024-01-02”,

“2024-04-02”,“2024-07-02”,

“2024-10-02”,“2025-01-02”,

“2025-04-02”,“2025-07-02”,

“2025-10-02”,“2026-01-02”,

“2026-04-02”,“2026-07-02”))

)

#————————————————————–

# 3. 5-year swap price : base

#————————————————————–

i = 5 # 5-year swap

# zero pricing

df.zr <– f_zero_maker_IRS(

df.mt, c(2,3,4,5),

lt.cf_date$fixed, lt.cf_date$float,

d.spot_date, no_amt)

pr <– f_zero_prr_IRS(

df.mt$swap_rate[i+6],

lt.cf_date$fixed[1: (2*i)],

lt.cf_date$float[1: (4*i)],

df.zr$d.date, df.zr$zero_rate,

d.spot_date,no_amt, save_cf_yn = “y”)

print(paste0(i,“-year Swap price at spot date = “, pr))

df.zr_delta <– df.mt_delta <– df.zr[,–c(2,3,4)]

df.zr_delta$pr <– df.mt_delta$pr <– pr

#————————————————————–

# 3. Bump and Reprice for Market Greeks

#————————————————————–

df.mt_delta$delta <– df.mt_delta$pr_up <– df.mt_delta$pr_dn <– NA

# iteration for all market maturities

for(r in 1:11) {

#———————

# bump up (1bp up)

#———————

df.mt_bump <– df.mt # initialization

df.mt_bump$swap_rate[r] <– df.mt_bump$swap_rate[r] + 0.0001

# zero pricing

df.zr <– f_zero_maker_IRS(df.mt_bump, c(2,3,4,5),

lt.cf_date$fixed, lt.cf_date$float,

d.spot_date, no_amt)

pr <– f_zero_prr_IRS(df.mt$swap_rate[i+6],

lt.cf_date$fixed[1: (2*i)],

lt.cf_date$float[1: (4*i)],

df.zr$d.date, df.zr$zero_rate,

d.spot_date, no_amt, “n”)

# save price with bumping up

df.mt_delta$pr_up[r] <– pr

# check whether swap prices at spot date is at par

pr <– f_zero_prr_IRS(df.mt_bump$swap_rate[i+6],

lt.cf_date$fixed[1: (2*i)],

lt.cf_date$float[1: (4*i)],

df.zr$d.date, df.zr$zero_rate,

d.spot_date,no_amt, “n”)

print(paste0(i,“-year Swap price at spot date = “, pr))

#———————

# bump down (1bp down)

#———————

df.mt_bump <– df.mt # initialization

df.mt_bump$swap_rate[r] <– df.mt_bump$swap_rate[r] – 0.0001

# zero pricing

df.zr <– f_zero_maker_IRS(df.mt_bump, c(2,3,4,5),

lt.cf_date$fixed, lt.cf_date$float,

d.spot_date, no_amt)

pr <– f_zero_prr_IRS(df.mt$swap_rate[i+6],

lt.cf_date$fixed[1: (2*i)], lt.cf_date$float[1: (4*i)],

df.zr$d.date, df.zr$zero_rate, d.spot_date,no_amt, “n”)

# save price with bumping down

df.mt_delta$pr_dn[r] <– pr

# check whether swap prict at spot date is at par

pr <– f_zero_prr_IRS(df.mt_bump$swap_rate[i+6],

lt.cf_date$fixed[1: (2*i)], lt.cf_date$float[1: (4*i)],

df.zr$d.date, df.zr$zero_rate, d.spot_date,no_amt, “n”)

print(paste0(i,“-year Swap price at spot date = “, pr))

}

# Market Greeks : Delta calculation

df.mt_delta$delta <– (df.mt_delta$pr_up –

df.mt_delta$pr_dn)/2

df.mt_delta

x11(width = 5, height = 3.5)

barplot(delta ~ substr(d.date,1,7), data = df.mt_delta,

width = 0.5, col = “blue”)

x11(width = 5, height = 3.5)

barplot(delta ~ substr(d.date,1,7), data = df.mt_delta[1:10,],

width = 0.5, col = “green”)

#————————————————————–

# 4. Bump and Reprice for Zero Greeks

#————————————————————–

df.zr_delta$delta <– df.zr_delta$pr_up <– df.zr_delta$pr_dn <– NA

# zero pricing

df.zr <– f_zero_maker_IRS(df.mt, c(2,3,4,5),

lt.cf_date$fixed, lt.cf_date$float, d.spot_date, no_amt)

for(r in 1:11) {

#———————

# bump up (1bp up)

#———————

df.zr_bump <– df.zr # initialization

df.zr_bump$zero_rate[r] <– df.zr_bump$zero_rate[r] + 0.0001

# zero pricing

pr <– f_zero_prr_IRS(df.mt$swap_rate[i+6],

lt.cf_date$fixed[1: (2*i)], lt.cf_date$float[1: (4*i)],

df.zr_bump$d.date, df.zr_bump$zero_rate,

d.spot_date, no_amt, “n”)

# save price with bumping up

df.zr_delta$pr_up[r] <– pr

#———————

# bump down (1bp down)

#———————

df.zr_bump <– df.zr # initialization

df.zr_bump$zero_rate[r] <– df.zr_bump$zero_rate[r] – 0.0001

# zero pricing

pr <– f_zero_prr_IRS(df.mt$swap_rate[i+6],

lt.cf_date$fixed[1: (2*i)], lt.cf_date$float[1: (4*i)],

df.zr_bump$d.date, df.zr_bump$zero_rate,

d.spot_date,no_amt, “n”)

# save price with bumping down

df.zr_delta$pr_dn[r] <– pr

}

# Market Greeks : Delta calculation

df.zr_delta$delta <– (df.zr_delta$pr_up –

df.zr_delta$pr_dn)/2

df.zr_delta

x11(width = 5, height = 3.5)

barplot(delta ~ substr(d.date,1,7), data = df.zr_delta,

width = 0.5, col = “blue”)

x11(width = 5, height = 3.5)

barplot(delta ~ substr(d.date,1,7), data = df.zr_delta[1:10,],

width = 0.5, col = “green”)

Colored by Color ScripterStay tuned for the next installment to learn about the output demonstrating zero delta vector along the maturities.

For additional insight on this topic and to download the R scripts, visit https://kiandlee.blogspot.com/2021/07/delta-sensitivity-of-interest-rate-swap.html.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from SHLee AI Financial Model and is being posted with its permission. The views expressed in this material are solely those of the author and/or SHLee AI Financial Model and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!