- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted October 24, 2025 at 1:31 pm

Investors are grabbing the bull by the horns after this morning’s lighter-than-anticipated CPI bolstered the case for a series of rate cuts this year and next. The print underscored the fact that tariff-sensitive areas of the landscape aren’t substantial enough to meaningfully alter price levels across the economy. Indeed, the core segment of the publication increased at the slowest pace since May, as the disinflationary impact of housing suppressed overall cost pressures. Animal spirits are additionally strengthening due to robust corporate earnings alongside S&P Global Flash PMIs signaling a reacceleration in activity, as the services and manufacturing segments ramped up and easily beat forecasts. Meanwhile, optimism that Washington and Beijing can improve cross-border commerce relations in a few days during a widely anticipated Trump-Xi meeting is supporting risk-on sentiment. And confidence that a deal is nearing with New Delhi is countering the impact of suspended communication with Ottawa after its government published a video advertisement criticizing levies and featuring a segment of late President Ronald Reagan advocating free trade. The US commander in chief opined that the move was “egregious behavior” designed to influence an incoming Supreme Court decision on duties, and he disclosed that he has ended talks with Canadian leaders. Stocks are trading at all-time highs and every sector is advancing minus energy. Treasuries were also climbing, but an intraday update from UMich depicting rising inflation expectations over the longer run is paring gains for duration. Still, the yield curve is descending in bull-steepening fashion led by the monetary policy responsive shorter tenors, as fixed-income watchers pencil in two quarter-point Fed reductions in 2025 and around three in 2026. The greenback is appreciating as well on firmer relative growth differentials, which are also benefiting cyclical commodities. A return of speculative excitement has bitcoin and forecast contracts catching bids too, but the safe-haven characteristics of gold, silver and volatility protection instruments are being neglected in light of offensive winds on Wall Street.

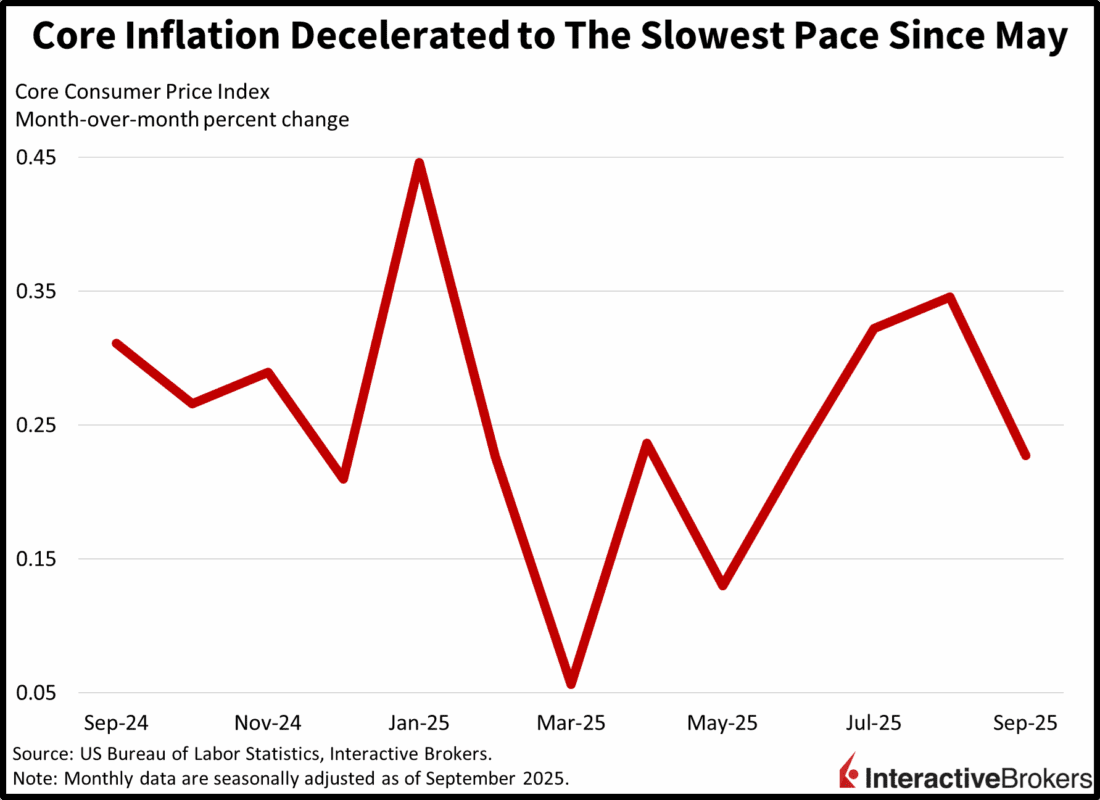

Core CPI Decelerates to Slowest Pace Since May

September’s Consumer Price Index (CPI) rose 0.3% month over month (m/m) and 3% year over year (y/y), while the core segment, which excludes food and energy due to their volatile characteristics, increased 0.2% and 3%. All four numbers arrived below expectations by 0.1% while the monthly figures decelerated m/m by the same 0.1% amount. Annualized results shifted in bifurcated fashion, meanwhile, as the previous print posted 2.9% for headline and 3.1% for core. Helping to drive the headline miss were deflationary outcomes in used automobiles and the electricity/heating category, with cost declines of 0.4% and 0.7% m/m. Another significant development came from decelerating housing pressures, as shelter slowed from a 0.4% rate in August to 0.2% last month. Elsewhere, gasoline, apparel, food at markets, transportation services, medical care services, new cars and drinking/dining establishments saw charges increase 4.1%, 0.7%, 0.3%, 0.3%, 0.3%, 0.2% and 0.1% m/m.

