- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted June 25, 2025 at 9:30 am

President Donald Trump’s announcement last Wednesday of a new trade agreement with China is the kind of headline that gives markets a sense of relief. As I overheard at Wealth Management’s EDGE conference, which I attended in Boca Raton, Florida, we may have dodged a recession.

Beyond that, I think Trump’s announcement provides investors with a fresh incentive to turn their attention to global trade, particularly the shipping industry.

According to the president’s statement on Truth Social, the deal is “done,” pending final approval from both him and President Xi Jinping. The terms include a commitment from China to supply rare earth metals, while the U.S. maintains significantly higher tariffs on Chinese imports—reportedly 55% compared to China’s 10%.

I think most people would agree that, after months of tariff turmoil, this is a constructive step toward stability and, indeed, fairness. For shipping, that matters more than you might think.

As everyone recalls, the White House imposed an eye-popping 145% tariff on Chinese imports in April, sending shockwaves through global supply chains and capital markets. Retailers hit the brakes. Orders were delayed or canceled, and ocean freight volumes plunged.

But just a few weeks later, the administration announced a 90-day pause and slashed tariffs to 30%. “Reciprocal” tariffs with other trading partners were also temporarily frozen.

During that window, we’ve seen a surge of renewed shipping activity.

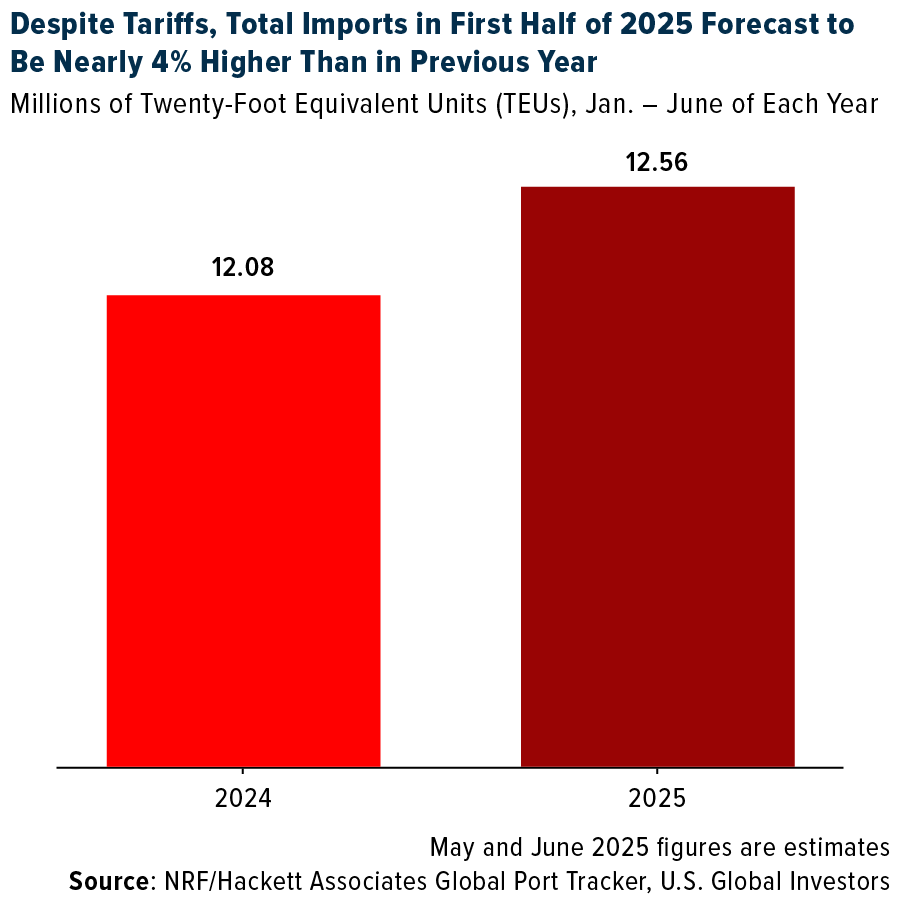

The National Retail Federation (NRF) reported last week that container imports at U.S. ports are now expected to climb 3.7% year-over-year for the first half of 2025. That’s better than forecasts before the pause. Shipping volume from China jumped 9% in the first week of June alone, according to Goldman Sachs data.

The container shipping industry has always been cyclical and sensitive to geopolitical events, and this year has been no exception. After bottoming in 2023, rates have rebounded sharply, driven not only by tariff uncertainty but also by persistent global disruptions, such as the Red Sea crisis.

