- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted November 25, 2025 at 12:58 pm

Downbeat economic data is delivering gains to stock and bond bulls alike as weaker-than-expected retail sales and consumer confidence numbers coincide with accelerating job losses and rising odds of a December Fed cut as a result. Meanwhile, a largely in-line PPI report signaled that inflationary pressures remain strong, but concerns over household budgets and worries about increasing unemployment dominated the narrative. The potential for a cyclical deceleration has investors buying Treasuries with a long-end bias, as the curve shifts south in bull-flattening fashion, providing additional support to equities. Indeed, the Russell 2000 and Dow Jones Industrial indices are advancing strongly amidst 10 of the 11 major equity sectors climbing. Technology was selling off before recovering, however, as intensifying competition in the race to develop the best AI semiconductors sends Nvidia heavily into the red following the news that Meta is considering using Google’s chips. Softening activity prospects are driving commodity prices lower, while evidence suggesting that Kyiv and Moscow are closer to a peace deal causes energy costs to plunge. A lack of speculative enthusiasm continues to curb bitcoin and offensive trading postures are lightening demand for volatility protection instruments, while narrowing central bank differentials and sluggish domestic statistics hamper the greenback. Forecast contracts are catching bids and signal an 84% chance that the Fed will reduce its benchmark next month.

Private sector payrolls declined by an average of 13,500 workers in each of the four weeks during the period ended Nov. 8, according to ADP. The result is an acceleration from the 2,500-job loss in the weekly average released seven days ago.

Consumer spending slipped in September, according to this morning’s Census Bureau retail sales report. Transactions declined 0.2% month over month (m/m), missing the 0.4% median estimate and arriving beneath August’s 0.6%. Of the 13 major categories, 8 produced m/m growth as follows:

Conversely, sporting goods destinations, ecommerce, apparel shops, electronics places and automobile dealerships experienced decreases of 2.5%, 0.7%, 0.7%, 0.5% and 0.3%.

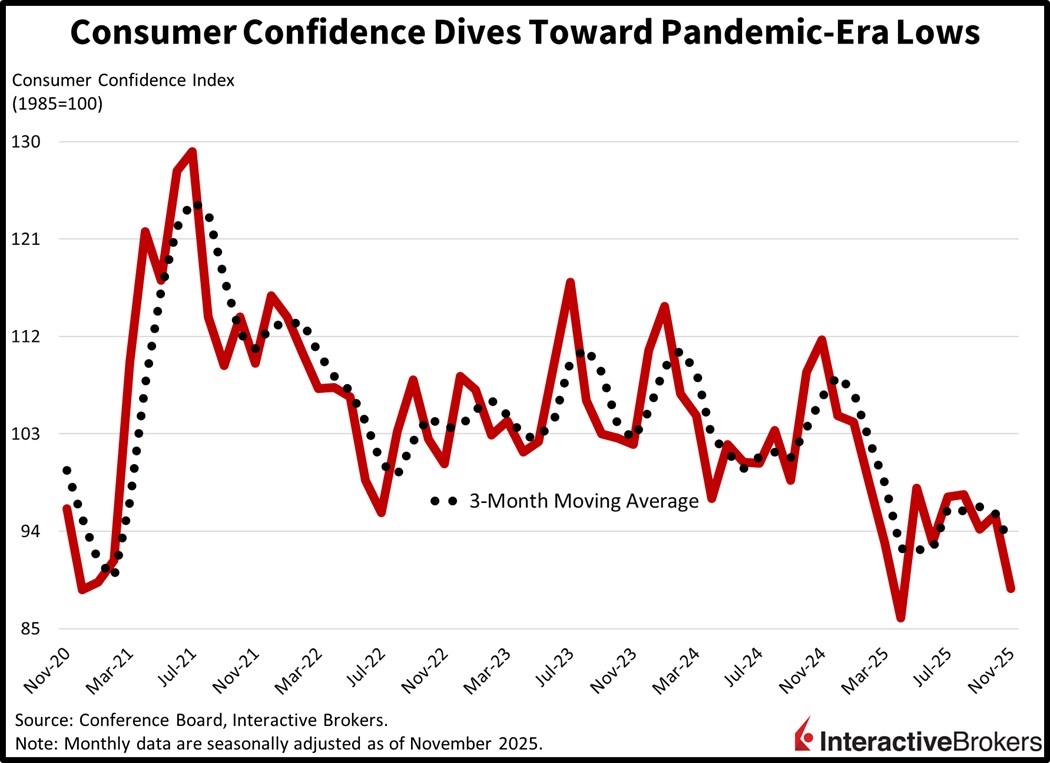

Consumer confidence plunged and is approaching some of the lowest numbers since the depths of the pandemic. The Conference Board’s headline number of 88.7 arrived below both the projected 93.4 and October’s 95.5 by wide margins, the weakest result since April. Survey respondents reported broad unease about the economy, as the sub-indices for present situations and expectations declined from 131.2 and 71.8 to 126.9 and 62.2, indicating that the anxiety about the road ahead worsened notably. Folks mentioned worries regarding job security, employment availability, inflation, the government shutdown and their current financial state.

