- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted August 27, 2025 at 10:16 am

The article “Calculate Synthetic NBBO from Prop Feeds“ was originally published on DataBento blog.

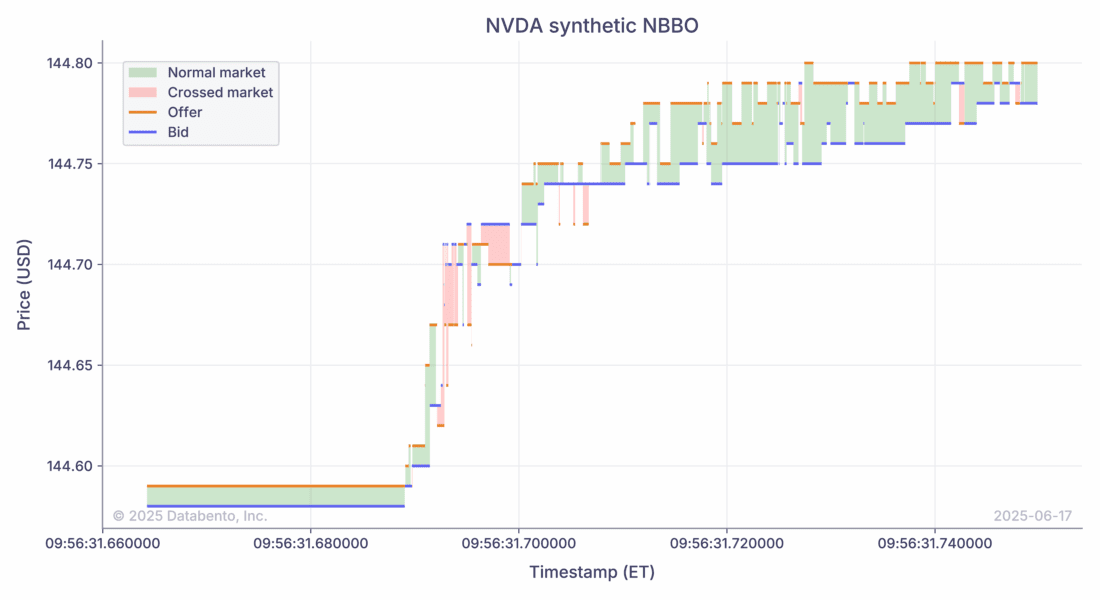

In this example, we will calculate a synthetic NBBO by taking the best bid and offer seen across the different exchanges. Unlike the official SIP NBBO which ignores odd lots and is calculated by CTA and UTP in their datacenters, this synthetic NBBO is derived from the direct prop feeds. Databento provides top-of-book coverage for all equity exchanges (except LTSE, which only provides <0.01% of total market volume). Databento captures all equity data in the NY4 datacenter with PTP timestamps. See our timestamping guide for more information.

We’ll use the MBP-1 schema and download data for the different equity exchanges. Next, we’ll process the data sequentially based on ts_recv, which is the timestamp when Databento received the data from the exchange. We’ll calculate the synthetic NBBO by taking the best bid and offer across these exchanges. After that, we’ll plot this over a 100-millisecond window to take a closer look at how the synthetic NBBO reacts when price moves.

import os

from collections import defaultdict

from dataclasses import dataclass, field

from heapq import merge

from typing import Union

import databento as db

import matplotlib.dates as mdates

import matplotlib.pyplot as plt

import pandas as pd

@dataclass()

class PriceLevel:

price: float

size: int = 0

count: int = 0

update_time: int = 0

def __str__(self) -> str:

return f"{self.size:4} @ {self.price:6.2f} | {self.count:2} order(s)"

@staticmethod

def _bid_sort(r) -> tuple[float, int, int]:

return r.price, r.size, -r.update_time

@staticmethod

def _ask_sort(r) -> tuple[float, int, int]:

return -r.price, r.size, -r.update_time

@dataclass()

class MbpBook:

offer: Union[PriceLevel, None] = field(default=None)

bid: Union[PriceLevel, None] = field(default=None)

def bbo(self) -> tuple[Union[PriceLevel, None], Union[PriceLevel, None]]:

return self.bid, self.offer

def apply(self, mbp1: db.MBP1Msg) -> None:

level = mbp1.levels[0]

ts_recv = mbp1.ts_recv

if level.bid_px == db.UNDEF_PRICE:

self.bid = None

else:

self.bid = PriceLevel(level.pretty_bid_px, level.bid_sz, level.bid_ct, ts_recv)

if level.ask_px == db.UNDEF_PRICE:

self.offer = None

else:

self.offer = PriceLevel(level.pretty_ask_px, level.ask_sz, level.ask_ct, ts_recv)

@dataclass()

class MbpMarket:

books: defaultdict[int, defaultdict[int, MbpBook]] = field(

default_factory=lambda: defaultdict(lambda: defaultdict(MbpBook)),

)

def get_book(self, instrument_id: int, publisher_id: int) -> MbpBook:

return self.books[instrument_id][publisher_id]

def bbo(

self,

instrument_id: int,

publisher_id: int,

) -> tuple[Union[PriceLevel, None], Union[PriceLevel, None]]:

return self.books[instrument_id][publisher_id].bbo()

def aggregated_bbo(

self,

instrument_id: int,

) -> tuple[Union[PriceLevel, None], Union[PriceLevel, None]]:

