- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 27, 2026 at 1:29 pm

The article “The Skip-Month Mystery: What Last Month’s Returns Are Really Telling You” was originally published on Alpha Architect blog.

New research challenges a long-standing rule in momentum investing—and reveals surprising insights about when to use it

For decades, investors using momentum strategies have followed a simple rule: ignore last month’s returns. This “skip-month” convention has been standard practice since the 1990s, designed to avoid short-term reversal effects where stocks that jump up one month tend to fall back the next.

But what if that ignored month is actually telling you something important?

Dibyam Dikhit, author of the January 2026 paper “The Informational Role of the Most Recent Month in Industry-Level Momentum Strategies,” examined nearly 50 years of industry-level returns and found that the most recent month contains economically meaningful information—not just noise to be filtered out. The findings suggest investors should think about the skip-month rule differently: not as a universal best practice, but as a conditional tool that works better in some market environments than others.

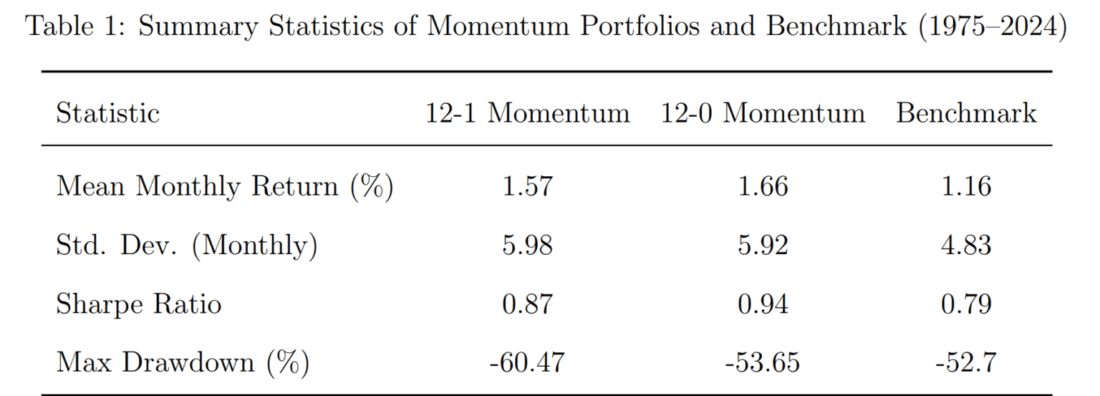

The study analyzed the Fama-French 48 industry portfolios from 1975 through 2024, comparing two momentum strategies with the analysis focusing on long-only momentum portfolios, in which returns are computed as the equal-weighted average of the selected industries during the holding month:

The 12-1 strategy (standard approach): Ranks industries based on their returns from 12 months ago through 2 months ago, explicitly excluding the most recent month. Each month, the strategy invests equally in the top 5 performing industries.

The 12-0 strategy (includes recent month): Ranks industries based on returns from 12 months ago through last month, including that most recent month in the calculation.

Rather than simply asking which strategy performed better, the researcher dug deeper: How do returns and volatility from the prior month help predict future momentum performance? And how does including or excluding that month change the strategy’s sensitivity to different market conditions?

To answer these questions, the study classified each month into regimes based on whether the previous month’s return was above or below its trailing average, and whether volatility was elevated or calm. This created four distinct market states:

1. Strong Prior-Month Returns Predict Stronger Momentum

Contrary to the conventional wisdom about short-term reversals, the study found that when the prior month delivered above-average returns, subsequent momentum performance was significantly stronger. This held true across both strategies, but the effect was more pronounced in the 12-1 portfolio.

For the 12-1 strategy, months following strong prior-month returns generated average returns of 2.03% compared to 1.28% following weak prior months—a difference of 59%. The 12-0 strategy showed the same directional pattern but with a smaller spread (1.69% versus 1.62%).

2. High Volatility Dampens Momentum—Even When Returns Are Strong

Volatility in the prior month proved to be a powerful predictor of weaker momentum performance. When the previous month was calm (below-average volatility), both strategies thrived, delivering average returns around 1.85%. But when volatility spiked, performance deteriorated sharply for the 12-1 strategy (dropping to 1.10%) while the 12-0 strategy proved more resilient (1.33%).

Interestingly, high volatility had such a dampening effect that calm months with below-average returns still outperformed turbulent months with above-average returns. This highlights volatility’s critical role in momentum persistence.

3. The Skip-Month Rule Makes Performance More Sensitive to Market Conditions

The most striking finding is that the 12-1 and 12-0 strategies don’t just perform differently—they react differently to prior-month signals. The 12-1 strategy (which excludes the recent month) showed much larger performance swings across different regimes. It delivered stronger gains when conditions were favorable but suffered steeper losses when conditions deteriorated.

By contrast, the 12-0 strategy (which includes the recent month) produced more stable returns across market regimes. This stability came from incorporating the most recent month’s information directly into portfolio formation, which appeared to smooth out extreme reactions to prior-month conditions. In addition, the 12–0 portfolio slightly surpassed the 12–1 portfolio in the full sample.

