- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Lesson 8 of 11

New to Interactive Brokers?

In this lesson, we will cover information about placing complex orders.

Before we begin, we will need to add some new imports compared to our usual two. First, be sure to include “from ibapi.tag_value import TagValue”. Then, be sure to add “from ibapi.contract import ComboLeg”.

Let’s begin by placing some more complex orders. Let’s start by making a Stock Combo, though this same process could be used for Futures or Options Spreads, with different contract details. In this case, I want to simultaneous buy TSLA and sell AAPL as a stock combo.

While moving through this lesson, please keep an open mind as to what Buy/Sell and Long/Short mean with respect to combos.

For example, when I enter a short position I need to sell a stock when I have a position of 0.

To further explain this, let’s start with a brief example. Let’s assume I want to be Long for the total trade. Right now, TSLA currently has a higher share price than AAPL, so I will use that as my base value.

So, if I want to be long for the whole combo, I can enter the trade by either:

OR

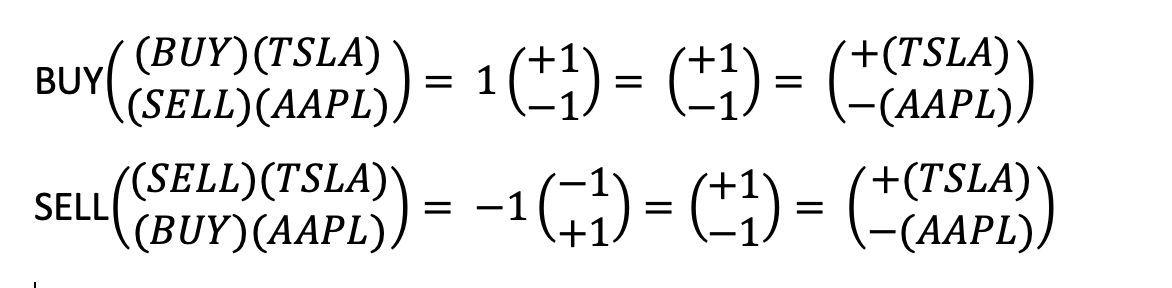

This structure is just like a vector-scalar multiplication:

You can think of buy as a positive one and sell as a negative one.

So, in this matrix you can see that I am trying to buy the whole of the share, and therefore, TSLA as a buy order times the whole of the buy order for the combo will net me a positive TSLA position. Similarly, if I buy the SELL of an AAPL position, I will wholly be negative on that.

We can invert this, and I can then do a sell order for the full combo. If I am selling the TSLA order and selling the whole of the combo, in reality, that is a negative one times a negative one, which brings me to a positive one, or a buy in this example.

Similarly, a negative one, or a sell for the combo times a positive one, or a buy for the AAPL shares, will then give me an overall position of negative or shorting the APPL stock.

Combo Order

To start, let’s take a look at our contract. We will be introducing a new concept here. As usual, I will have my contract object, mycontract. For the example, I will include both of my underlyings. In the stock combo example, I will be using AAPL,TSLA; however, for a future or option spread, you will just use your one underlying value, such as ES or SPX respectively. Now, for the secType, I will use BAG. This indicates that I am using a combo order to the system. Exchange and Currency will remain the same as usual.

Now I can begin to add legs to my order. I will create my first leg. To do so, I will create leg1 and set it equal to ComboLeg().

Then I will add my leg’s contract ID, in this case I will use TSLA, 76792991. I will be using a ratio of 1; however, you are welcome to change this value to a higher number as needed. I’ll add my leg’s action, or BUY per my ratio before, and then set my leg’s exchange as SMART.

Then, I can edit my second leg, which I will call leg2. Just like before, I will add AAPL’s conid, another ratio of 1, and exchange of SMART. However, this time I will set my action to SELL.

Now that we have our legs, we can attach them to our contract object. To do this, I will type “mycontract.comboLegs = []”.

