- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted September 3, 2025 at 12:50 pm

Implied volatility (IV) is a critical metric in options trading and financial risk management, reflecting the market’s expectation of the future price fluctuations of an underlying asset. Unlike historical volatility, which is based on past price data, IV must be inferred from market prices using a pricing model such as Black-Scholes.

This article presents the theoretical formulation of IV and demonstrates its computation using the Newton-Raphson method with Vega, while addressing edge cases where Vega is small through a hybrid Newton-Raphson and Bisection approach. Python implementations, convergence tables, and visual examples are provided to illustrate the practical computation, convergence characteristics, and key phenomena such as the volatility smile and the relationship between IV and option prices.

Implied volatility (IV) represents the market’s consensus regarding the expected magnitude of future price movements of an underlying asset. In contrast to historical volatility, IV is derived from current option prices using models like Black-Scholes and is expressed as an annualized standard deviation of returns.

Accurate estimation of IV is essential for option pricing, risk assessment, and the development of trading strategies. It enables traders and analysts to interpret market sentiment, identify potentially mispriced options, and design hedging or speculative positions effectively.

Computing IV is inherently challenging because the Black-Scholes pricing formula is nonlinear in volatility, preventing a closed-form solution. Numerical methods, particularly the Newton-Raphson iterative procedure leveraging Vega—the sensitivity of the option price to volatility—are widely used for rapid and precise estimation. However, in scenarios where Vega is extremely small, such as deep in-the-money or out-of-the-money options or near expiration, Newton-Raphson may fail to converge. To address this, a hybrid approach combining Newton-Raphson with Bisection provides a robust and efficient solution.

This article outlines a comprehensive framework for IV computation, supported by Python implementations, convergence illustrations, and visual examples. Key behaviors, including the volatility smile and the relationship between IV and option prices, are discussed to provide practical insights for market participants and researchers.

The Black–Scholes partial differential equation (PDE) describes the theoretical price of an option over time:

For a European call option:

For a European put option:

where

and

The Newton-Raphson method iteratively solves for the root of a function using its derivative:

Here, is the difference between the Black-Scholes price and the market price:

The derivative of the function with respect to volatility is known as Vega:

where

Key Point: In actual implementation, Vega is recalculated at each iteration using the current estimate of . This ensures accurate adjustment of and reliable convergence of the Newton-Raphson method.

def newton_iv(option_class, spot, strike, rate, dte, callprice=None, putprice=None):

x0 = 0.2

tolerance = 1e-7

maxiter = 200

if (callprice is not None) == (putprice is not None):

raise ValueError("Exactly one of callprice or putprice must be provided")

for i in range(maxiter):

opt = option_class(spot, strike, rate, dte, x0)

if callprice:

f = opt.callPrice - callprice

else:

f = opt.putPrice - putprice

vega = opt.vega

if abs(vega) < 1e-14: # fallback if Vega too small

break

x1 = x0 - f / vega

if abs(x1 - x0) <= tolerance * abs(x1):

