- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Latest Webinars

Posted March 8, 2024 at 11:15 am

This morning’s nonfarm payroll report depicted robust hiring in February while also showing an increase in unemployment, moderating wage growth and anemic labor force participation. Bulls were focusing on the weaker aspects of the report by buying up speculative assets, stocks and bonds, but bears are mightily trying to pull an intraday interception, as stocks have reversed from green to red. This morning’s weaker figures, which are supportive of a lighter Federal Reserve, also align with the riskiest juncture of monetary policy tightening—the potential for the labor market to deteriorate markedly before the central bank provides accommodation.

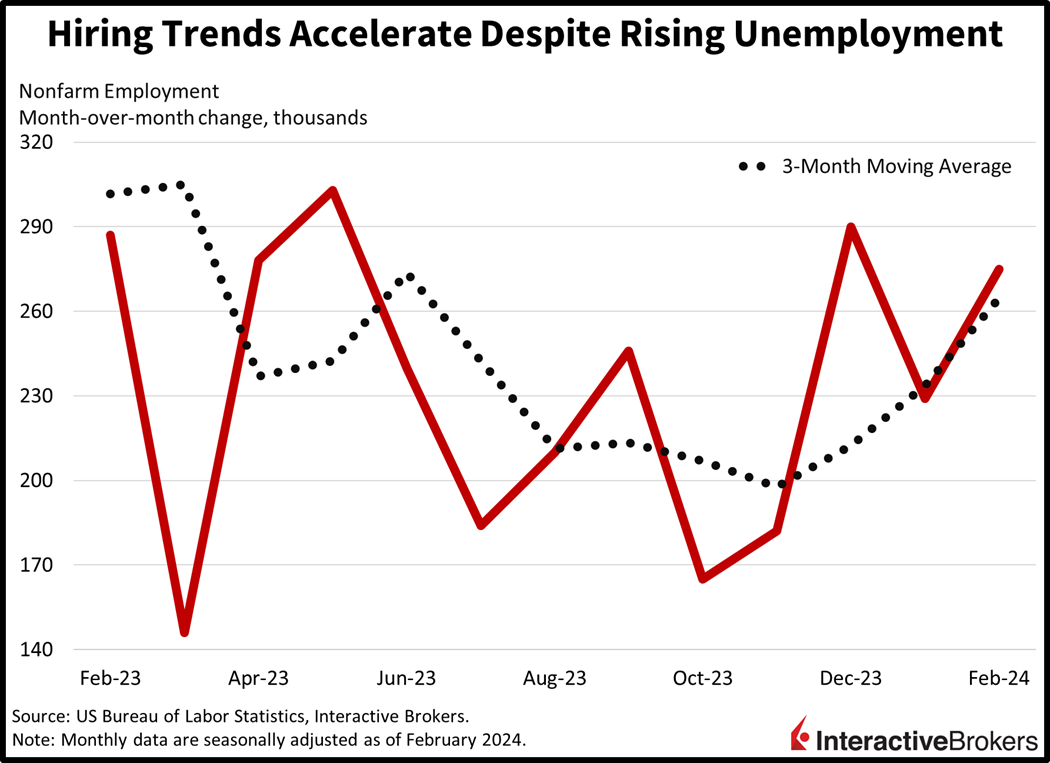

The US economy added 275,000 workers last month, exceeding estimates of 200,000 and January’s downwardly revised 229,000. The report offered a non-cyclical tilt, with education, health services and government adding 137,000 jobs, roughly half of the headcount additions. Among the cyclical sectors, the leisure and hospitality category, the trade, transportation and utilities group and the construction sector performed best, adding 58,000, 40,000 and 23,000 employees. All other gainers added below 10,000 jobs while manufacturing lost 4,000 and mining was unchanged. Employment in the temporary help services category, an indicator of labor demand, dropped to its lowest level since 2020.

While headline growth was impressive, the report depicted softening in certain areas. The unemployment rate climbed to 3.9%, the loftiest level since January 2022, while average hourly earnings grew at the slowest rate since February 2022. Average hourly earnings grew 0.1% month-over-month (m/m) and 4.3% year-over-year (y/y), much lighter than forecasts expecting 0.3% and 4.4% as well as January’s 0.5% and 4.4%. Additionally, the labor force participation rate remained at 62.5%, down from November’s 62.8%.

