- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted April 30, 2024 at 11:15 am

Markets are buckling ahead of the Powell press conference tomorrow, as this morning’s data justifies an increasingly hawkish committee. Today’s stateside economic data on employment costs and consumer confidence point to lingering inflationary pressures, while Europe has avoided recession with an upside beat on first quarter GDP. The European Union, however, is facing a similar problem as other regions: activity rebounding alongside price pressures, further disrupting the journey towards a soft landing amidst 2% inflation.

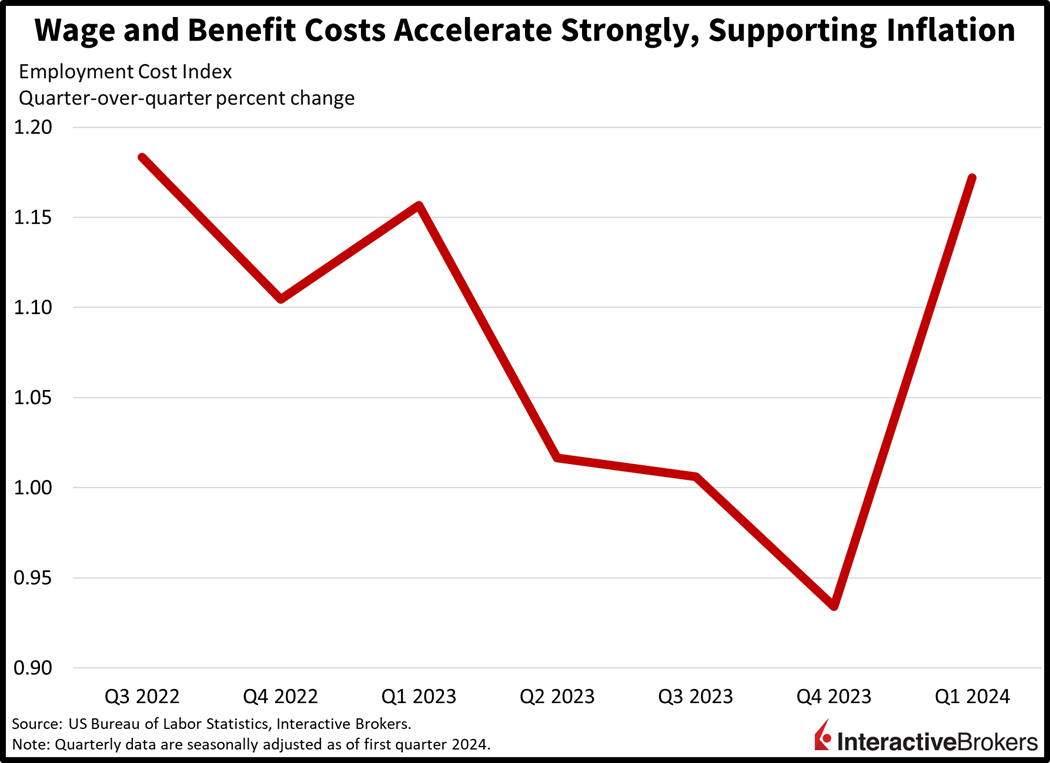

Inflation’s persistence is continuing to be supported by a powerful tailwind of rising labor expenses with workers getting fatter paychecks and increasingly pricey benefits, according to the Employment Cost Index report released today. Quarter after quarter, annualized wage growth exceeding 4% has consistently lifted the costs of services, posing significant hurdles to the Federal Reserve’s 2% inflation target. The index, or ECI, considers private company wages but also takes benefit expenses and government workers into account, unlike average hourly earnings that are published in the monthly jobs report. In the first three months of this year, it rose 1.2% quarter over quarter (q/q) and 4.2% year over year (y/y), an acceleration from the fourth quarter’s 0.9% q/q while maintaining the same y/y rate. Increases in benefit expenditures led the push, speeding up from 0.7% to 1.1% q/q, while salary growth kept its momentum of 1.1% q/q.