Then I can append each leg to my list, “mycontract.comboLegs.append(leg1)”, “mycontract.comboLegs.append(leg2)”.

Keep in mind, I am only doing a 2-leg stock combo. Just like in TWS, I could have up to six legs on a guaranteed spread.

This is everything we need for our contract. Let’s get started with our order object. We have our usual options of a Market or Limit Order; but there are alternative order types such as REL+MKT that we would recommend investigating further in our documentation’s Order section. In this case, I will use a LMT order.

As I mentioned before, TSLA is at about $225 and AAPL is about $150. If we do the math, we know our order would put us at a current price of about $75. I will set my limit price to $80.

Our other order attributes will be the same, except in my case I will be adding myorder.smartComboRoutingParams as an empty list. These are for unique values for combo orders. In particular, because I am using a Non-guaranteed order, I will need to approve this for the system. To do so, I will append to that list, “TagValue(‘NonGuaranteed’, ‘1’)” to approve the use of non-guaranteed orders.

With that set, I can now submit my order. If we look at the order in TWS, we will see this order pair reflected appropriately.

Before moving on, I would like to note that this combo order structure is the same structure used for Bear Call/Bull Put orders, Iron Condors, and more. Please reference our documentation for further information.

Bracket Order

With the Combo order complete, I would like to now build out a bracket order. For bracket orders, we can use a different approach than what was used for combos. Here, I will only be making a profit-taker and stop-loss bracket order for an AAPL stock order. This will start as a standard Limit order just like in our prior videos. I will add my action here as a BUY, though instead of my usual “myorder” name, I will call this “parent”. I will also add “parent.transmit = False” so we do not prematurely submit and/or execute a trade.

Now I have my parent order, but I need to go ahead and build my profit taker initially. To do so, I will create my order object, profit_taker. Now I’ll set my order ID to my parentId + 1, and then my parent ID accordingly. I’ll set my action to SELL, another orderType of LMT, and a limit price. Once again, I’ll leave my profit_taker.transmit = False.

And now making this one last order, this time for stop loss. Like before, I will set my stop_loss as my order object name. Then I can deem my stop_loss action as a SELL.

Now I can set my orderType to “STP” in my stop loss, and then set my stop_loss.auxPrice for the stop price. In this instance, I will change my stop_loss.transmit value to TRUE now that I have all of my orders.

Now we can place all of these orders. As usual, I can use my self.placeOrder() request to start placing my orders. I will go ahead and place my order for my parent order, with my parent orderId, mycontract, and then the parent object.

We will then do the same for my profit_taker, with its respective values, and then finally we can end with our stop_loss. I would note that we have to use the parent first, as the other two pieces of the order build off the parent order ID.

Conversely, we must end with the stop loss in this scenario as this contains the final order transmission from that transmit.true or transmit=false.

If we run our code, we can see in Trader Workstation our bracket order posted in our orders summary. We will be able to see these values in our openOrder or orderStatus callbacks.

Bracket orders use the same structure as Hedging orders, and OCA orders. We would advise reviewing our documentation further if you are interested in using these order types.

Order Management

It is important to bear in mind the order efficiency ratio which tracks the ratio of messages sent or submissions, modifications, and cancellations, to the number of orders which actually execute. In general, this ratio is expected to be around 20 or less and is automatically tracked by the Interactive Brokers servers. Please review our IBKRinfo articles describing this topic for more information as well as the calculations to find these values.

This concludes our video on Complex Orders in the TWS API. Thank you for watching, and we look forward to having you join us for more TWS Python API lessons.