The pace of home price gains slowed further in September based on the FHFA and S&P/Case-Schiller data. Increases decelerated year over year (y/y) to 1.7% and 1.4%, respectively, slower than August’s 2.4% and 1.6%. There was no expansion in the m/m results, however, with the former data source reporting an unchanged statistic while the latter noted a 0.5% decline. But the alleviating valuations and improving inventories have yet to bolster transactions much, as this morning’s pending home sales metric beat the 0.5% expectation with a 1.9% m/m increase, but it remained 0.4% lower y/y.

The S&P 500 is trading at 6752 right now and is well above its closely watched 50-day moving average at 6715 as well modestly north of its 20-day, which stands at 6,746. A close near these levels would significantly repair the technical damage in the charts of the last few week and set up equities for a year-end rally. Another large batch of economic data is due out tomorrow, but once again, the likelihood of a disappointment is pretty subdued since the publications have been meaningfully delayed and aren’t a high priority. Meanwhile, favorable seasonals are conducive to glass-half full perspectives amongst investors that are poised to drive stocks higher.

Hong Kong’s trade deficit sank from $50.2 billion in September to $39.9 billion last month with both exports and imports hitting record high levels, according to the Census and Statistics Department.

Year to date as of the end of October, exports grew 13.8%, outpacing the 13.6% jump in imports.

The value of goods sold to foreign customers in October climbed 17.5% y/y, accelerating from 16.1% in September. The following countries, along with their growth of purchases from the special administrative region, provided the most significant contributions to the y/y result:

Among items shipped abroad, the telecommunications and sound recording and reproducing apparatus and equipment category and the electrical machinery, apparatus and appliances, and electrical parts classification grew 35.7% and 16.1%.

The value of items flowing into Hong Kong, meanwhile, climbed 18.3% y/y in October, up significantly from the 16.1% jump in the preceding period. Purchases of items from Vietnam, the UK and Malaysia led the y/y print with gains of 189.1%, 55.7% and 25.1%. Singapore and China, furthermore, experienced 20.8% and 18.4% upticks while imports from the US sank 10.4%. The office machines and automatic data processing machines category and the electrical machinery, apparatus and appliances, and electrical parts thereof group led the increase in items flowing into the country, expanding 30.1% and 16.8%, respectively.

The South Korea Composite Consumer Sentiment Index climbed to 112.4 in November, up 2.6 points from last month, a result, in large part, of improved opinions about the country’s economy. Views of current and future domestic economic conditions were up five and eight points, respectively, relative to October. Expectations of future household income and living standards also advanced with gains of two points and one point, respectively. In other results, current living standards and expectations for future purchases were unchanged at 96 and 110. Survey respondents, furthermore, anticipate inflation rates of 2.6% for 2025 and a 2.5% for both the coming three-and five-year periods.

The percentages of Canadian businesses that are promoting domestically made products has jumped significantly while domestic air travel has surged as the number of flights between the country and the US sank, according to data released today from Statistics Canada. During the past six months, 20% of businesses reported placing a stronger emphasis on marketing Canadian products, according to the Survey on Business Conditions. The shift comes as the country’s relationship with the US is strained due to the trade dispute and other issues. During the same period, 13% of businesses experienced stronger sales of domestic products. Among sectors, 30.3% and 22.2% of retailers and manufacturers noticed the shift.

In other topics, 61.2% of businesses said they expect cost-related obstacles during the current quarter. These challenges include interest rates, input costs, inflation and higher expenses for insurance, transportation and real estate. Additionally, 39.9% of survey respondents intend to pass tariff costs on to customers.

Also today, Canada reported that domestic air travel in September was 5% above the volume of the year-ago period, marking the first month in which the metric exceeded pre-Covid-19 levels. It was the sixth consecutive monthly increase. International flights excluding the US were 6.4% higher y/y but volume of travel to the US sank 3.5%.

Weak results for the food, beverage and tobacco subsector and the agricultural supplies industry group caused the total value of wholesale transactions minus petroleum, oilseed and grain to fall 0.1% last month, according to an advance estimate of Statistics Canada.

Sentiment in the UK retailing sector descended by the greatest extent in 17 years this month with disappointing sales weighing on the Confederation of British Industry’s CBI Distributive Trades Survey. Among respondents, 35% expect conditions will worsen this quarter. Sales this month were rated as poor and December sales are expected to have disappointing holiday results. Retailers also reduced staffing and plan to cutback on investing and hiring. In a press release, CBI Chief Economist Alpesh Paleja maintained uncertainty about the country’s next budget, which many observers believe will require tax increases to plug an anticipated funding shortfall, is causing businesses to hold back on investment and hiring while households are cautious about day-to-day spending.

New to Interactive Brokers?

Open AccountInformation posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!