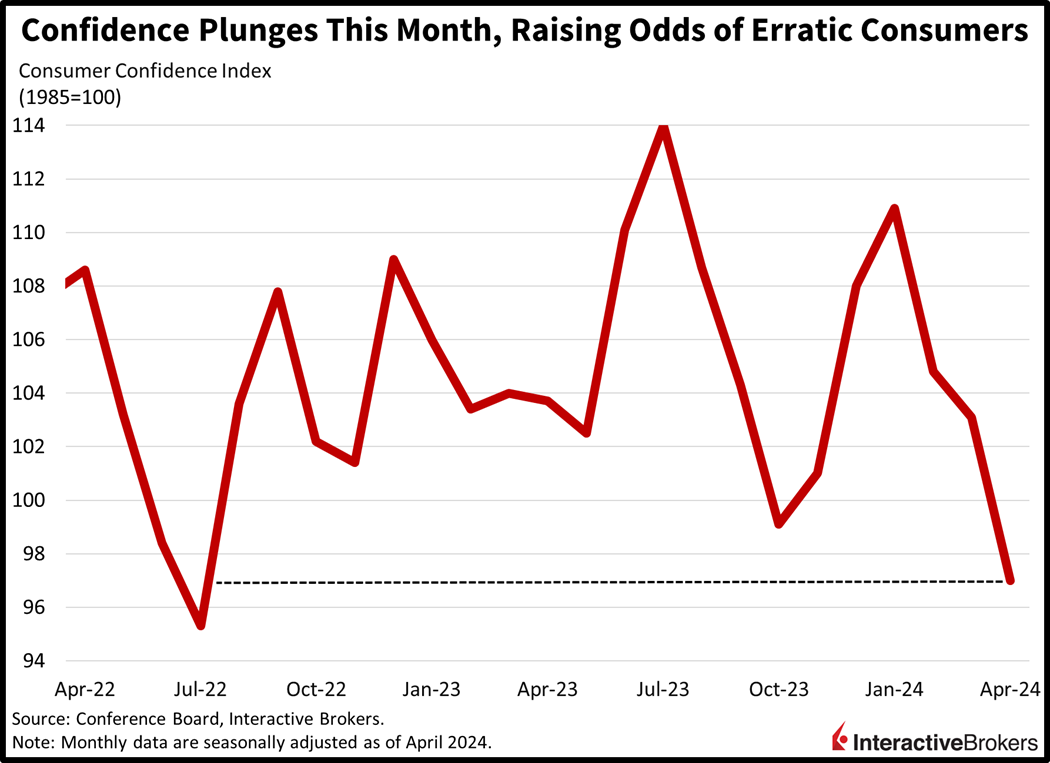

Heavier paychecks failed to widen smiles for American consumers, however, as rising charges for food and gasoline dented the spending power of wallets and pocketbooks alike. The Conference Board’s Consumer Confidence Index plunged to 97 this month from 103.1 last month while missing projections of 104 by a mile and then some. Driving the big miss, which was the lowest reading since July 2022, were deteriorating future prospects, with the Expectations sub-index cratering from 74 to 66.4 month over month (m/m). The Present Situation sub-index slipped from 146.8 to 142.9, meanwhile. Folks were incrementally less optimistic about the current job picture while increasingly pessimistic about future conditions related to income possibilities, job vacancies and labor opportunities. Plans for big-ticket purchases like homes and durable goods declined, while vacation bookings also retreated to their lowest level since last summer. Households were also concerned about geopolitical conflicts and the upcoming US presidential election.