Order Management – API User Guide

Bracket Order – API User Guide

Once Cancels All – API User Guide

Code Snippet: Bracket Order

from ibapi.client import *

from ibapi.wrapper import *

from ibapi.contract import ComboLeg

from ibapi.tag_value import TagValue

class TestApp(EClient, EWrapper):

def __init__(self):

EClient.__init__(self, self)

def nextValidId(self, orderId: int):

# Order info

mycontract = Contract()

mycontract.symbol = "AAPL"

mycontract.secType = "STK"

mycontract.exchange = "SMART"

mycontract.currency = "USD"

parent = Order()

parent.orderId = orderId

parent.orderType = "LMT"

parent.lmtPrice = 140

parent.action = "BUY"

parent.totalQuantity = 10

parent.transmit = False

profit_taker = Order()

profit_taker.orderId = parent.orderId + 1

profit_taker.parentId = parent.orderId

profit_taker.action = "SELL"

profit_taker.orderType = "LMT"

profit_taker.lmtPrice = 137

profit_taker.totalQuantity = 10

profit_taker.transmit = False

stop_loss = Order()

stop_loss.orderId = parent.orderId + 2

stop_loss.parentId = parent.orderId

stop_loss.orderType = "STP"

stop_loss.auxPrice = 155

stop_loss.action = "SELL"

stop_loss.totalQuantity = 10

stop_loss.transmit = True

self.placeOrder(parent.orderId, mycontract, parent)

self.placeOrder(profit_taker.orderId, mycontract, profit_taker)

self.placeOrder(stop_loss.orderId, mycontract, stop_loss)

def openOrder(self, orderId: OrderId, contract: Contract, order: Order, orderState: OrderState):

print(f"openOrder: {orderId}, contract: {contract}, order: {order}, Maintenance Margin: {orderState.maintMarginChange}")

def orderStatus(self, orderId: OrderId, status: str, filled: float, remaining: float, avgFillPrice: float, permId: int, parentId: int, lastFillPrice: float, clientId: int, whyHeld: str, mktCapPrice: float):

print(f"orderStatus. orderId: {orderId}, status: {status}, filled: {filled}, remaining: {remaining}, avgFillPrice: {avgFillPrice}, permId: {permId}, parentId: {parentId}, lastFillPrice: {lastFillPrice}, clientId: {clientId}, whyHeld: {whyHeld}, mktCapPrice: {mktCapPrice}")

def execDetails(self, reqId: int, contract: Contract, execution: Execution):

print(f"execDetails. reqId: {reqId}, contract: {contract}, execution: {execution}")

app = TestApp()

app.connect("127.0.0.1", 7497, 1000)

app.run()Combo Order Snippet

from ibapi.client import *

from ibapi.wrapper import *

from ibapi.contract import ComboLeg

from ibapi.tag_value import TagValue

class TestApp(EClient, EWrapper):

def __init__(self):

EClient.__init__(self, self)

def nextValidId(self, orderId: int):

# Order info

mycontract = Contract()

mycontract.symbol = "AAPL,TSLA"

mycontract.secType = "BAG"

mycontract.exchange = "SMART"

mycontract.currency = "USD"

leg1 = ComboLeg()

leg1.conId = 76792991

leg1.ratio = 1

leg1.action = "BUY"

leg1.exchange = "SMART"

leg2 = ComboLeg()

leg2.conId = 265598

leg2.ratio = 1

leg2.action = "SELL"

leg2.exchange = "SMART"

mycontract.comboLegs = []

mycontract.comboLegs.append(leg1)

mycontract.comboLegs.append(leg2)

myorder = Order()

myorder.orderId = orderId

myorder.action = "BUY"

myorder.orderType = "LMT"

myorder.lmtPrice = 80

myorder.totalQuantity = 10

myorder.tif = "GTC"

myorder.smartComboRoutingParams = []

myorder.smartComboRoutingParams.append(TagValue('NonGuaranteed', '1'))

self.placeOrder(orderId, mycontract, myorder)

def openOrder(self, orderId: OrderId, contract: Contract, order: Order, orderState: OrderState):

print(f"orderId: {orderId}, contract: {contract}, order: {order}, Maintenance Margin: {orderState.maintMarginChange}")

