- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted September 15, 2025 at 11:57 am

The article “Intelligent Concentration: A Synopsis of Warren Buffett and Diversification” was posted on Alpha Architect blog.

Warren Buffett’s diversification practices have been back in the spotlight over the past few years. Specifically, the level of concentration in his portfolio has come under scrutiny due to the size of the largest stock holding in Berkshire Hathaway’s marketable equities portfolio. A historical review of Buffett’s implementation of diversification and concentration in practice, as well as his perspective on these concepts, documents a long tradition of heterodox thinking and application.

First and foremost, Buffett unquestionably understands the value and benefits of diversification. In his 1965 annual letter, Buffett explained his ideal investment opportunity set, an explanation most finance professors can appreciate, as it demonstrates his understanding of the purpose and benefits of diversification.

“Frankly, there is nothing I would like better than to have 50 different investment opportunities, all of which have a mathematical expectation (this term reflects the range of all possible relative performances, including negative ones, adjusted for the probability of each – no yawning, please) of achieving performance surpassing the Dow by, say, fifteen percentage points per annum. If the fifty individual expectations were not intercorrelated (what happens to one is associated with what happens to the other) I could put 2% of our capital into each one and sit back with a very high degree of certainty that our overall results would be very close to such a fifteen percentage point advantage.”

But he follows up this explanation by writing:

“It doesn’t work that way.”

Identifying even 10 different investment opportunities with high expected performance is incredibly difficult. In most markets and at most times, the number of attractive investment opportunities is exceedingly small (i.e., markets are generally quite efficient or at least not inefficient). Therefore, Buffett’s portfolio has typically contained relatively few holdings. Nevertheless, an objective assessment indicates “adequate” diversification.

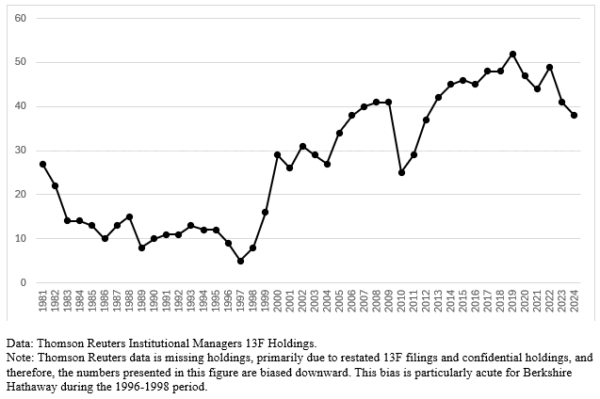

Figure 1 displays the number of holdings in Berkshire Hathaway’s marketable equities portfolio from 1981 to 2024. Over the entire period, the average number of stocks is approximately 28. There is a marked shift in the number of holdings in more recent decades, as the average more than doubles to approximately 40 from 2003 to 2024, compared to an average of approximately 15 from 1981 to 2002.[1] The ideal number of stocks in a portfolio is contingent upon the manager’s risk tolerance (both idiosyncratic risk and total risk/price variability) and desired expected return. But as Alpha Architect has noted (here and here), Berkshire Hathaway’s marketable equities portfolio has generally contained enough stocks to reduce volatility without “diworsifying.”

Figure 1: Number of Holdings in Berkshire Hathaway’s Marketable Equities Portfolio Over Time

Data: Thomson Reuters Institutional Managers 13F Holdings

Note: Thomson Reuters data is missing holdings, primarily due to restated 13F filings and confidential holdings, and therefore, the numbers presented in this figure are biased downward. This bias is particularly acute for Berkshire Hathaway during the 1996-1998 period.

