- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Lesson 5 of 10

Already an Interactive Brokers Client?

New to Interactive Brokers?

Apart from reading an issuer’s official statement or attending an investor presentation about an issuer’s proposed offering, investment decisions about municipal bonds typically require additional information from certain organizations in the ecosystem in which these instruments are issued and traded.

Along with other fundamental factors that investors may use to assess the risks associated with municipal securities, institutions such as municipal bond guarantors, as well as credit rating agencies such as S&P Global, Moody’s Investors Service, and Fitch Ratings each play a role in the issuance and trading process.

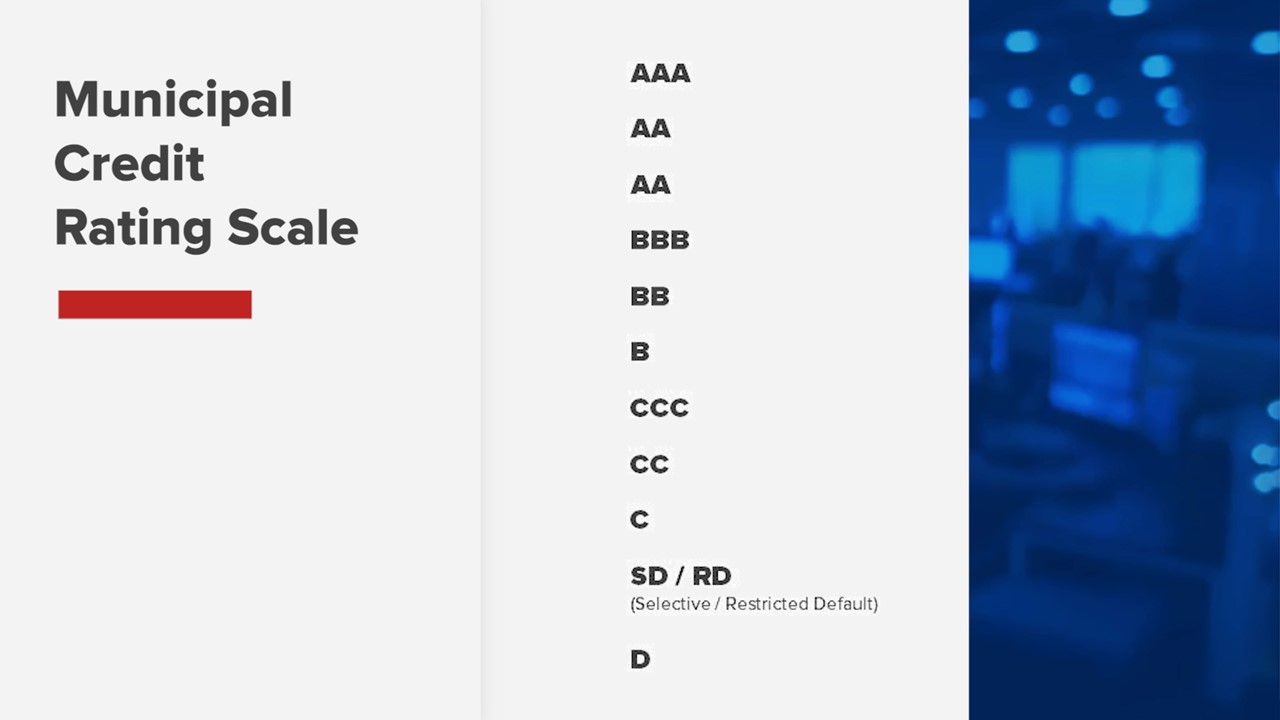

For example, certain credit rating agencies typically use a scale to categorize the creditworthiness of most issuers of municipal debt, as well as their debt offerings, with designations usually divided into investment-grade (‘AAA’-‘BBB’) and lower-quality (“BB’-‘C’) credits.

The following are key takeaways from an interview between Interactive Brokers’ senior market analyst Steven Levine and Ed Grebeck, a strategist in the global debt markets and an expert in the bond Insurance and rating agency industries. Grebeck had given one of the earliest warnings to investors about the global financial crisis.

With equity investments, individual investors can do their own research into each individual company, with the hope of finding one of the gems that’s going to rapidly increase in value, and they also want to make sure that its value doesn’t collapse.

With respect to bonds, all they’re hoping to get is their principal investment back plus some interest over the period.

In the case of municipal bonds, rating agencies will usually look at items such as:

They will seek to answer questions that may include:

In aggregating all these factors, the rating agency will assign a credit rating aligned with their scale.

Meanwhile, rating agencies will also assign a credit rating to bond insurers, with ‘AA’ currently the highest.

The ratings agencies set up the capital charges that influences the bond insurer’s investment-grade double-‘A’ rating based on what its investments are.

For example:

If the bond insurer’s guarantee is for an ‘A’-rated or double-‘A’ rated credit, they may allow pennies on the dollar of capital; but if they were to guarantee a double-‘B’ rated investment, that may require several dollars of capital for every hundred guaranteed.

For example:

In 1978-79, the New York State budget was roughly US$16bn, while in 2018-19, it mushroomed to around US$175bn. This represents a compound annual growth rate (CAGR) of more than 6% over that 40-year period.

Over the same timeframe, the state’s population has grown from about 17.5 million to 19.5 million – a CAGR of around 0.25%.

An investor would most likely be hard-pressed to identify any business that would grow as fast as New York State, while its economy is shrinking.

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!