Recent earnings releases provide a favorable glimpse of inflation for retailers, the tailwind of artificial intelligence (AI) for tech companies and in at least one example, businesses increasing their spending to improve efficiency. The following highlights illustrate those trends:

Markets were celebrating this morning’s report with market players pointing to the rising unemployment rate as a justification for rate cuts in the near future. All major US equity indices were higher but have now reversed most of those gains by tumbling into the red. The small-cap, rate-sensitive Russell 2000 Index is leading with a gain of 0.3%, meanwhile. The S&P 500 and Nasdaq Composite indices both reached fresh all-time highs earlier in the session, but are now down 0.2% and 0.5%. The Dow Jones Industrial Average is hanging in there and is still positive by 0.2%. Sectoral breadth is positive with 8 out of 11 sectors higher being led by communication services, industrials and financials, which are up 1.2%, 0.3% and 0.3%. The laggards consist of the consumer staples and technology segments, which are lower by 0.8% and 0.7%. The exuberance was extending to cryptocurrencies, with bitcoin reaching a fresh all-time high north of $70,000, but it’s now trading below $68,000. Short-end rates are plunging on lighter monetary policy expectations while the long-end is relatively unchanged. The 2- and 10-year Treasury maturities are trading at 4.46% and 4.08%, 5 and 1 basis point (bps) lower on the session. Projections of a friendlier Fed amidst a hawkish Bank of Japan are weighing on the dollar, with its index down 23 bps to 102.56. The yen is gaining a sharp 0.7% against the US currency, while the greenback is losing ground to all of its other developed market peers, including the euro, pound sterling, franc, yuan and Aussie and Canadian dollars. Crude oil is down in response to softening demand expectations resulting from the risks of rising joblessness and buoyant supplies stateside. WTI crude is down 1.3%, or $1.03, to $78.36 per barrel.

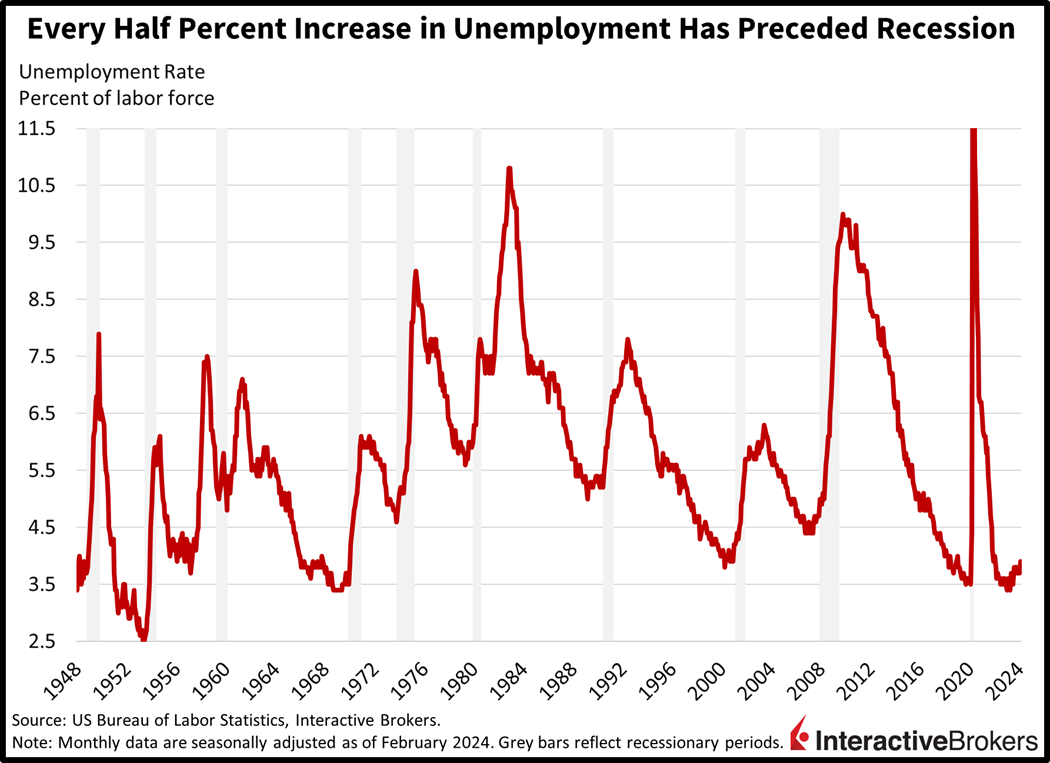

Market players are increasingly anticipating that June will bring the Federal Reserve’s first rate cut, incrementally shortening our risky journey across the monetary policy bridge. In the meantime, however, sharp rises in the unemployment rate often precede economic slowdowns. Historically speaking, when the unemployment rate has increased 50 basis points, it has been followed by recession. The unemployment rate in April 2023 was 3.4% while today’s report places it at 3.9%, 50 bps higher than this cycle’s trough. As we arrive at the riskiest part of the economic cycle, we’re seeing labor conditions and consumption patterns deteriorate, but can they hang in there long enough as the long and variable lags of monetary policy tightening work their way through the economy? Next week’s Consumer Price Index and Retail Sales reports will offer important clues on the direction of inflation and consumer spending, and their roles in what could possibly mark a turning point in the economic cycle.

Visit Traders’ Academy to Learn More About Payroll Employment and Other Economic Indicators

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics, an affiliate of Interactive Brokers LLC, and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

I find this report very useful to understand

the present economics.