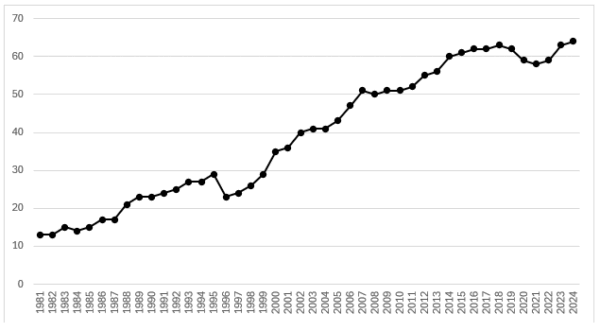

Berkshire Hathaway is even more diversified than its marketable equities portfolio suggests, as its total equity portfolio also includes numerous operating companies/subsidiaries. Figure 2 displays the number of operating companies owned by Berkshire Hathaway from 1981 to 2024. The number of operating companies has grown consistently over the past four decades, from 13 in 1981 to 64 in 2024, at a rate of approximately 1 (net) new operating company per year. The inclusion of these private holdings significantly increases the total number of holdings in Berkshire Hathaway’s total equity portfolio, growing from 40 in 1981 to 102 in 2024, with a minimum of 27 in 1986 and a maximum of 114 in 2019. As noted above, the ideal number of holdings is subjective. However, Berkshire Hathaway’s total equity portfolio has historically contained enough holdings to balance expected return and risk, and thus provides the desired benefits of diversification. Some might even argue that Buffett has overdiversified in recent decades.

Figure 2: Number of Operating Companies at Berkshire Hathaway Over Time

Data: Berkshire Hathaway Annual Reports, author’s analysis and calculations

Note: Certain operating companies with subsidiaries of their own are counted as a single company (e.g., Scott Fetzer and MidAmerican Energy Holdings Company/Berkshire Hathaway Energy Company). The sizeable drop from 1995 to 1996 is due to a reduction in the number of subsidiaries in the Insurance Group.

Much of the recent criticism surrounding Berkshire Hathaway’s portfolio is specifically related to the size of its largest holding in the marketable equities portfolio. Renowned professor of finance at NYU, Aswath Damodaran, has been particularly critical.

“… I heard that now Apple is now at 35% of Berkshire Hathaway’s holdings, and to me, you’re hitting a danger zone.”

Investing The Templeton Way 03/03/2023

“Any company that ends up with 30% of its portfolio in one company is asking for trouble … having 30% of your portfolio in one company is never a good idea … Strategically and tactically it was a bad idea to have that much money in one stock.”

“… 30% of its portfolio is Apple. I think it was just a concentration issue, which is when you have a third of your portfolio trapped in one company. It’s a very dangerous place for anybody to be.”

The irony of Professor Damodaran’s viewpoint is that a concentrated portfolio has been standard practice for nearly all of Buffett’s investing career. In 1951, while still a retail investor, Buffett had 20% of his capital invested in a local Sinclair Service Station.[2] Furthermore, at the end of 1951, 65%-75% of Buffett’s net worth was invested in GEICO shares.[3] Holdings data for Buffett’s time managing Buffett Partnership Ltd. (BPL) are unavailable. However, Buffett noted in his 1965 annual letter that, in the first nine years of his partnerships, there were five or six positions that accounted for 25% or more of his portfolio. Thus, the evidence suggests that high levels of concentration have been a staple throughout Buffett’s early investing career. Unsurprisingly, this preference for concentration subsequently continued at Berkshire Hathaway.

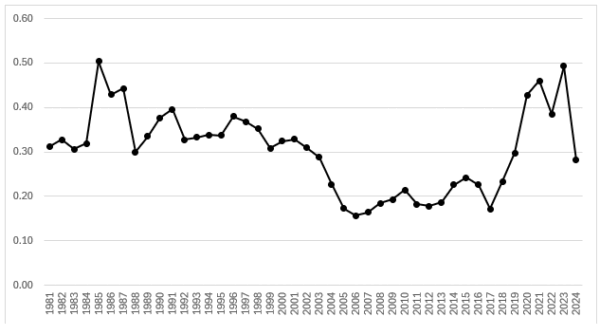

Figure 3 displays Berkshire Hathaway’s largest stock holding as a percentage of the total market value of its marketable equities portfolio at the end of each calendar year. The largest stock holding has constituted an average of approximately 30% of the marketable equities portfolio from 1981 to 2024. However, until recently, the largest stock holding has been well below average for much of the past two decades. The recent size of Apple in Berkshire Hathaway’s portfolio has approached all-time highs, but such a significant concentration in Apple is highly logical (assuming price is not significantly above intrinsic value), considering Buffett’s view of the company: “[Apple] just happens to be a better business than any we own.”