"""Calculate the aggregated BBO across all venues"""

agg_bbo: list[Union[PriceLevel, None]] = [None, None]

all_bbos = list(zip(*(book.bbo() for book in self.books[instrument_id].values())))

for idx, reducer in ((0, max), (1, min)):

all_best = [b for b in all_bbos[idx] if b]

if all_best:

best_price = reducer(b.price for b in all_best)

best = [b for b in all_best if b.price == best_price]

agg_bbo[idx] = PriceLevel(

price=best_price,

size=sum(b.size for b in best),

count=sum(b.count for b in best),

)

return tuple(agg_bbo)

def consolidated_bbo(

self,

instrument_id: int,

) -> tuple[Union[PriceLevel, None], Union[PriceLevel, None]]:

all_bids, all_offers = zip(*(book.bbo() for book in self.books[instrument_id].values()))

best_bid = max((b for b in all_bids if b), key=PriceLevel._bid_sort, default=None)

best_offer = max((o for o in all_offers if o), key=PriceLevel._ask_sort, default=None)

return best_bid, best_offer

def apply(self, msg: db.MBP1Msg) -> None:

book = self.books[msg.instrument_id][msg.publisher_id]

book.apply(msg)

if __name__ == "__main__":

equity_datasets = [

"XNAS.ITCH", # Nasdaq

"XBOS.ITCH", # Nasdaq BX

"XPSX.ITCH", # Nasdaq PSX

"XNYS.PILLAR", # NYSE

"ARCX.PILLAR", # NYSE Arca

"XASE.PILLAR", # NYSE American

"XCHI.PILLAR", # NYSE Texas

"XCIS.TRADESBBO", # NYSE National

"MEMX.MEMOIR", # Members Exchange

"EPRL.DOM", # MIAX Pearl

"IEXG.TOPS", # IEX

"BATS.PITCH", # Cboe BZX

"BATY.PITCH", # Cboe BYX

"EDGA.PITCH", # Cboe EDGA

"EDGX.PITCH", # Cboe EDGX

]

symbol = "NVDA"

start = pd.Timestamp(2025, 6, 17, 9, 30, tz="US/Eastern")

end = pd.Timestamp(2025, 6, 17, 10, 0, tz="US/Eastern")

schema = "mbp-1"

client = db.Historical(key="YOUR_API_KEY")

# Get data for all datasets

dataset_data_dict: dict[str, db.DBNStore] = {}

for dataset in equity_datasets:

dataset_name = dataset.replace(".", "-").lower()

data_path = f"{dataset_name}-{symbol}-{start.date().isoformat().replace('-', '')}.{schema}.dbn.zst"

if os.path.exists(data_path):

data = db.DBNStore.from_file(data_path)

else:

data = client.timeseries.get_range(

dataset=dataset,

start=start,

end=end,

symbols=symbol,

schema=schema,

path=data_path,

)

dataset_data_dict[dataset] = data

# Merge all datasets into one stream sorted by ts_recv

data = merge(*dataset_data_dict.values(), key=lambda x: x.ts_recv)

# Iterate over the records and calculate the consolidated BBO

cbbo_list: list[tuple[pd.Timestamp, float, float]] = []

market = MbpMarket()

for record in data:

market.apply(record)

best_bid, best_offer = market.consolidated_bbo(record.instrument_id)

cbbo_list.append((

record.pretty_ts_recv,

best_bid.price if best_bid is not None else float("Nan"),

best_offer.price if best_offer is not None else float("Nan"),

))

# Create DataFrame

df = pd.DataFrame(cbbo_list, columns=["Timestamp", "Bid", "Offer"])

df = df.set_index("Timestamp")

df["is_crossed"] = df["Bid"] >= df["Offer"]

# Now we'll plot a small slice of time when the book is crossed

start_time = pd.Timestamp(2025, 6, 17, 9, 56, 31, 650000, tz="US/Eastern")

end_time = pd.Timestamp(2025, 6, 17, 9, 56, 31, 750000, tz="US/Eastern")

df = df.loc[start_time:end_time]

fig, ax = plt.subplots(figsize=(11, 6))

# Shade periods where book is not crossed green

plt.fill_between(

df.index,

df["Bid"],

df["Offer"],

where=~df["is_crossed"],

alpha=0.2,

linewidth=0,

color="green",

step="post",

label="Normal market",

)

# Shade periods where book is crossed red

plt.fill_between(

df.index,

df["Offer"],

df["Bid"],

where=df["is_crossed"],

alpha=0.2,

linewidth=0,

color="red",

step="post",

label="Crossed market",

)

# Plot BBO lines

for col, color in [("Offer", "C1"), ("Bid", "C0")]:

plt.hlines(

y=df[col][:-1],

xmin=df.index[:-1],

xmax=df.index[1:],

colors=color,

label=col,

)

plt.gca().xaxis.set_major_formatter(mdates.DateFormatter("%H:%M:%S.%f", tz="US/Eastern"))

plt.ylabel("Price (USD)")

plt.xlabel("Timestamp (ET)")

plt.title(f"{symbol} synthetic NBBO")

plt.legend()

plt.tight_layout()

plt.show()Notice that the synthetic NBBO may occasionally appear crossed, unlike the regulatory NBBO published by the SIPs. This is expected behavior due to two factors: first, proprietary feeds include odd lot quotations, which are excluded from SIP NBBO calculations; second, the feeds originate from different data centers, resulting in receive-time deltas. These characteristics can temporarily produce crossed markets, but they also enable the construction of a more predictive microprice.

Source: DataBento

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Databento and is being posted with its permission. The views expressed in this material are solely those of the author and/or Databento and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Please keep in mind that the examples discussed in this material are purely for technical demonstration purposes, and do not constitute trading advice. Also, it is important to remember that placing trades in a paper account is recommended before any live trading.

The order types available through Interactive Brokers LLC's trading platforms are designed to help you limit your loss and/or lock in a profit. Market conditions and other factors may affect execution. In general, orders guarantee a fill or guarantee a price, but not both. In extreme market conditions, an order may either be executed at a different price than anticipated or may not be filled in the marketplace.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!