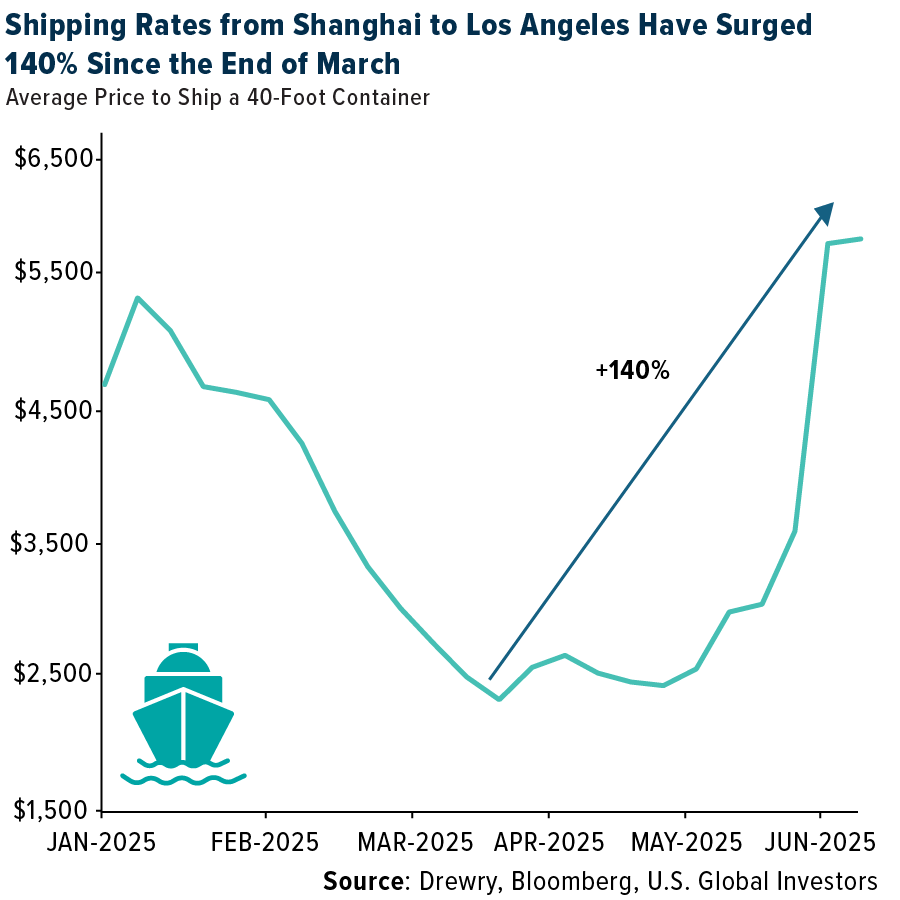

Drewry’s World Container Index showed a 70% spike in just four weeks, with freight costs from Shanghai to Los Angeles up nearly 140% since the end of March. That said, prices remain well below the COVID-era highs, when rates surpassed $10,000 per 40-foot container.

For context, today’s rates are closer to $5,800—a historically elevated level, but not unsustainable. Importers are moving fast to restock while the policy window is open. That activity is supporting not only shipping volumes but also company earnings.

In the first quarter of 2025, the global container shipping industry posted nearly $10 billion in profit. That’s a drop from the $15.6 billion earned in Q4 of last year, but it’s also 83% higher than the same period in 2024.

The market has begun to take notice. As of this month, I count nine publicly traded container carriers with a market capitalization of at least $10 billion. This includes names like Maersk and Hapag-Lloyd, along with rapidly growing Asian players such as Wan Hai Lines. These companies now rival or surpass familiar, investable U.S. airline stocks in terms of valuation.

This tells me that institutional investors see the potential in global shipping.

Granted, it’s not all smooth sailing. A recent survey by Freightos of more than 100 small-to-midsize importers paints a picture of anxiety beneath the surface. Even with the pause in place, 80% of respondents said they’re as or more worried than they were in April. Nearly half gave the situation a “perfect 10” on the disruption scale. Full disclosure, this survey was taken before the U.S.-China trade deal was announced.

Reshoring—or the practice of shifting production back to the U.S.—remains a possibility for companies that have moved overseas, but only 6% of companies have done so, according to Freightos.

You may have seen headlines that the World Bank revised its global growth forecast downward to 2.3% for 2025, marking the slowest non-recessionary year since 2008. Trade frictions, including those stemming from tariff uncertainty, are among the top culprits.

But there’s more to the story. The same World Bank report echoed Trump’s longstanding complaint that the U.S. faces unfairly high trade barriers abroad. The Washington, D.C.-based organization calls for a broad reduction in global tariffs, suggesting growing recognition of the problem and, perhaps, momentum for reform.

If that happens, and the world moves toward more equitable trade terms, shipping could be a key beneficiary. More open markets mean more trade, and more trade means more cargo.

Shipping companies are coming off a strong earnings season. Rates are elevated but not extreme. Inventories are being replenished. And long-term, the world will still need ships to move the goods that power our economies.

Interested in learning more about investment opportunities in global shipping? Email us at info@usfunds.com with the subject line SHIPPING.

—

Originally Posted June 16, 2025 – Tariff War Truce Triggers Shipping Surge

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (03/31/2025): COSCO SHIPPING Holdings Co. Ltd., AP Moller – Maersk A/S, Evergreen Marine Corp., HMM Co. Ltd., Nippon Yusen KK, Wan Hai Lines Ltd., Delta Air Lines Inc., United Airlines Holdings Inc., Southwest Airlines Co., American Airlines Group Inc.

The Drewry World Container Index (WCI) is a composite index that tracks the average cost of shipping a 40-foot container (FEU) on eight major international trade routes.

All opinions expressed and data provided are subject to change without notice. Holdings may change daily.

Some of these opinions may not be appropriate to every investor. By clicking the link(s) above, you will be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

About U.S. Global Investors, Inc. – U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product.

Certain materials in this commentary may contain dated information. The information provided was current at the time of publication.

Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content.

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by clicking here or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Foreside Fund Services, LLC, Distributor. U.S. Global Investors is the investment adviser.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from US Global Investors and is being posted with its permission. The views expressed in this material are solely those of the author and/or US Global Investors and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!