def orderStatus(self, orderId: OrderId, status: str, filled: float, remaining: float, avgFillPrice: float, permId: int, parentId: int, lastFillPrice: float, clientId: int, whyHeld: str, mktCapPrice: float):

print(f"orderStatus. orderId: {orderId}, status: {status}, filled: {filled}, remaining: {remaining}, avgFillPrice: {avgFillPrice}, permId: {permId}, parentId: {parentId}, lastFillPrice: {lastFillPrice}, clientId: {clientId}, whyHeld: {whyHeld}, mktCapPrice: {mktCapPrice}")

def execDetails(self, reqId: int, contract: Contract, execution: Execution):

print(f"execDetails. reqId: {reqId}, contract: {contract}, execution: {execution}")

app = TestApp()

app.connect("127.0.0.1", 7497, 1000)

app.run()

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Please keep in mind that the examples discussed in this material are purely for technical demonstration purposes, and do not constitute trading advice. Also, it is important to remember that placing trades in a paper account is recommended before any live trading.

I wonder how to code the one cancels all order in python. Could you show us a complete sample code for reference? Thank you very much!

Hello William, thank you for asking! We have just the resource you are looking for on IBKR Campus: https://www.interactivebrokers.com/campus/ibkr-quant-news/how-to-code-one-cancels-all-orders-in-python/. We hope this helps!

How do you do this for a MKT parent order?

Hello David, thank you for reaching out. Advanced orders such as Bracket Orders or Hedging involve attaching child orders to a parent. This can be easily done via the IBApi.Order.ParentId attribute by assigning a child order’s IBApi.Order.ParentId to an existing order’s IBApi.Order.OrderId. When an order is attached to another, the system will keep the child order ‘on hold’ until its parent fills. Once the parent order is completely filled, its children will automatically become active. Also, it is a very good idea to make use of the IBApi.Order.Transmit flag as demonstrated in Bracket Orders. However, if this is not your question- feel free to create a web ticket to contact our API experts. They would be happy to help.

https://www.interactivebrokers.com/sso/resolver?action=NEW_TICKET.

How do you do this if you are trading futures and you want to buy/sell 2 contracts with a profit taker at say 5% and one at 10% with stops for each contract at 5% from purchase price. This is something possible in ToS, and I’m wondering how to implement with TWS API. Thanks!

Hello Kevin, thank you for reaching out. Because the content of the combo order is built from the contract, and the bracket order is assembled by an order object, all you would need to do is use the contract as described in the video, and then make a standard bracket order referencing the combo contract as the target for each bracket leg. Market data can be received, as described in Lesson 5: Requesting Market Data, and then used to calculate your prices.

How to create stop-loss price for positions

thanks

Hello, thank you for reaching out. We have several stop loss orders available. Please check out this page for more details.

https://interactivebrokers.github.io/tws-api/basic_orders.html

What is the maximum number of legs on a combo? Your article states that it “could have up to six legs”. Does it hold for option combos?

thanks

Hi Arnold, thank you for reaching out. Interactive Brokers supports 6-legged combos. With that being said, some exchanges will not allow 6 legged combos. In this case, SPX and CBOE do not support 6-legged combos. Meanwhile, NASDAQ does support a 6-legged combo for stocks. This will vary on an exchange-by-exchange basis. Please reach out again if you have any more questions. We are here to help!

I’m reading active open future combo order using the tws API where I have limit and stop order for the entire combo. When my handler “openOrder” is called, I get a “BAG” order with a contract with legs. Each leg has information such as “656793020|1|CME,656793167|-2|CME” how do get the leg strike, expiration, Right etc from conId (656793020) ?

Hello, thank you for asking. Users can request contract details using ConIds and the Exchange value. This will return the full contents of the contract such as symbol, strike, expiration, right, and so on. You can view more about requesting contract details in our previous lesson, https://www.interactivebrokers.com/campus/trading-lessons/essential-components-of-tws-api-programs/ during the “Futures Contract” discussion.

