- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted December 10, 2024 at 12:09 pm

The article “Frog in the Pan Momentum: International Evidence” first appeared on Alpha Architect blog.

This article analyzes various reasons why momentum strategies might work outside US borders. While the US story is firmly rooted in behavioral biases, is the same true on an international scale? That seems logical and likely. In fact, the authors conclude that a “slow diffusion of news best explains momentum in the international context…across all of our tests, we find supportive evidence for the FIP (“frog in the pan”) proxy in both emerging and non-US developed markets.” The results indicate that underreaction to continuous news plays a key role in generating momentum internationally. I suppose that means that when investors underreact to steady news, it’s very like ignoring the frog in the pan – momentum begins to boil before any of the frogs notice.

The market efficiency debate is central to the field of finance, and the ability of the field to explain investor behavior. The debate, however, continues to this day and momentum has been a sticky thorn in the side of those promoting rational and efficient markets. In particular, momentum flies in the face of the most conservative level of market efficiency: the weak-form notion of market efficiency. Weak-form efficiency holds that a stock’s relative performance is unrelated to its past performance at any time horizon. Strategies like momentum investing should not produce excess profits, nor should they be outside the ability of generally accepted risk models to account for results. So there you have it: Behavioral biases in global markets. Just another nail in the coffin of market efficiency.

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

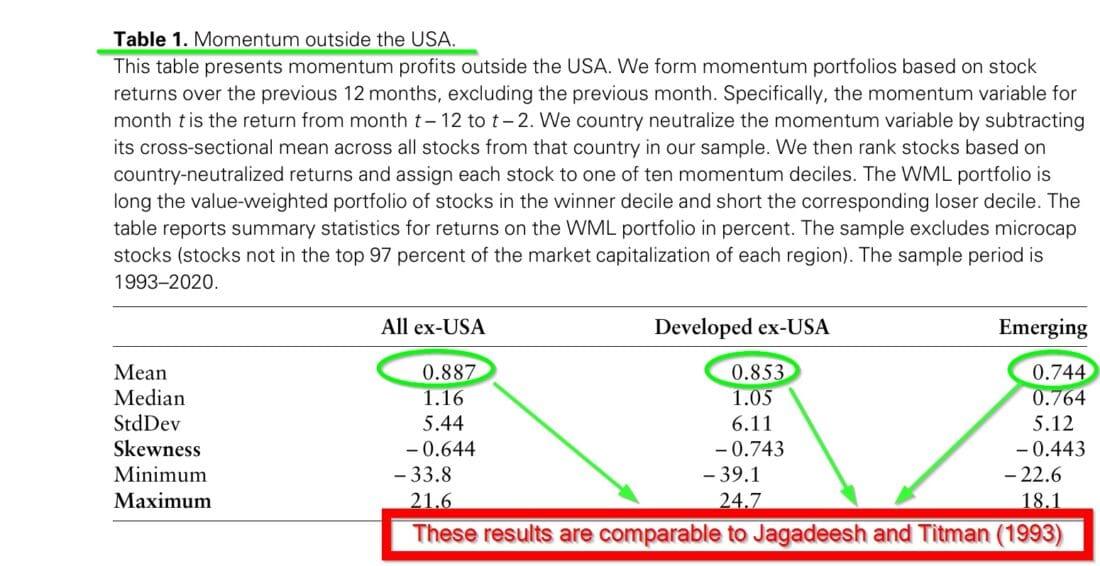

Although momentum exists in many markets throughout the world, explanations for momentum have largely been tested using US data. We investigate the extent to which US-based momentum explanations extend to the international context, using regression-based and portfolio approaches. Among the several hypotheses we consider, we find reliable support for the hypothesis that due to limited attention, investors underreact to information arriving in small bits rather than in large chunks, which results in momentum. We also find secondary support for the overconfidence hypothesis for momentum. Finally, we find that momentum is stronger in up-markets and less-volatile markets in the international context just as in the USA. This finding also accords with the investor overconfidence hypothesis, under the proviso that investors are more confident in rising, low-volatility markets.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

This site provides NO information on our value ETFs or our momentum ETFs. Please refer to this site.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Alpha Architect and is being posted with its permission. The views expressed in this material are solely those of the author and/or Alpha Architect and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!