- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted August 22, 2025 at 10:00 am

If you’ve been following the luxury sector, you’ve probably seen your fair share of sobering news.

On the surface, it may look like the era of high-end handbags and bespoke suits is coming to an end. But dig a little deeper, and a different story emerges—one filled with possible opportunity for the patient, value-oriented investor.

I’ve studied markets for decades, and if there’s one thing I know, it’s that cyclical downturns have often presented the best entry points. I believe the current luxury slump is no exception. In fact, the data tells me we may be on the verge of a comeback.

Last year, global luxury sales posted their weakest performance since the 2008 financial crisis—excluding the COVID years—and 2025 isn’t off to a roaring start, either. Bain & Company projects sales will shrink by another 2% to 5% this year. That’s not what you’d expect from an industry that’s historically grown at twice the rate of global GDP.

But here’s the thing: This isn’t the first time luxury has hit a soft patch, and in the past, it’s come back stronger.

Take 2015, for example. Back then, consumers began to turn away from flashy logos, and major brands like Louis Vuitton were forced to rethink their design philosophy. The result? A pivot to more understated, timeless styles like the Capucines bag, now one of LV’s bestsellers. Sales bounced back, and those who kept the faith were rewarded.

No discussion of luxury is complete without China. Before the pandemic, Chinese travelers accounted for roughly two-thirds of their luxury spending outside of China. That changed when the pandemic hit, and many brands pivoted to local markets.

Now, with international travel picking up again, we may be on the cusp of a reversal. Chinese tourists are venturing back into Europe, where luxury goods often sell for 5% to 45% less than in China due to taxes and pricing strategies. That price gap could create an incentive to buy abroad.

To be clear, sales in mainland China are still soft. Bain estimated a 20% drop last year, and some brands like Richemont reported a 23% decline.

But we don’t think the secular tailwind of rising wealth in China has gone away. In 2024 alone, over 141,000 new millionaires were minted in China—more than 380 a day. Over time, that wealth could find its way into high-end purchases, whether from Western brands or increasingly popular domestic designers.

