- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted October 1, 2024 at 11:54 am

The article “Can Skewness Identify Future Outperforming Mutual Funds” first appeared on Alpha Architect blog.

The annual SPIVA has documented that retail mutual funds underperform with great persistence, with any persistence of outperformance not significantly greater than would be randomly expected. The large body of research on the failure of active management led Charles Ellis to famously call it a “loser’s game”—one that is possible to win, though the odds of doing so are so poor the surest way to win is to not play. By that, he meant to avoid investing in funds that engage in individual security selection and/or market timing (active management).

Despite the large body of evidence against the use of active strategies, given the potential reward, there have been many attempts to find a methodology that would identify future outperformers ahead of time. Much of the effort has focused on active share as predictor. Unfortunately, the evidence, as presented in this article about the predictive power of active share, does not support the hypothesis that active share explains future outperformance. But hope springs eternal.

New Research

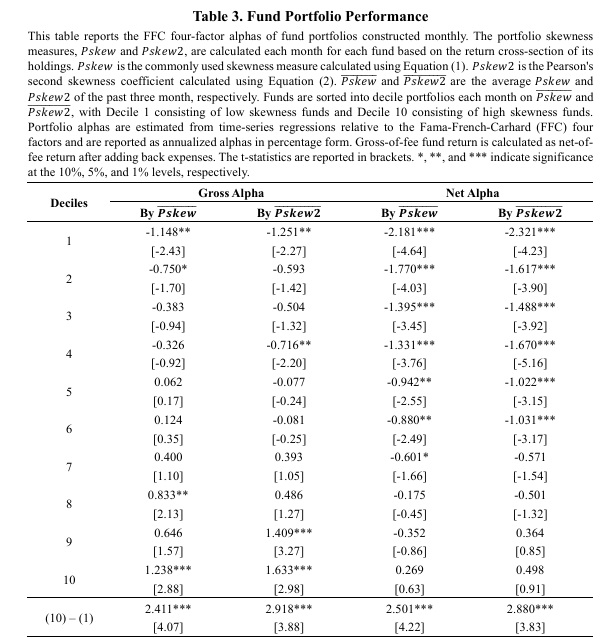

Jo Drienko, Chao Gao, and Yifei Liu, authors of the August 2024 study “A Skew is a Skill: Portfolio Skewness of Mutual Fund Holdings,” hypothesized: “Skilled managers are more likely to include winners and exclude losers in their portfolios, thus resulting in higher skewness in the cross-sectional return distribution of their holdings.” To investigate this hypothesis, they constructed portfolio skewness measures (the average monthly portfolio skewness of the past three months) from the cross-section of the holdings in each fund’s portfolio. Their data sample covered U.S. equity mutual funds over the period 1980-2023. Following is a summary of their key findings:

Unfortunately, as the table below demonstrates, the net of fee returns (what investors earn) of the highest skewness funds did not generate statistically significant alphas.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

It’s also worth noting that the authors found that active share did not show significant alpha predictability.

Their findings led Drienko, Gao, and Liu to conclude:

“We find that funds with high portfolio skewness significantly outperform funds with low portfolio skewness in the future. From a time-series perspective, the outperformance is larger when the investment opportunity is higher, meaning that skilled managers have better responses to investment opportunity innovations.” They added: “We infer that managers of high skewness funds achieve better performance through stock selection rather than active trading…. Portfolio skewness has implications for mutual fund investors as it only relies on limited historical holdings data to construct. It is particularly helpful in identifying funds consistently selecting inferior stocks as these funds significantly underperform, regardless of fund fees.”

Before drawing any conclusions, it is important to note that the authors use portfolio holdings, and the filings of holdings are delayed by 45 days. Thus, investors would not get data for the nearest future month until it had been over for at least 15 days. As an example, consider a fund with Q4 calendar end in December. You need the December holdings to determine whether the fund will do well in January. However, those holdings won’t be available until about Feb 15. Thus, their findings are not very useful for an investor. This issue could be addressed by addressed by lagging the data. Whether the results still hold remains to be seen, although the authors note that their measure of skewness doesn’t change too much from quarter to quarter.

Investor takeaways

Drienko, Gao, and Liu showed that the skewness of fund returns can help investors by identifying funds that are likely to persistently underperform. Unfortunately, being able to avoid persistent losers is not sufficient for successful management as skewness did not allow them to confidently select funds that could outperform. While the skewness metric did demonstrate that it could select funds with managers skilled a security selection, the fund’s expenses and implementation meant that the fund was just about able to cover its expenses, and that was before the negative impact of active management on after-tax returns—and the finding was not statistically significant at even the 10% level of confidence.

Larry Swedroe is the author or co-author of 18 books on investing, including his latest Enrich Your Future.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

This site provides NO information on our value ETFs or our momentum ETFs. Please refer to this site.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Alpha Architect and is being posted with its permission. The views expressed in this material are solely those of the author and/or Alpha Architect and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Mutual Funds are investments that pool the funds of investors to purchase a range of securities to meet specified objectives, such as growth, income or both. Investors are reminded to consider the various objectives, fees, and other risks associated with investing in Mutual Funds. Please read the prospectus accordingly. This communication is not to be construed as a recommendation, solicitation or promotion of any specific fund, or family of funds. Interactive Brokers may receive compensation from fund companies in connection with purchases and holdings of mutual fund shares. Such compensation is paid out of the funds' assets. However, IBKR does not solicit you to invest in specific funds and does not recommend specific funds or any other products to you. For additional information please visit https://www.interactivebrokers.com/en/index.php?f=1563&p=mf

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!