- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted June 24, 2026 at 1:49 pm

A recovery in commercial traffic along the Strait of Hormuz is sparking a Treasury rally as inflation concerns are being quelled by crude oil plunging below $70 a barrel. The shipping rebound is raising optimism about the potential for a lasting peace deal between Washington and Tehran while stoking animal spirits on Wall Street. The relief in price-pressure expectations has duration leading today’s robust fixed-income performance as yields descend in bull-flattening motion led by the longer tenors. Modest short-end gains combined with a strengthening greenback are signaling that new Fed Chair Kevin Warsh is unlikely to be too impressed by sinking energy costs and likely wants to see broader progress in subduing goods and services charges prior to lightening his hawkish stance. Stocks are loving it, however, as a broad climb throughout the benchmarks has 10 of the 11 major sectors advancing amidst the Russell 2000 jumping to a fresh record. Tech is sluggish on a relative basis, though, as investors await an earnings report from 2026’s market leader Micron after the bell while they digest an equity offering from a key competitor, SK Hynix, which is seeking $29 billion to expand memory chip production deemed crucial for AI projects. Commodities are getting battered by favorable geopolitical developments, an appreciating dollar and a huge miss on new home sales that is adding to worries concerning real estate. Elsewhere, cryptocurrencies and volatility protection instruments are declining but prediction markets are catching bids.

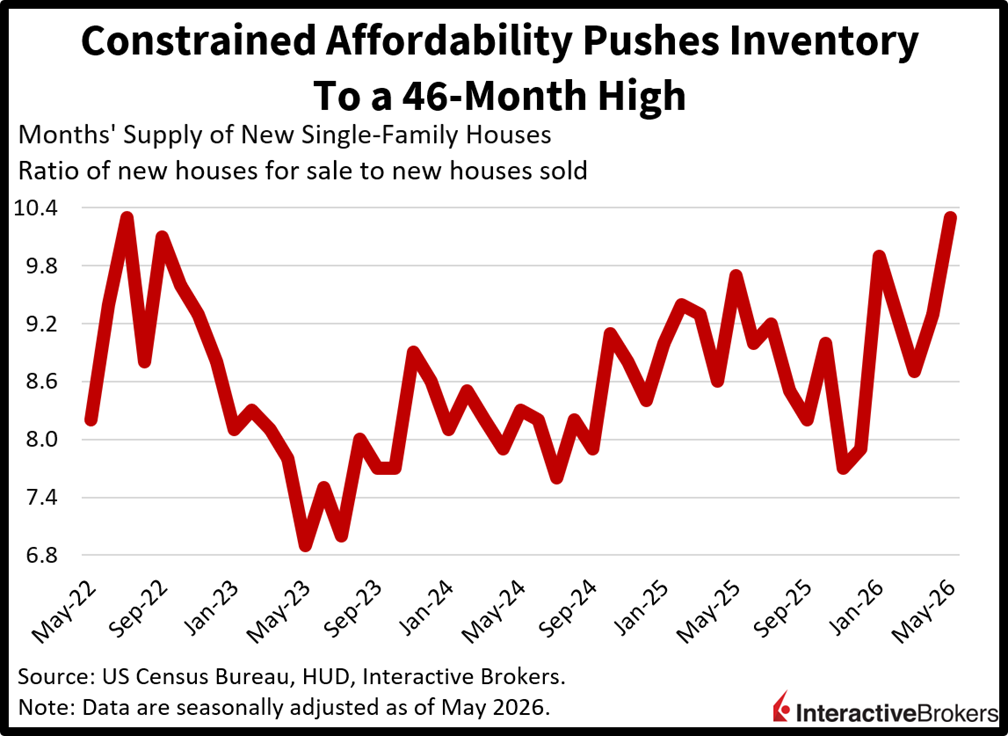

New home sales dove last month as builders faced trouble closing deals amidst constrained affordability. Lofty valuations and elevated mortgage rates pushed up inventory, which is poised to temper future construction activity. The headline, at 580k seasonally adjusted annualized units, was almost a four-year low and it was the weakest figure since January. It marked a 7.3% month-over-month (m/m) decline and fell below both the 640k estimate and April’s 627k. Regional results were bifurcated, however, with m/m decreases of 26.9% and 4.1% in the West and South while Midwest and Northeast transactions grew 16.2% and 3% m/m. More broadly, supply hit a 46-month high, with the ratio of residences for sale relative to those sold rising to 10.3 months.

