- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted March 11, 2025 at 12:55 pm

One question I get all too often at times like these is something like, “I bought VIX calls, and they didn’t do what I expected.” Options traders all too often forget that options are priced off the forward value of the underlying security at the desired expiration. That can differ substantially from the spot value. The concept of forward value is crucially important. Here is what to keep in mind.

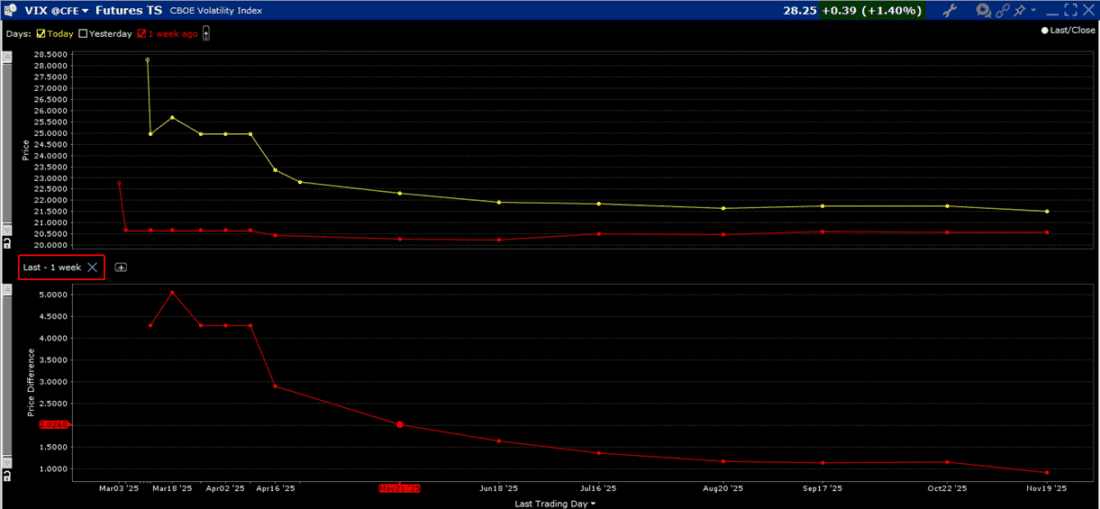

Put very simply, when one is trading VIX options, the price is based off the futures that expire in the same month or week as the options. As we can see from the real-world examples below, those values can either be quite similar to each other or differ substantially.

Source: Interactive Brokers

Just one week ago, spot VIX was relatively elevated, but the VIX futures curve was pancake flat beyond that. At that time, the “at-money” value of virtually every VIX option was about 20.5. This was despite the fact that spot VIX, the number that is most frequently quoted, was 23. Those who bought calls might have thought they were getting a bargain, and conversely, those who bought puts might have thought that prices seemed unreasonably high. A thorough understanding of forward values becomes key to understanding that distinction.

The most basic consideration about forward value occurs when one is trading options on dividend-paying stocks. Dividends reduce the forward value of a stock – if you own options rather than shares on an ex-dividend date you forego the stock’s dividend. Experienced options traders know to be quite cognizant of dividend dates, and typically exercise deep in-the-money calls to avoid that pitfall. Thus, whether those traders are explicitly considering forward values, they tend to think in those terms.

For years, when rates were near-zero, those who traded non-dividend paying stocks could lose sight of the fact that forward values were important because forward values could be nearly identical to spot prices. When rates began to rise, we wrote a piece reminded readers about the role of interest rates in options pricing, with the unenticing title, “Rho – The Forgotten But Important Options Greek.” Even now, the role of interest rates on forward values can be relatively subtle, especially with traders’ increasing focus on short-term options, but they become quite obvious when a stock is hard-to-borrow. In those cases, the forward value can be substantially below the spot price, reflecting the negative interest rates that prevail for hard-to-borrow stocks.

By the way, here is an important shortcut to determining a forward value. Look at the calls and puts of a given option’s expiration. If the price of the call is equivalent to the put, then that is roughly the forward value of the underlying product at that expiration. Sometimes they don’t line up perfectly, so then find the lines where the call price flips from above the corresponding put price to below it. That means that the forward value is between the two strikes.

These concepts apply to options on index products. For example, when we think about futures on the S&P 500 (SPX) we note that those typically trade at a premium – at least with interest rates at current values. This is because the interest rate is greater than the index’ dividend yield. Thus, we currently see June ES futures trading about $50 above the soon-to-expire March futures. The logic is that one can buy the futures on margin instead of paying cash for the index and invest the difference in T-bills, with the interest gained by the favorable margin treatment outweighing the foregone dividends of the component stocks over that period.

Yet there is a very important distinction when trading VIX options. Unlike SPX, where there is a stable relationship between interest rates and dividends that leads to a consistent “contango”, or upward sloping futures curve, VIX has a tendency to flatten or slip into “backwardation” during times of market stress. I explained backwardation this way:

It implies an abnormal state, and a commodity that is experiencing shortages tends to be in backwardation. If demand outstrips supply in the short term, but is expected to normalize at some point in the ensuing months, we tend to see a curve in backwardation.

In the case of VIX futures, the commodity in short supply is volatility protection. Its supply and demand can vary wildly when markets are unstable. This is something that is reflected in the chart above. We see the shape of the curves change dramatically in just a week. Confusingly for some, that depending upon which expirations were used, it also means that the returns on calls differed substantially over that period.

Note the differences in the bottom half of the chart. Outside of spot prices, the biggest spike was seen futures expiring March 18th. Those rose by about $4.75. Thus, one would have expected a 50-delta option with the same expiration to rise by about $2.32 (if implied volatilities remained constant – a difficult “if”). Yet if one bought a call expiring in May, where the futures rose by about $2.12, that same delta call would have appreciated by about $1.06. That’s a nice return, but far less than that reaped by the buyer of the shorter-term option. (Of course, if one had bought puts, the longer-term options would have suffered smaller losses.)

That is how I explained the situation to those who raised the question about seemingly subpar VIX option performances. Hopefully that made sense of a somewhat unintuitive concept.

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Related Articles

Hey Steve, another option question: Over the last couple of weeks the daily put/call ratio on the QQQ has generally been below the 1.0 level. Has this been typical in market sell-offs during prior years?

Another important thing to remember about VIX is that the index and front mo futures contract do not trade the same. Aug 5, vix index was in the 60s, front mo futures vix barely cracked 30s or 40s I forget now.

The other issue that makes VIX options tricky is the fact that VIX is mean-reverting. So if the market falls and then stays down well before your option expires, VIX will likely be lower again by the time of expiry, and it’s European-style, so you will not get the boost from a VIX call option as you would get from just a put option on the index level itself. Unless panic remains and VIX stays remains higher.