Figure 3: Berkshire Hathaway’s Largest Stock Holding as a Percentage of its Marketable Equities Portfolio Over Time

Data: Berkshire Hathaway Annual Reports

Buffett and Charlie Munger address the criticism surrounding the size of Apple in Berkshire Hathaway’s marketable equities portfolio at the 2023 annual meeting. Munger was particularly direct – “I think [Professor Damodaran] is out of his mind!” As Buffett more tactfully explained, and as discussed above, Berkshire Hathaway’s marketable equities portfolio is only a portion of its total investment portfolio. Buffett and Munger’s view of stocks is no different than that of 100% owned businesses. “They’re all businesses.” To appropriately assess concentration in Berkshire Hathaway’s portfolio, a simple adjustment to the denominator is required.

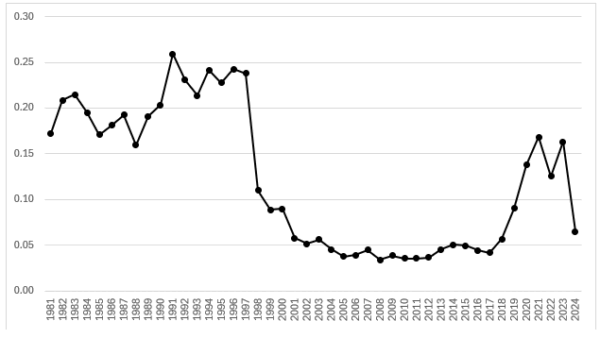

Figure 4 displays Berkshire Hathaway’s largest stock holding as a percentage of total assets at the end of each calendar year. The largest holding remains quite significant, constituting approximately 18% on average from 1981 to 2024. However, there has been a marked shift in recent decades, with the largest stock holding only averaging approximately 7% from 2003 to 2024.[4] The recent size of Apple in Berkshire Hathaway’s portfolio has only approached the long-term average and is still well below historical highs. The days of Buffett managing a truly concentrated portfolio appear to be a relic of a bygone era.[5]

Figure 4: Berkshire Hathaway’s Largest Stock Holding as a Percentage of Total Assets Over Time

Data: Berkshire Hathaway Annual Reports

The historical record indicates that Buffett has consistently preferred a highly concentrated portfolio, which most might consider unconventional. However, such a result is not unexpected. At the end of 1965, Buffett wrote to his partners at BPL to ensure that they were aware of his “unconventional (but logical)” beliefs on diversification and his preference for highly concentrated positions. Buffett added a new “Ground Rule,” the set of axioms that governed his investment partnership, to ensure all partners understood his approach and beliefs, thereby eliminating any misconceptions. The new Ground Rule stated:

“We diversify substantially less than most investment operations. We might invest up to 40% of our net worth in a single security under conditions coupling an extremely high probability that our facts and reasoning are correct with a very low probability that anything could drastically change the underlying value of the investment.”

The increase in diversification and decline in concentration over time might help explain Buffett’s relative investment performance. Figure 5 displays the rolling 60-month (5-year) annualized difference between Berkshire Hathaway’s total return and the S&P 500. From 1981 through the late 1990s, Buffett outperformed the market by a significant margin. But since the late 1990s, such outperformance has eroded with only brief intermittent periods of outperformance and at levels well below the long-term average. At least part of this deterioration can be attributed to the size of Berkshire Hathaway’s portfolio, as decreasing returns to scale are unavoidable, Buffett having noted this expectation for his shareholders for more than forty years now.[6] The deterioration in performance may also be the result of the growth of operating companies over marketable securities. Purchasing outright ownership almost always entails a price premium that reduces returns. Nevertheless, the fact that Buffett’s relative performance dissipates over the same period in which diversification meaningfully increases and concentration decreases means that it is at least a possibility that some portion of the lack of outperformance in recent years may be attributable to these factors. As Buffett once noted, diversification “will tell you how to do average.”

