- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted August 11, 2025 at 11:47 am

The article “Simplicity May Lead to Too Much Risk Taking” was originally published on Alpha Architect blog.

We often assume that simplifying investment products helps reduce risk. But this paper challenges that intuition. Puri shows that simpler structures—like low-dimensional lotteries or intuitive cash flows—can actually encourage investors to take on more risk. Why? Because people misunderstand the risk in simple designs and overestimate their returns. Using detailed experiments with lottery-like payoffs and real investment choices, the paper finds that perceived simplicity can distort demand and lead to inefficient pricing. For advisors, the message is clear: simplifying products might not reduce client risk—it could increase it if not paired with proper education and expectations management.

Simplicity Can Be Misleading

Investors often interpret simpler assets as safer, even when the underlying risk is unchanged. This can lead to a mismatch between perceived and actual risk.

Demand Increases with Simplicity

Experimental results show that when complex financial products are simplified in presentation (e.g., using visual aids or fewer outcomes), investor demand increases—even for high-risk assets.

Overvaluation of Risky Simplicity

Investors are willing to pay more for risky assets when those risks are framed simply. This leads to price distortions in markets and potentially inefficient allocations of capital.

Behavioral Biases Drive This Effect

The paper links these findings to behavioral tendencies like overconfidence and narrow framing. Simplicity reduces cognitive load but masks the true risk-reward profile.

Don’t Confuse Simplicity with Safety

A well-designed ETF or structured product may appear “cleaner” to a client but still carry substantial risk. Advisors must carefully walk clients through the real risk exposures.

Use Simplicity Strategically—Not Superficially

Simplifying the presentation of portfolios or models is helpful, but it must come with clear risk disclosure. Otherwise, clients may assume the strategy is less volatile than it actually is.

Watch for Mispriced Risk in Client Behavior

If clients gravitate toward a specific investment because “it looks straightforward,” take a closer look. They may be unintentionally overexposing themselves to tail risk or complexity hiding under a simple façade. This behavior is similar to another blog, which discusses how trust in a financial advisor can lead investors to take on more risk than intended.

“Sometimes, simple-looking investments can actually be more risky than they seem. Just because something is easy to understand doesn’t mean it’s safer. Our job is to help you see the full picture, so we’re not just choosing the simplest path—we’re choosing the smartest one.”

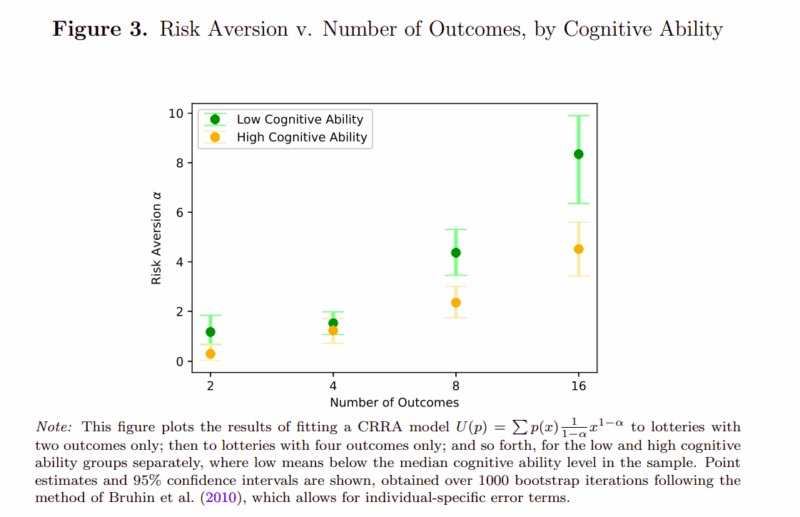

Figure 3 splits participants in the risk aversion module by cognitive ability – above or below median, respectively – and plots risk aversion by number of outcomes. The result at two outcomes replicates that of the above literature, e.g. low cognitive ability individuals have higher measured ‘risk aversion.’ However, as complexity increases to eight and sixteen outcomes, the discrepancy in CRRA-measured risk aversion further diverges, indicating that complexity aversion and measured cognitive ability are weakly negatively correlated.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

I introduce and test for preference for simplicity in choice under risk. I characterize the theory axiomatically, and derive its properties and unique predictions relative to canonical models. By designing and running theoretically motivated experiments, I document that people value simplicity in ways not fully captured by existing models that study risk premia in financial markets. Participants’ risk premia increase as complexity increases, holding moments fixed; their dominance violations increase in complexity; their behavior is predicted by simplicity’s characterizing axiom; and their complexity aversion is heterogeneous in cognitive ability. None of expected utility theory, cumulative prospect theory, prospect theory, rational inattention, sparsity, salience, or probability weighting that differs by number of outcomes fully capture the experimental findings. I generalize the underlying theory to additionally capture broader measures of complexity, including obfuscation, computation, and language effects.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

This site provides NO information on our value ETFs or our momentum ETFs. Please refer to this site.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Alpha Architect and is being posted with its permission. The views expressed in this material are solely those of the author and/or Alpha Architect and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

This abstract is the most obtuse summary I have read to date on the subject of simplicity. Less is more.