- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted January 2, 2024 at 10:16 am

The article “Can Machine Learning Help to Select Mutual Funds with Positive Alpha?” first appeared on Alpha Architect blog.

The study emphasizes the importance of integrating machine learning with other tools for investment managers, pension-plan administrators, financial advisors, and independent analysts to help investors select active mutual funds with positive alpha. It also highlights the significance of fund characteristics in predicting alpha, even when portfolio holdings are not disclosed.

Machine learning and fund characteristics help to select mutual funds with positive alpha

The authors ask the following questions:

This paper matters because it challenges prevailing notions about the performance of active mutual funds, showcases the potential for machine learning to enhance investment outcomes, and offers insights that can inform investment strategies, regulatory decisions, and discussions about market efficiency in the mutual-fund industry.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

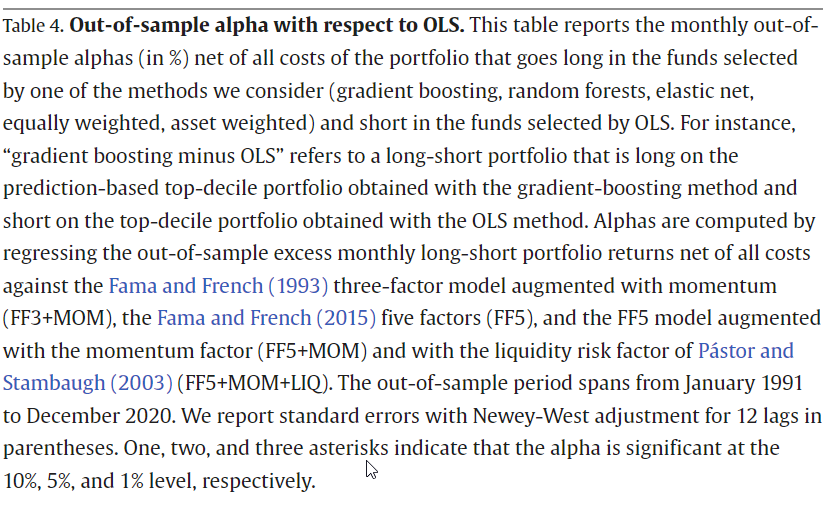

Machine-learning methods exploit fund characteristics to select tradable long-only portfolios of mutual funds that earn significant out-of-sample annual alphas of 2.4% net of all costs. The methods unveil interactions in the relation between fund characteristics and future performance. For instance, past performance is a particularly strong predictor of future performance for more active funds. Machine learning identifies managers whose skill is not sufficiently offset by diseconomies of scale, consistent with informational frictions preventing investors from identifying the outperforming funds. Our findings demonstrate that investors can benefit from active management, but only if they have access to sophisticated prediction methods.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

This site provides NO information on our value ETFs or our momentum ETFs. Please refer to this site.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Alpha Architect and is being posted with its permission. The views expressed in this material are solely those of the author and/or Alpha Architect and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Mutual Funds are investments that pool the funds of investors to purchase a range of securities to meet specified objectives, such as growth, income or both. Investors are reminded to consider the various objectives, fees, and other risks associated with investing in Mutual Funds. Please read the prospectus accordingly. This communication is not to be construed as a recommendation, solicitation or promotion of any specific fund, or family of funds. Interactive Brokers may receive compensation from fund companies in connection with purchases and holdings of mutual fund shares. Such compensation is paid out of the funds' assets. However, IBKR does not solicit you to invest in specific funds and does not recommend specific funds or any other products to you. For additional information please visit https://www.interactivebrokers.com/en/index.php?f=1563&p=mf

Do you know of any free and sophisticated prediction programs?