Figure 5: Rolling 60-Month (5-Year) Annualized Difference Between Berkshire Hathaway’s Total Return (A Shares) and the S&P 500

Data: CRSP

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Are high levels of concentration in only a few stocks (i.e., the Buffett approach) optimal? Yes! Under certain conditions.

In Buffett’s 1965 annual letter, he writes;

“We have to work extremely hard to find just a very few attractive investment situations. Such a situation by definition is one where my expectation (defined as above) of performance is at least ten percentage points per annum superior to the Dow. Among the few we do find, the expectations vary substantially. The question always is, “How much do I put in number one (ranked by expectation of relative performance) and how much do I put in number eight?” This depends to a great degree on the wideness of the spread between the mathematical expectation of number one versus number eight.” It also depends upon the probability that number one could turn in a really poor relative performance. Two securities could have equal mathematical expectations, but one might have .05 chance of performing fifteen percentage points or more worse than the Dow, and the second might have only .01 chance of such performance. The wider range of expectation in the first case reduces the desirability of heavy concentration in it.”

Buffett outlines the characteristics he believes are necessary for an investment to be attractive.[7] First, at least 10% expected returns per year greater than the market. Second, Buffett requires his potential investments to have a minimal chance (say 1% or 5%) of relatively high underperformance (15% or more). The investment opportunity set for stocks that will outperform the market by such a large margin and have such a small chance of relatively meaningful underperformance is minimal. The limited investment opportunities available under such conditions is one of the primary limitations to diversification, as generally practiced and recommended. At any given time, there are not 50 stocks, and probably not even 30 stocks, that can be identified ex-ante, meeting Buffett’s criteria. Nevertheless, the characteristics described by Buffett provide the basis for an intriguing hypothetical to test the level of diversification and concentration that is mathematically optimal.

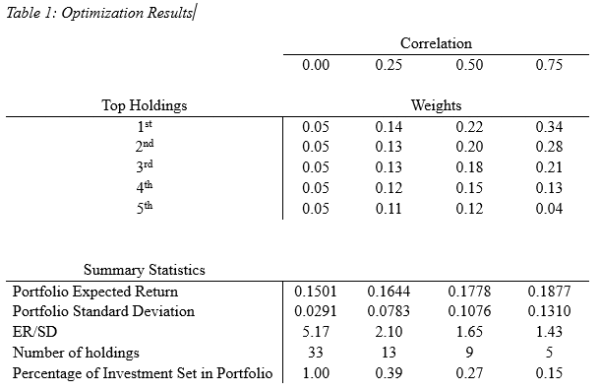

The setup: a hypothetical investment set of 33 stocks, a reasonable pool considering the characteristics. The 33 stocks have the following attributes: excess (above-market) expected returns that range from 20% to 10%, in 1% increments, with three different levels of standard deviation for each return level. The standard deviations are derived from the chance of underperformance at levels of 1%, 5%, and 10%. These probabilities result in z-scores of 2.33, 1.65, and 1.29, due to the areas to the left of the negative value of each z-score being 0.0099, 0.0495, and 0.1003, respectively. As an example, the three stocks with 20% expected excess returns have standard deviations of 15.02%, 21.21%, and 27.13%. This investment set is incredibly attractive as an equally weighted portfolio has an expected excess return (above-market) of 15% and a standard deviation of 15.81%. Such a portfolio rivals the “God Portfolio” of Alpha Architect.