The flattest yield curve in 15 months could invert by year-end if economic data disappoint against the backdrop of a Fed chair that is unlikely to quickly waver on his inflation priority in response to slowdown angst. Tomorrow’s numbers could further compress the 25-basis point (bps) spread between the 2- and 10-year maturities if heavy price pressure figures are met with sluggish consumer spending momentum. That is the expectation; however, cost statistics are better telegraphed by Wall Street than shopping details for these specific indicators, so a downside surprise on consumption is more likely than an upside inflation beat. But investors will be much more focused in the immediate term on Micron’s earnings report while especially trying to gauge the current inning of the AI revolution. Participants will seek clues about the appetite for additional capital expenditures, margins across the industry and the return prospects of the substantial investments that are being made.

The Japan economy has recovered moderately, but it continues to face pressure from high energy prices and other challenges created by the US-Iran war, according to minutes released today from last week’s Bank of Japan (BoJ) meeting. The publication, while providing an encouraging economic outlook, is also increasing investors’ expectations for the central bank to enact additional rate hikes after it lifted its key benchmark 25 bps to 1% on June 16.

Looking ahead, strong corporate profits, demand for artificial intelligence hardware, government stimulus and the development of alternative sources of raw materials are likely to offset the impact of the Middle East crisis, allowing Japan’s economy to continue growing, albeit at a decelerated pace. While noting that the Consumer Price Index has dropped below the organization’s 2% target, policymakers maintain that inflation could strengthen due to businesses passing higher costs onto consumers.

Price pressures for corporate services were up 3.3% year over year (y/y) in May, matching both the economist consensus estimate and April’s pace, according to the Services Producer Price Index from the Bank of Japan. For the month-over-month (m/m) result, prices were unchanged, which also matched April’s print. With higher energy costs following the start of the US-Iran war, transportation experienced the most significant price pressures from both a y/y and m/m perspective. Indeed, when excluding international transportation, the index was up only 3% y/y.

For the m/m result, the stickers for the transportation and postal activities categories climbed 0.6%. Within this category, international air freight, domestic air passenger transportation, international air passenger transportation and ocean freight became 12.5%, 9.3%, 4% and 3% more expensive. Other categories that became pricier and the extent of their changes were as follows:

Conversely, advertising services and the other services category declined by 1.3% and 0.1%, respectively.

Sales of manufactured items in Canada climbed only 1.1% m/m in May, a notable deceleration from the 4.2% gain in April, according to preliminary data from Statistics Canada. The motor vehicle industry group and chemical subsector posted the fastest growth in May.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Futures, event contracts, and forecast contracts are not suitable for all investors. Before trading these products, please read the CFTC Risk Disclosure. For a copy, visit our Warnings and Disclosures Page.

Trading in digital assets, including cryptocurrencies, is especially risky and is only for individuals with a high risk tolerance and the financial ability to sustain losses. Eligibility to trade in digital asset products may vary based on jurisdiction.

There is a substantial risk of loss in foreign exchange trading. The settlement date of foreign exchange trades can vary due to time zone differences and bank holidays. When trading across foreign exchange markets, this may necessitate borrowing funds to settle foreign exchange trades. The interest rate on borrowed funds must be considered when computing the cost of trades across multiple markets.

Spot currencies are not available at IBKR Singapore.

Related Articles

Simulation")

")

All that is missing is the amount of the recovery – no discussion at all. How many ships? How close to recovery of ships through the strait? >>Hormuz Traffic Recovery Sparks Treasury Rally as Oil Sinks Below $70: June 24, 2026<<