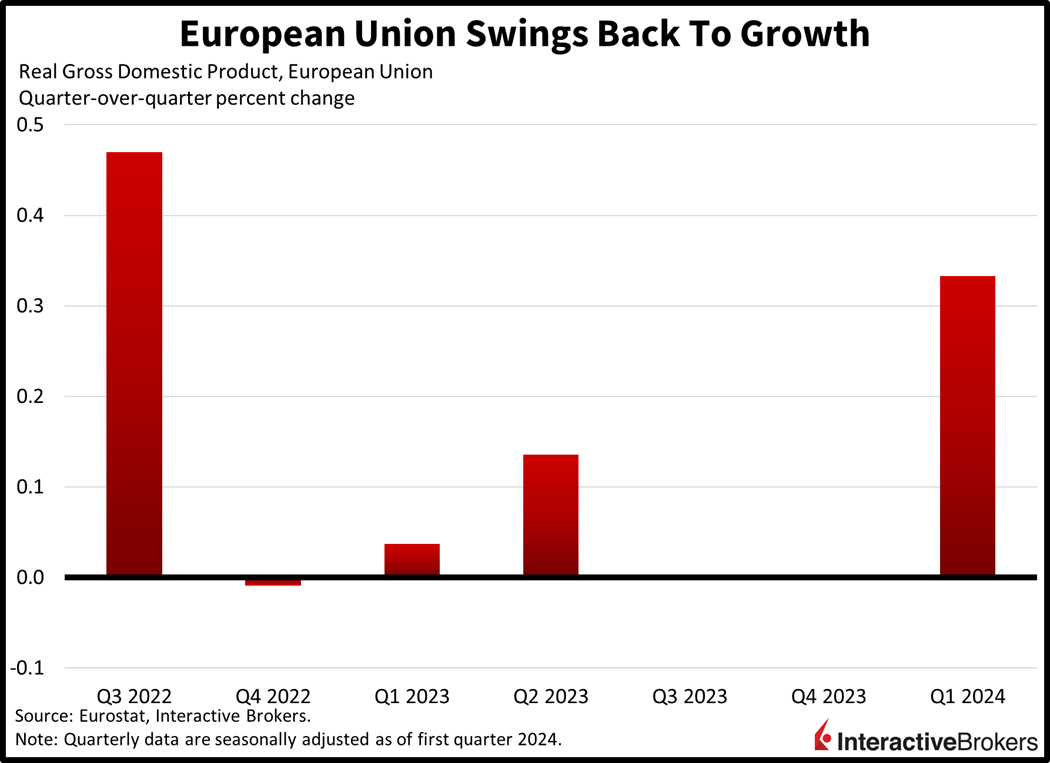

Across the Atlantic, the European Union shifted back to growth this year but not without persistent inflation. Gross domestic product increased 0.3% q/q, amidst broad-based activity strengthening across the region, beating estimates and climbing from the fourth-quarter’s doughnut (0%). The recovery has been driven by improving confidence across businesses and consumers as the continent looks forward to the beginning of the European Central Bank’s easing cycle possibly this summer.

Growth was met with fierce price pressures though, as this morning’s inflation data for April, released in a separate report, depicted continued cost burdens. Inflation rose 0.6% m/m and 2.4% y/y, in-line with estimates and near March’s figures of 0.8% and 2.4%. Charges rose across the board as follows:

Consumer spending in the first quarter varied among firms reporting earnings this morning. PayPal noted resilient spending while Coca-Cola, 3M and McDonald’s experienced weakening sales to differing degrees.

Stocks, bonds and the dollar are all frontrunning the possibility of a frowning Powell at tomorrow’s interest rate decision. All major equity indices are much lower with the Russell 2000, Dow Jones Industrial, Nasdaq Composite and S&P 500 down 1.2%, 0.8%, 0.7% and 0.6%. Sectoral breadth is negative with all segments lower, led by consumer discretionary, energy and materials; they’re losing 1.5%, 1.4% and 1.3%. Treasuries are being unloaded, with the 2- and 10-year maturities trading at 5.01% and 4.66%, 3 and 4 basis points (bps) heavier on the session. The greenback is gaining on loftier inflation expectations, rising rates and an outlook for the Fed to remain tight relative to other central banks. The Dollar Index is up 41 bps to 106.07 as the US currency gains versus all of its major counterparts, including the euro, pound sterling, franc, yen, yuan and Aussie and Canadian dollars. Crude oil is retreating as traders see light at the end of the tunnel in the Middle East amidst US Secretary of State Anthony Blinken pushing for a peace deal. WTI crude is down 0.6%, or $0.46, to $82.19 per barrel. Gold and copper are also seeing selling pressure, with prices down 2.1% and 1.7%.

As we all wonder about the specifics of policymakers’ discussions during the first day of the Fed’s two-day meeting today, the importance of tomorrow’s press conference following Powell’s presentation is escalating for market participants. From the beginning of the year to today, rate expectations have shifted significantly; we’re down from seven estimated cuts to only one for 2024, as economic and inflation data has surprised to the upside all year on an aggregate basis. Another important consideration will be plans for tapered quantitative tightening (QT), or the process of the Fed allowing Treasuries and mortgage-backed securities to roll off their balance sheet without replacing them at a more subdued pace. Powell is especially attentive to these liquidity risks, as he probably perceives himself as too draconian when rates spiked in 2019 as a result of scarce bank reserves. Presently, however, there may be room for a positive surprise, with yields and stocks effectively setting up for a hawkish Powell. An upside case may flourish if the chair constantly reminds us that despite his firmness, the committee has the tools to loosen financial conditions acutely if the labor market turns.

Visit Traders’ Academy to Learn More About Consumer Confidence and Other Economic Indicators

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Related Articles

OPY seems like the best quarter on all investment bank still 62% of real book cheap