Economic growth is thriving at the second fastest pace of the year with new orders driving beats across both categories of the S&P Global Flash Purchasing Managers’ Index (PMI) and countering the impacts of the government shutdown. The headline scores for services and manufacturing accelerated to 55.2 and 52.2 from 54.2 and 52, exceeding expectations for 53.5 and 52. The results were well ahead of the contraction-expansion threshold of 50. Hiring improvements were able to offset the negative forces of worsening business confidence and compressing margins, as firms increasingly competed for sales as signaled by rising input costs amidst stabilizing selling charges. Employment gains were contained by a lack of suitable candidates, however, and declines in sentiment were limited by optimism about lighter interest rates. Conversely, exports suffered as tariffs and weaker activity from international economies weighed on transactions.

Markets are poised to rally into year-end as an accelerating economy coincides with an extended series of reductions from the Federal Reserve. The anticipated monetary policy accommodation bodes well for a broadening in equities, allowing the more cyclically oriented, rate-sensitive components to potentially begin outperforming and drive a healthier composition across the major domestic benchmarks, in which tech stocks have been dominating recently. Indeed, excitement in the Russell 2000, today’s leader amongst the indices, is emblematic of the small-cap gauge standing to benefit from loosening financial conditions while larger old-school categories are likely to also participate in appreciation. Meanwhile, October’s real-time annualized measures of inflation are trending lower, as lighter gasoline prices and positive base effects are likely to support easing projections in 2026 since 50 basis points of cuts are essentially in the bag at this point. Finally, seasonal tailwinds are right around the corner, as turkeys and Santa Claus have historically been bullish for stocks.

Eurozone manufacturing is no longer in contraction, but it is still a hair shy of expanding, according to the October HCOB Flash Eurozone Manufacturing PMI. On a broader basis, Eurozone economic activity is expanding at a faster pace than in September. The manufacturing gauge climbed from 49.8 to 50, the contraction-expansion threshold, while the PMI that focuses on the output from goods producers moved from 50.9 to 51.1. More encouragingly, the broader composite PMI climbed from 51.2 to 52.2, a 17-month high and the services sector gauge hit a 14-month high of 52.6, up from September’s 51.3. Businesses increased their activity in response to a steeper increase in orders and new business. This trend was led by services, but manufacturing demand also picked up. Employment, meanwhile, grew in services but contracted in manufacturing at the fastest pace in four months. Also discouraging, overall business confidence fell to a five-month low.

The UK’s composite PMI strengthened this month with support from both services and manufacturing sectors. The broad gauge climbed from 51.2 to 52.2, exceeding the economist consensus estimate of 51.2.

Retail sales in the UK climbed 0.5% m/m and 1.5% last month, beating the economist consensus estimates for a monthly decline of 0.2% and an annual ascent of 0.6%. In August, retailing increased 0.6% m/m and 0.7% y/y.

Singapore’s biomedical manufacturing flexed its clout last month, pushing industrial production in September past estimates following a discouraging August. Overall output in September jumped 26.3% m/m and 16.1% y/y, according to the Singapore Economic Development Board. The metrics were significantly stronger than the economist consensus estimates of 8.6% and 0.5%. In August, production dropped 11% m/m and 9% y/y.

When excluding the island-nation’s biomedical sector, industrial output last month was up 0.8% m/m and 5.4% y/y. The biomedical manufacturing group led the y/y expansion with gains of 45.9%. Within this category, pharmaceutical manufacturing activity was 55.3% higher than in the year ago period. The following categories and the extent of their increases also contributed to the headline strength:

Conversely, general manufacturing and precision engineering slipped 4.7% and 5.9%, respectively.

Declining financing costs, generational wealth transfers and investments from foreign residents supported housing demand during the third quarter and drove prices of private homes up 0.9% from the April-June period, according to the Urban Redevelopment Authority. Economists anticipated a 1.2% ascent. Nevertheless, it was the fourth consecutive quarter of price increases with the preceding period experiencing a 1% gain.

Japan Purchasing Managers Index Falls

Japan’s Manufacturing and Services PMI slipped from 51.3 in September to 50.9 month, the weakest level in five months. The manufacturing component descended further into contraction, dropping from 48.5 to 48.3 and missing the economist consensus estimate of 48.8. Services continue to grow but at a slower pace, with the sector’s PMI sinking from 53.3 to 52.4. So far this month, the rate of payroll growth slowed, business sentiment weakened and new work orders fell for both sectors. Foreign demand also weakened but the pace of the decline slowed. Businesses in both sectors reported higher input costs and raising their selling prices.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Hi I am a Canadian economist recently retired from University of Victoria, previously from UBC and now at Trinity Western U. I know how Canada should respond to U.S. tariffs, but Canadian politicians are an ignorant bunch. Here is my solution: 1. Agree to increase defense expenditures (apparently met). 2. Eliminate the dairy (egg and poultry) marketing boards. When the President talks about 200% tariffs imposed by Canada, he refers to the dairy quota regime that prevents imports. The dairy regime is known to hurt Canadian consumers and prevents dairy producers from exporting any dairy products. It is and continues to be a boondoggle benefits only a very few producers, mainly located in Quebec. 3. Agree to negotiate a true North American customs union (beginning bilateral). If Canada cannot survive in a customs union, then Canada is not a separate nation to begin with. After all, Italy, France, Netherlands, etc survive as entities within a Europe than has gone far beyond a customs union. Finally, get rid of Canadian regulations on anything to do with the environment. It is killing our economy.