- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted July 1, 2026 at 1:19 pm

Stocks are rebounding from early turbulence and are heading for a third consecutive session of gains after a one-two punch featuring Fed Chair Warsh acknowledging progress on inflation and separately, economic figures that are providing additional evidence of an ongoing cyclical reacceleration. The head of US monetary policy, who spoke at the Sintra, Portugal, ECB hosted forum, also opined that cost pressures are still elevated, which countered what could have been a dovish market response, keeping the yield curve unchanged as fixed-income observers interpreted his presentation as neutral. The greenback is strengthening on an independence bid though, as the institution is seen as increasingly prioritizing the price side of its mandate in consideration of robust labor conditions and buoyant activity. This morning’s data provided proof of just that, as ADP reported strong hiring, Challenger, Gray and Christmas depicted declining layoffs and ISM announced a sustained manufacturing expansion. Although a pair of the results were slightly below estimates, equities are reacting positively with the Russell 2000 Index and the Dow Jones Industrial Average hitting fresh records amidst broad sector participation. Conversely, tech is returning a good chunk of yesterday’s advance as semiconductor weakness offsets steep climbs amongst the Magnificent 7 names minus Nvidia. Elsewhere, cryptocurrencies and precious metals are rallying while prediction markets catch bids, but energy and copper commodities are retreating while volatility protection instruments are facing neglect as weakening hedging demand coincides with risk-on winds dominating Wall Street.

Private employers added jobs broadly last month although the pace of hiring moderated from May’s 15-month high. The June 98k headline slightly missed the median estimate of 113k and arrived beneath the prior period’s 122k. Mining was the only sector that reduced payrolls; the segment saw headcounts shrink 5k. The other nine categories experienced growth, with education/health services, trade/transportation/utilities, and financial activities leading with additions of 48k, 15k and 14k. Other services, information, manufacturing, leisure/hospitality, construction and professional/business services contributed at more tempered degrees with expansions of 8k and under. Additionally, small, mid-size and large businesses, defined as having 1-49, 50-499 and 500+ employees, expanded their rosters by 53k, 29k and 25k. Wages accelerated overall, meanwhile, as the year-over-year (y/y) change in annual pay came in at 6.6% and 4.4% across job changers and stayers, compared to 6.5% and 4.4% from the previous interval.

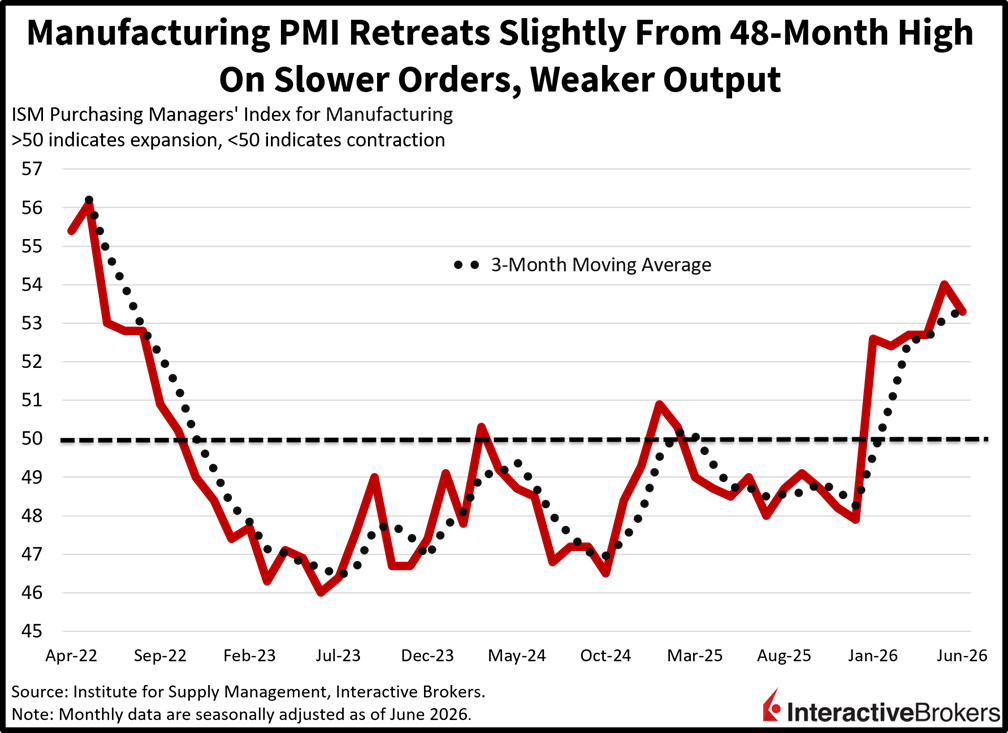

The US manufacturing sector decelerated in June from a 48-month high on slower demand and weaker output. But the Institute of Supply Management’s (ISM) Purchasing Managers’ Index (PMI), at 53.3, was still robust and considerably above the expansion-contraction threshold of 50. The print, however, was slightly lower than the median estimate for an unchanged 54 from May. New orders, production, backlogs and exports fell to scores of 56, 52.2, 50.5 and 48.5 from 56.8, 54.3, 52.2 and 50.6. Prices grew but at a more tempered pace of 73 on the back of a significant plunge in fuel costs, which was partially countered by increases in tariff-related expenses. Employment continued to decline, but the category’s lift from 48.6 to 49.7 toward the neutral level signals the potential for payroll growth in the near future.