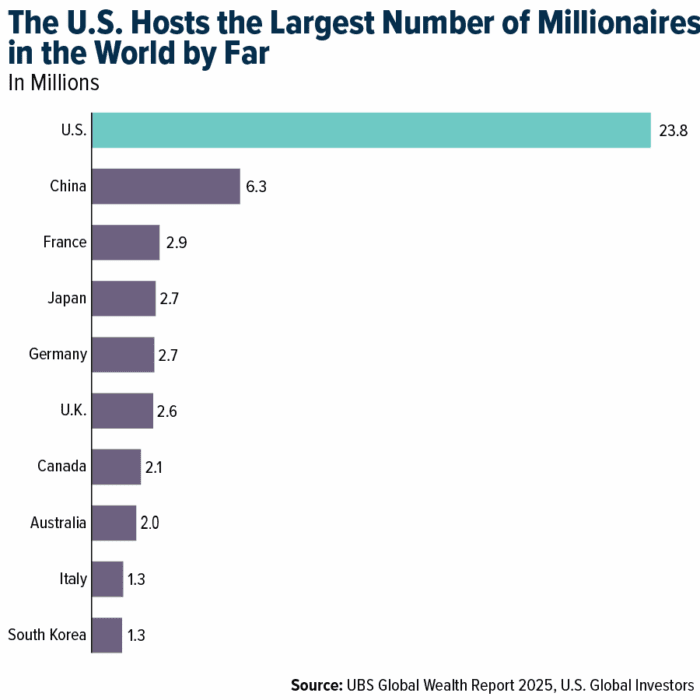

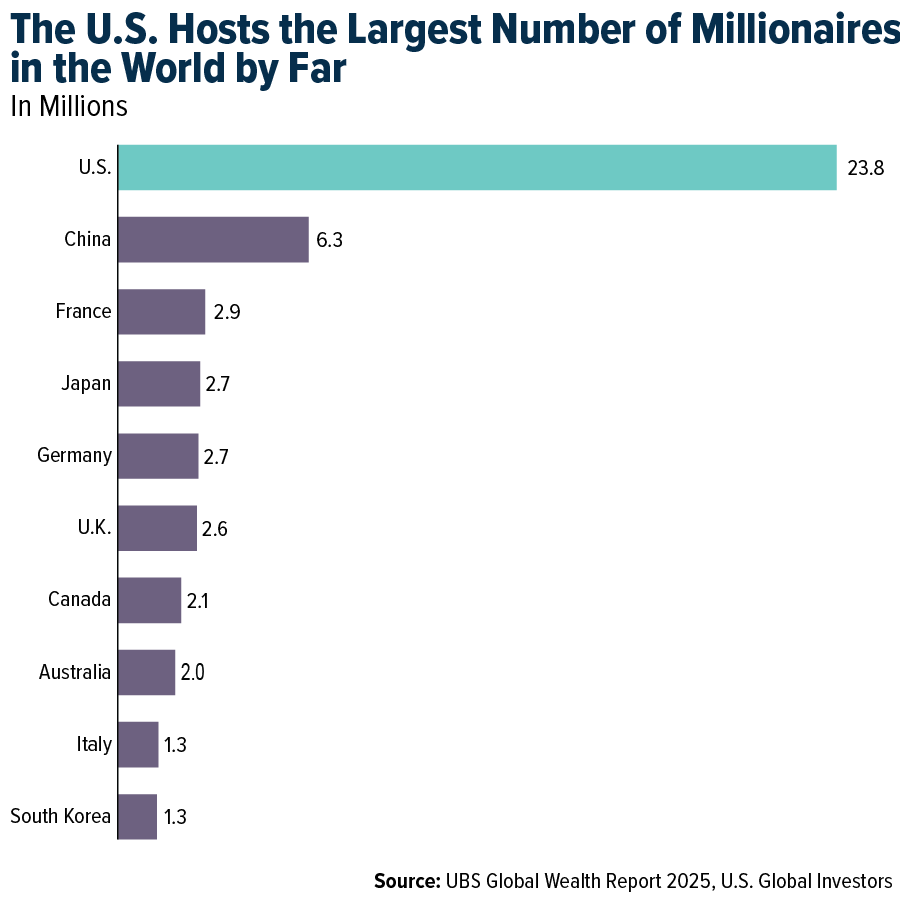

Closer to home, the U.S. continues to lead the world in absolute wealth. According to the latest UBS Global Wealth Report, the country now boasts nearly 24 million millionaires—more than the next seven countries combined. That’s nearly 40% of the world’s total.

And that number is only expected to grow. UBS forecasts that 5.3 million Americans will join the millionaire club by 2029, a nearly 9% increase. This matters because luxury demand has tended to track wealth creation more than overall GDP.

Good news, then, that financial markets are booming. The S&P 500 recently hit an all-time high, before Trump announced a new battery of tariffs. Bitcoin, often a leading indicator of risk appetite, touched $120,000. That tells me that investor confidence is healthy.

When you pair that with a tax environment that favors high earners (thanks in part to the One Big Beautiful Bill), the case for luxury demand staying strong looks compelling, at least to me.

Not all brands are hurting. Hermès reported an 8% increase in revenue for the first half of 2025. Prada’s total sales rose 9%, with its trendier Miu Miu line surging a whopping 49%. Even Richemont, which owns Cartier, saw group sales rise 6%, despite Chinese weakness.

As for the laggards, Gucci’s sales fell 26% in the first half, dragging down Kering’s overall numbers. Some, like LVMH, are using this period to buy back shares. Bernard Arnault, the group’s founder and CEO, has personally bought over $1 billion worth of LVMH stock this year.

As I often say, follow the money, especially when it’s coming from insiders.

—

Originally Posted August 11, 2025 – The Case for Luxury Stocks While They’re Still on Sale

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting www.usfunds.com. Read it carefully before investing.

Mutual fund investing involves risk. Principal loss is possible. Stock markets can be volatile and share prices can fluctuate in response to sector-related and other risks as described in the fund prospectus. Foreign and emerging market investing involves special risks such as currency fluctuation and less public disclosure, as well as economic and political risk. Companies in the consumer discretionary sector are subject to risks associated with fluctuations in the performance of domestic and international economies, interest rate changes, increased competition and consumer confidence.

Fund portfolios are actively managed, and holdings may change daily.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

All opinions expressed and data provided are subject to change without notice. Holdings may change daily.

Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

About U.S. Global Investors, Inc. – U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by clicking here or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Foreside Fund Services, LLC, Distributor. U.S. Global Investors is the investment adviser.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from US Global Investors and is being posted with its permission. The views expressed in this material are solely those of the author and/or US Global Investors and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!