return x1

x0 = x1

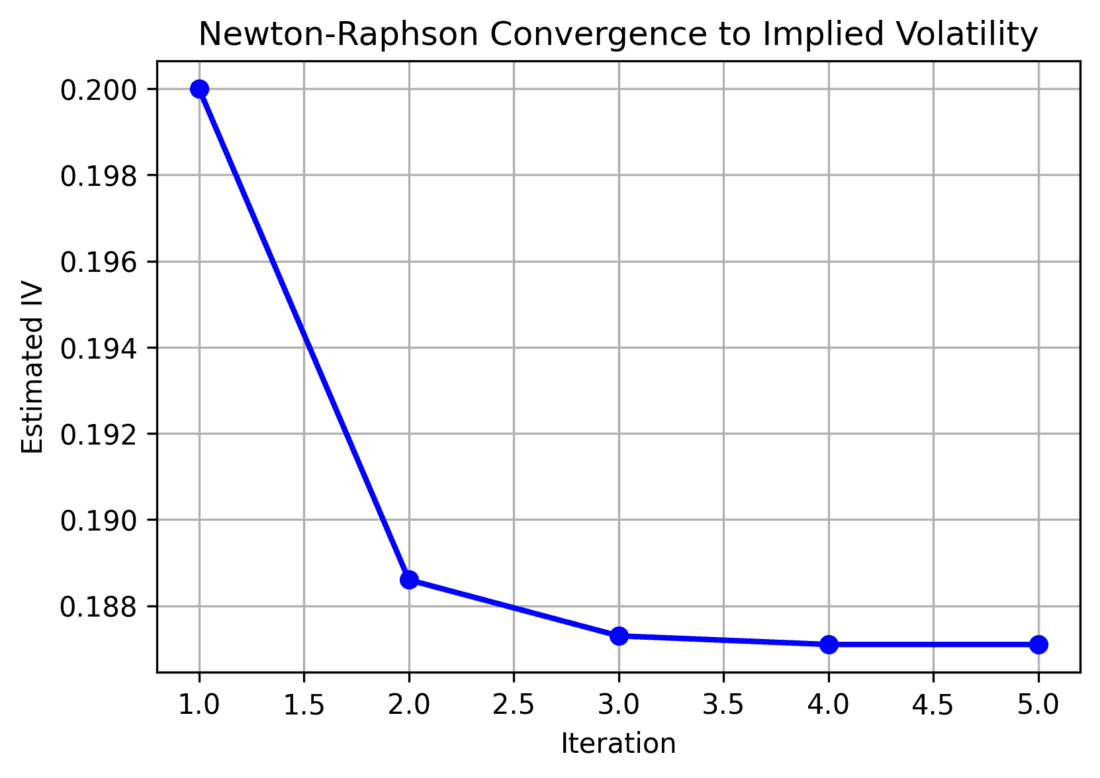

return x1Newton-Raphson Iterations for IV Calculation

| Iteration | Estimate σn | f(σn) | Vega f'(σn) |

|---|---|---|---|

| 1 | 0.2000 | 0.512 | 0.45 |

| 2 | 0.1886 | 0.123 | 0.44 |

| 3 | 0.1873 | 0.010 | 0.44 |

| 4 | 0.1871 | 0.0003 | 0.44 |

| 5 | 0.1871 | 0.0000 | 0.44 |

Illustration of Newton-Raphson iterations converging to implied volatility. Rapid convergence is observed within a few iterations.

Convergence Insights:

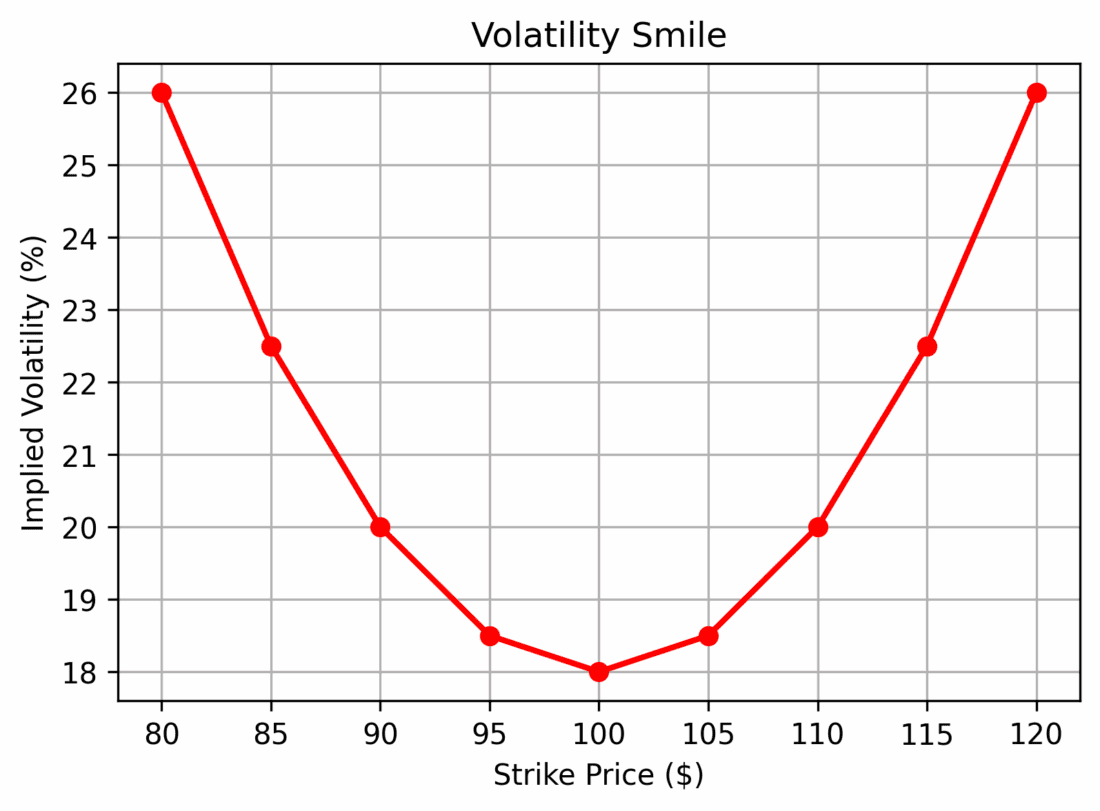

Volatility smile: Implied volatility varies across strike prices, often higher for out-of-the-money options. Traders use this to identify relatively cheap or expensive options.

