- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted June 18, 2024 at 11:39 am

The article “Complexity Is a Virtue in Return Prediction” first appeared on Alpha Architect blog.

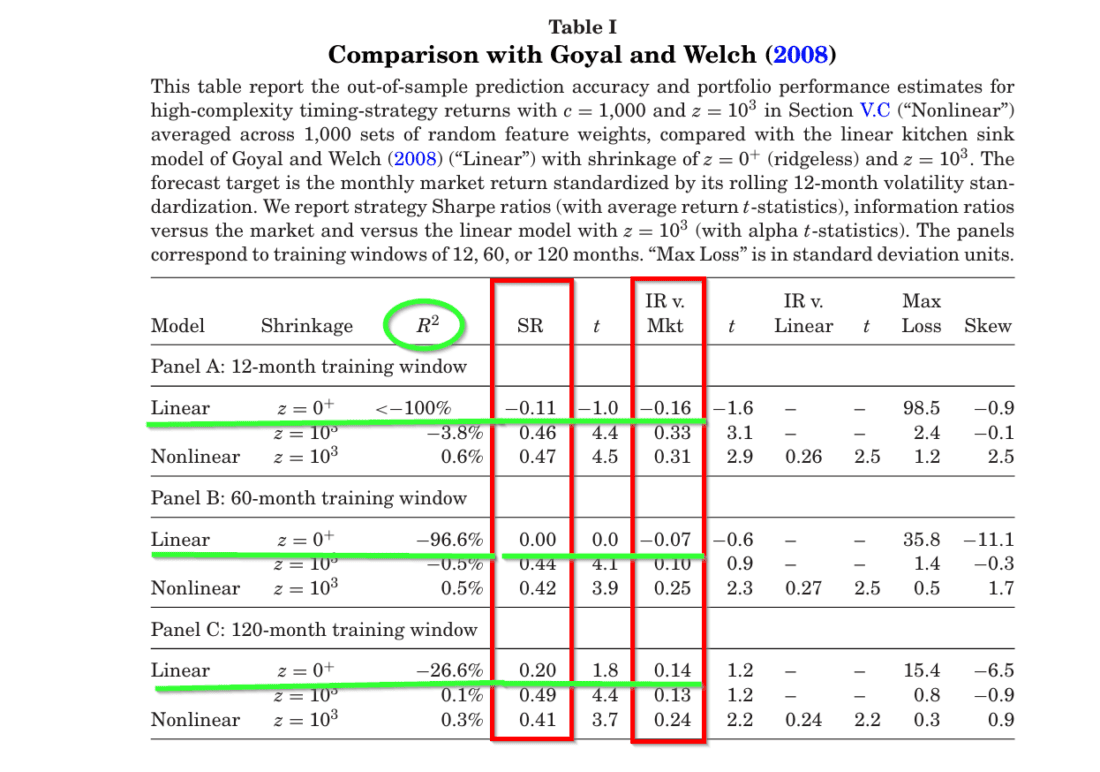

Finance has seen unprecedented growth in the use of artificial intelligence, specifically in machine learning models. Applications have included portfolio construction, stock analysis and in this case, the prediction of stock market returns. This paper discusses the benefits of using complex models as found in AI, over simple models such as ordinary least squares for predicting market returns. The authors highlight the limitations of traditional simple models and advocate for the adoption of complex, machine learning-based approaches. Traditionally, market return predictions have relied on simple models with only a few parameters which significantly understate the predictability of stock returns. Complex models, which use more parameters than the number of observations, offer much better levels of predictability for market returns. Good news for the application of AI in quantitative finance.

This is an excellent article. I believe it will provide much impetus in moving finance and investments in the direction of complexity and away from the very restrictive, simple models we are using currently. A word of warning: the article is heavy on the mathematical and theoretical foundations of ML models. The reward for working through the details is an understanding of the statistical linkages between the large or complex and small or simple models. This summary will only provide a review of the high points, at least for now.

The research presented here establishes the “virtue of complexity” found in ML models and finds that it aligns itself very closely with real-world market behavior without the bias imposed by the simple models or the misuse of statistics. The authors do caution against adding variables to a model on an arbitrary basis but encourage adding them if they are likely to be relevant. They also encourage the use of highly parameterized nonlinear prediction models. A few takeaways: (1) Simple models are preferable only if they are specified correctly and that’s a tall order, (2) Complex models are preferable under general conditions, and (3) There is a need to move beyond simple models and consider the benefits of complexity, especially in the context of machine learning, to improve return predictions and portfolio performance .

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Much of the extant literature predicts market returns with “simple” models that use only a few parameters. Contrary to conventional wisdom, we theoretically prove that simple models severely understate return predictability compared to “complex” models in which the number of parameters exceeds the number of observations. We empirically document the virtue of complexity in U.S. equity market return prediction. Our findings establish the rationale for modeling expected returns through machine learning.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

This site provides NO information on our value ETFs or our momentum ETFs. Please refer to this site.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Alpha Architect and is being posted with its permission. The views expressed in this material are solely those of the author and/or Alpha Architect and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!