June layoff announcements softened to 45.8k, a 53% month-over-month (m/m) drop and the lowest total of the year. The cuts are still predominantly from AI-related developments, according to Challener, Gray & Christmas. Hiring plans, however, fell to 10.9k from the 19.53k last month; they were well above the 3.2k from the year-ago period.

A modest miss in tomorrow’s government jobs report, similar to today’s ADP print, would likely drive an independence rally prior to the three-day July 4 weekend. Numbers that are strong, but not too hot, would point to an ongoing expansion in the labor market without raising yields, factors that would be conducive for another session of fresh records for the Dow Jones Industrial Average and the Russell 2000 Index. A figure approaching 100k of 95k, below the 110k expected, is what I’m projecting, and that result is poised to offer a terrific end of week for investors. And the good news is that participants won’t have to digest any pivotal economic figures until the week of July 13, when inflation data will signal that the peak in annualized price pressures is behind us and that costs are decelerating from here on the back of subdued fuel charges, constrained housing valuations and slow rent growth.

The S&P RatingDog China General Manufacturing PMI for June depicts conditions improving for the seventh-consecutive month in the world’s second-largest economy with businesses reporting strong orders, increased hiring and easing input inflation. This headline weakened slightly from May’s 51.8 to 51.7, a three-month low that missed the economist consensus estimate of 51.9, but it remained significantly above the contraction-expansion threshold of 50. Earlier yesterday, the official National Bureau of Statistics PMI showed manufacturing climbing from 50 in May to 50.3 for last month, a result, in large part, of vibrant export demand for alternative energy equipment and artificial intelligence products. The RatingDog gauge is more heavily weighted toward large companies and exports. As such, it is less impacted by the country’s sluggish domestic conditions, resulting in it trending higher than the government PMI in recent months.

Some of the positive RatingDog observations were as follows:

Conversely, input inflation continued but slowed from April’s four-year high and manufacturers were able to increase their gate prices. Businesses also reported the second consecutive month of declines in export orders, but the drop was only marginal. When looking at the coming 12 months, manufacturers said they are optimistic due to having created new products while finding new opportunities and forging improvements in production. Nevertheless, the degree of optimism was the softest year-to-date.

South Korea’s trade surplus jumped from $27 billion in May to $36.1 billion last month with strong global demand for AI semiconductors pushing up the country’s exports, according to a preliminary estimate from Statistics Korea. Exports were 70.9% higher than in the year-ago period, a considerable advance from May’s 53.4% y/y growth. Meanwhile, the country’s purchases of items from foreign markets climbed 30.1% y/y following the preceding period’s 20.7% increase. The strong surge in shipments to other countries resulted in exports hitting $102.2 billion, an all-time high. The value of semiconductor shipments almost tripled as companies building AI facilities snatched up memory chips. Higher energy prices, furthermore, resulted in the value of petroleum product exports growing 49.8%. Automobile shipments also climbed but at a much more modest 5% pace. During June, the US increased its purchases of South Korean products by 78.6%. In other markets, South Korea increased its sales to Southeast Asian nations and the European Union by 86.6% and 31.8%, respectively.

Prices in the euro area were up 2.8% y/y in June, a significant deceleration from the 3.2% jump in May, according to a preliminary release of the All-Items Harmonized Consumer Price Index from Eurostat. The headline, furthermore, was lower than the economist consensus estimate of 3%. On a m/m basis, prices descended by 0.1%, a reversal from May’s 0.1% ascent. The m/m/ descent was driven largely by energy, which sank by 1.7%, and the food, alcohol and tobacco category, which slipped 0.2% due to a 0.9% drop in processed foods. Stickers for non-energy industrial goods, furthermore, sank 0.2%. The services sector bucked the trend with prices up 0.4%. The y/y print moderated, in part due to energy, after a 10.8% May increase, being up only 8.7%. Annualized inflation for services, furthermore, slowed from 3.5% in May to 2.2% last month.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures, event contracts, and forecast contracts are not suitable for all investors. Before trading these products, please read the CFTC Risk Disclosure. For a copy, visit our Warnings and Disclosures Page.

Investments in certain commodities (precious metals) may be subject to significant price volatility and often involve risks related to market fluctuations, liquidity constraints, geopolitical events, and changes in global economic conditions that could adversely affect their value.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!