Please reach out with any more questions. We are here to help!

How can one get a price of a combo order for options. Say SPY ATM straddle.

In lesson 8 of API for python, regarding a positive or negative stock combo. It is never explained clearly what a net positive combo. means vs. net negative. Is it referring to net dollars or net shares? I will have to figure it out based on the examples given.

Hello, thank you for asking. The ‘Net Positive’ and ‘Net Negative’ terms are referring to the dollar amount, as this will indicate a Credit or Debit spread. Please be aware that this video series is only intended for use with how to perform certain actions through the TWS API. This should not be considered investment advice. Please reach back out with any additional questions. We are here to help!

For the Bracket Order, why is the profit_taker.lmtPrice set to $137 and the stop_loss.auxPrice set to $155? I would think that those numbers would be the opposite since in this example we are submitting a buy order at $140. Am I mistaken in my approach?

Excellent videos thus far. Thank you again.

Hello, thank you for pointing this out. The prices for the Profit Taker and the Stop Loss are flipped. This information has been passed to the appropriate team, and they are looking to resolve this for future tutorial releases. Please reach back out with any additional questions. We are here to help!

Is it possible to add a time condition to a Bracket Order?

Hello, thank you for asking. It is possible to add a time condition to a bracket order. The order conditions can be applied to just the parent order or either of the legs. Please note that if a time condition is applied to the parent order, regardless of whether or not the child orders have a time condition, the order will wait until the parent condition is met. If you have any additional questions, please create a web ticket for this inquiry; we have a category specifically for “API.” One of our API experts will be happy to guide you! https://spr.ly/IBKR_ClientServicesCampus

Hello.

I have a live account with realtime data subscribed, and in my paper trading account I can receive realtime data with no problem. But when I place orders (bracket orders) in my paper trading account, orders are filled with a 10-minute delay (in the US futures market).

Say I place a BUY order at $1000 and stop loss at $900. BUY order get filled based on a 10-minute delayed price, and SL gets triggered not at the time when the price hit $900 and lower, but 10 minutes after that point. BUY order get filled if the 10-minute old price level satisfies the condition, even if the price never touched $1000 after placing it. What am I doing wrong here?

Thank you for your help!

Hello, thank you for reaching out. For time-sensitive trading inquiries, please contact Client Services via phone: https://spr.ly/IBKR_ClientServicesCampus

Is it possible to have a ladder entry using a combo or bracket order? I’ve been trying to place two orders with take profit + stop loss attached, but the orders get rejected along the lines of “can’t have open orders on both sides of the trade”. So again, I’m trying to place a buy bracket at -10% and -20% of the current price, but presumably because they have a TP sell order attached they get rejected – is there a solution for this?

Hello, How the effective multiplier is calculated for the combo order in case the legs were: 1 Long MNQ , 1 Short MES and 1 Short MYM, futures contracts, having an individual multiplier of: 2.0 , 5.0 and 0.5 respectively.

Hello, the easiest way to find the multiplier for a particular product is through the Description window in Trader Workstation: (1) Right click on the product in question and select Financial Instrument Info followed by Description or Details. (2) The window will populate and will list information related to the product, including its multiplier. We hope this helps.

Hi, how does one need to modify the parameters of mycontract to trade say Oil spreads? Do the parameters change if the exchange has native spreads?

Hello, thank you for asking. For the exchange-hosted commodity spreads, this contract will appear slightly different. In particular, you may see the contract’s symbol field set to something like “COL.WTI” for a combination of Coil and WTI futures. In other cases, you may find a generic symbol like “FYT”. A larger discussion on this combination behavior can be found in our Contract documentation at https://www.interactivebrokers.com/campus/ibkr-api-page/contracts/#inter-com-fut.

Hello and thankyou in advance. How do we use python to place orders on the platform like: Iron Condor BULL PUT Vertical Bear PUT vertical Butterfly Straddle You get the picture, Sample python code would help me enourmously. Kind regards