Table 1 presents the results of mean-variance optimization for this hypothetical investment set, calculated using excess (above-market) expected returns and standard deviations, and assuming a pure interest rate of zero, as the returns are already in excess of the market return. The optimization process is conditional upon the variance-covariance matrix and thus, the level of correlation between the potential investments. With the “correct” value for correlation unknown, the optimization is conducted at varying levels of correlation. Table 1 displays the results. With no correlation, the portfolio holds all 33 stocks, maintaining a minimal concentration among the five largest holdings. As correlation increases, the top holdings become increasingly concentrated, and the number of holdings, and therefore the level of diversification, decreases. With moderate to high correlation, the portfolio holds very few stocks and becomes highly concentrated, with weights remarkably similar to those in Buffett’s BPL and Berkshire Hathaway portfolios. The optimal level of diversification and concentration depends on the investment opportunity set and the level of correlation among those opportunities. However, under certain conditions, such as those expressly suggested by Buffett, minimal diversification and significant concentration are optimal.

Table 1: Optimization Results

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

It is essential to emphasize that this synopsis does not suggest that most investors, professional or otherwise, should construct portfolios consisting of only a few highly concentrated equities. On the contrary, the vast majority of investors should indeed have low-cost, highly diversified portfolios. Buffett has said so himself on numerous occasions. “On the other hand, if you are a know-something investor, able to understand business economics and to find five to ten sensibly priced companies that possess important long-term competitive advantages, conventional diversification makes no sense for you.” Emphasis added to accentuate the key conditions and skills necessary for successful investment in a concentrated portfolio. Misguided examples such as the “catastrophic concentration” portfolio blatantly disregard these necessary conditions as they contain stocks that were undoubtedly not sensibly priced, almost certainly lacked any articulable long-term competitive advantages, and exhibited incomprehensible business economics (at least in the case of Enron), thus unequivocally not meeting Buffett’s return and risk characteristics. Investors, whether professional or otherwise, will need to conduct a sincere and critical self-examination to determine whether they possess the essential skills required for successful investment in concentrated portfolios before employing such an approach.

Lloyd Everhart is a self-taught security analyst in the tradition of Benjamin Graham with a passion for investing and a focus on the equity markets. He holds a BA in History from George Mason University.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Third party information may become outdated or otherwise superseded without notice. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency has approved, determined the accuracy, or confirmed the adequacy of this article.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

Join thousands of other readers and subscribe to our blog.

[1] The increase in the number of equity holdings in recent decades is likely at least partially attributable to the addition of investment managers at Berkshire Hathaway outside of Buffett and Munger, such as Lou Simpson, Todd Combs, and Ted Weschler.

[2] Warren Buffett Lecture at the University of Florida School of Business, October 15, 1998. According to Buffett’s 1998 estimate, this was a roughly $6 BILLION mistake.

[3] Warren Buffett’s 1995 Letter to Berkshire Shareholders and Alice Schroeder’s The Snowball: Warren Buffett and the Business of Life.

[4] The beginning of this shift occurred in 1998 with the acquisition of General Re as total assets more than doubled.

[5] The reduced level of concentration is likely at least partially attributable to the sheer size of Berkshire Hathaway’s capital base. By the late 1990s, a 20% position would have been approaching $10B. In 2024, a 20% position would be above $200B. For context, there are only a few hedge funds with total assets under management greater than $200B. The universe of stocks that can accommodate such large positions is exceptionally small and almost certainly does not include companies that can reasonably be considered undervalued. The practicality of getting such large sums into a single stock, from trading frictions, price movements, and disclosure, is likely unfeasible.

[6] “We are certain that the rate of per-share progress will diminish in the future – a greatly enlarged capital base will see to that.” – Warren Buffett’s Annual Letter to Shareholders 1983

“You can be certain that this percentage will diminish in the future. Geometric progressions eventually forge their own anchors.” – Warren Buffett’s Annual Letter to Shareholders 1982

[7] Ironically (or maybe not), Buffett’s performance while managing BPL is strikingly similar to the characteristics he articulates as attractive investment situations.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

This site provides NO information on our value ETFs or our momentum ETFs. Please refer to this site.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Alpha Architect and is being posted with its permission. The views expressed in this material are solely those of the author and/or Alpha Architect and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!