Key Insights:

Call option price increases as implied volatility rises. Higher IV implies higher potential price swings.

Key Insights:

The Newton-Raphson method is highly efficient for computing implied volatility, offering rapid convergence when the option’s Vega—the sensitivity of price to volatility—is sufficiently large. In most scenarios, only a few iterations are needed to reach high precision.

However, in certain edge cases, Newton-Raphson alone can fail:

To address these challenges, a hybrid approach combining Newton-Raphson with Bisection is employed:

Benefits of the Hybrid Method:

In summary, the hybrid model is both efficient and fail-safe, providing a practical solution for real-world implied volatility computation where numerical stability is critical.

For edge cases where Vega is very small (deep in-the-money/out-of-the-money options, or near expiry), the Newton-Raphson method may fail to converge. To handle such cases, a hybrid approach combining Newton-Raphson with Bisection is used:

This hybrid method provides both speed and robustness for computing implied volatility.

def hybrid_iv(option_class, S, K, r, T, market_price, tol=1e-7, maxiter=200):

sigma = 0.2

low, high = 1e-5, 5.0

for i in range(maxiter):

option = option_class(S, K, r, T, sigma)

f = option.callPrice - market_price

vega = option.vega

if abs(vega) < 1e-6:

sigma = (low + high) / 2

else:

sigma = sigma - f / vega # Newton-Raphson update

sigma = max(low, min(high, sigma))

if abs(f) < tol:

break

if f > 0:

high = sigma

else:

low = sigma

return sigma

iv = hybrid_iv(BS, S=100, K=100, r=0.02, T=1, market_price=8)

print(f"Calculated Implied Volatility: {iv:.6f}")

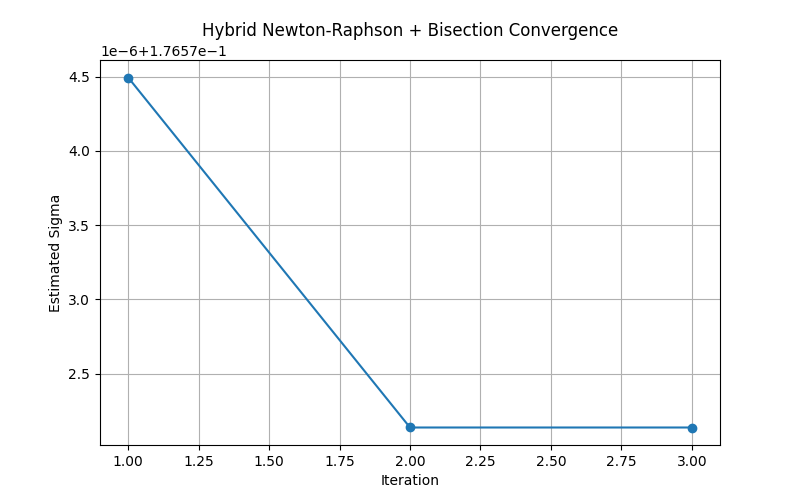

Hybrid Newton-Raphson + Bisection iterations converging to implied volatility.

Key Insights:

Current Bisection Fallback: The bisection step in the hybrid IV calculation is currently triggered only when Vega < 10-6. However, it does not iterate fully until convergence.

Production Recommendation: In real-world implementations, it is common to alternate adaptively between Newton-Raphson and bisection methods rather than switching just once. This ensures both robustness and reliable convergence across all option types and edge cases.

Current bisection fallback is only triggered when Vega < 1e-6, but it doesn’t iterate fully until convergence. In production, you’d typically alternate between NR and bisection adaptively, not just switch once.

Implied volatility (IV) is a cornerstone metric in options pricing, reflecting market expectations of future price fluctuations. Accurate computation of IV is essential for trading strategies, risk management, and hedging decisions.

This article presented a comprehensive framework for IV calculation:

The hybrid approach combines speed and stability, making it suitable for real-world scenarios where numerical precision and reliability are critical. Recalculating Vega at each iteration further ensures accurate and consistent IV estimates.

In summary, this framework equips analysts and traders with the tools to efficiently compute implied volatility, interpret market expectations, and make informed decisions in options markets.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Quant Insider and is being posted with its permission. The views expressed in this material are solely those of the author and/or Quant Insider and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Options involve risk and are not suitable for all investors. For information on the uses and risks of options, you can obtain a copy of the Options Clearing Corporation risk disclosure document titled Characteristics and Risks of Standardized Options by going to the following link ibkr.com/occ. Multiple leg strategies, including spreads, will incur multiple transaction costs.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!