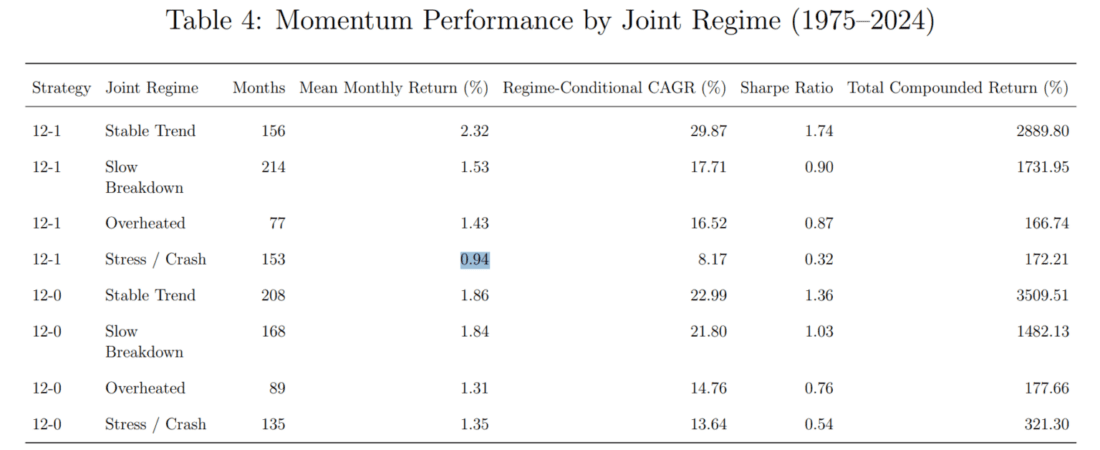

4. Market Regimes Matter: The Best and Worst Environments for Momentum

When combining return and volatility signals, clear patterns emerged:

Stable Trend (strong returns + low volatility): The ideal environment for momentum. The 12-1 strategy soared with 2.32% average monthly returns.

Stress/Crash (weak returns + high volatility): The worst environment. The 12-1 strategy managed only 0.94% average returns, while 12-0 held up better at 1.35%.

Slow Breakdown and Overheated: Intermediate regimes showed moderate momentum performance.

Across these joint regimes, the 12-0 strategy displayed remarkably consistent mean returns (ranging from 1.31% to 1.86%), while the 12-1 strategy swung more dramatically (0.94% to 2.32%).

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

His findings led Dikhit to conclude:

“While the study focuses on long-only industry portfolios and does not incorporate transaction costs, leverage, or shorting, the results provide clear evidence that the most recent month carries predictive value.”

1. The Skip-Month Rule Isn’t One-Size-Fits-All

The conventional skip-month rule serves a purpose, but it’s not universally optimal. The research suggests a conditional approach: consider using the 12-1 strategy (excluding the recent month) when the prior month showed strong performance, as this amplifies momentum continuation. But when the prior month was weak, the 12-0 strategy (including the recent month) may be preferable, as it stabilizes returns and reduces downside exposure.

2. Pay Attention to Recent Volatility, Not Just Returns

Volatility in the most recent month proved to be as important as—if not more important than—the direction of returns. High volatility consistently predicted weaker momentum performance, even when returns were positive. Investors should monitor not just whether the market is up or down, but how bumpy the ride has been.

3. Momentum Works Best in Stable Uptrends

The Stable Trend regime—characterized by strong recent returns and calm markets—delivered the best momentum performance by far. During these periods, the 12-1 strategy generated compound annual growth rates exceeding 29%. Conversely, Stress/Crash environments (weak returns plus high volatility) were clearly unfavorable, producing returns less than half that level.

4. Consider Stability vs. Sensitivity in Portfolio Design

Investors face a trade-off: the 12-1 strategy offers higher upside in favorable conditions but greater downside in unfavorable ones, while the 12-0 strategy provides more consistent performance across market regimes. Your choice should depend on your risk tolerance and ability to dynamically adjust strategies based on market conditions.

5. The Most Recent Month Contains Diagnostic Information

Perhaps the most important insight is that the most recent month shouldn’t be dismissed as mere noise. It provides valuable signals about market conditions, trend strength, and momentum persistence. Rather than mechanically excluding this information, sophisticated investors can use it to understand and potentially predict how their momentum strategies will perform in the near term.

This research reframes the skip-month convention from a universal best practice to a conditional tool. The most recent month’s behavior—both its returns and its volatility—contains meaningful information about near-term momentum outcomes. By paying attention to these signals, investors can better understand when their momentum strategies are likely to thrive or struggle.

The implications extend beyond just choosing between 12-1 and 12-0 strategies. The findings suggest that adaptive approaches—which adjust strategy parameters based on recent market conditions—may offer advantages over static rules. As markets evolve, so too should our strategies for capturing momentum.

For momentum investors, the message is clear: don’t just skip the most recent month out of habit. Understand what it’s telling you about market conditions and use that information to your advantage.

Larry Swedroe is the author or co-author of 18 books on investing, including his latest Enrich Your Future. This article is for informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

This site provides NO information on our value ETFs or our momentum ETFs. Please refer to this site.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Alpha Architect and is being posted with its permission. The views expressed in this material are solely those of the author and/or Alpha Architect and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!