- Solve real problems with our hands-on interface

- Progress from basic puts and calls to advanced strategies

Interactive Options Course

Posted January 3, 2023 at 3:20 pm

By Kaiko

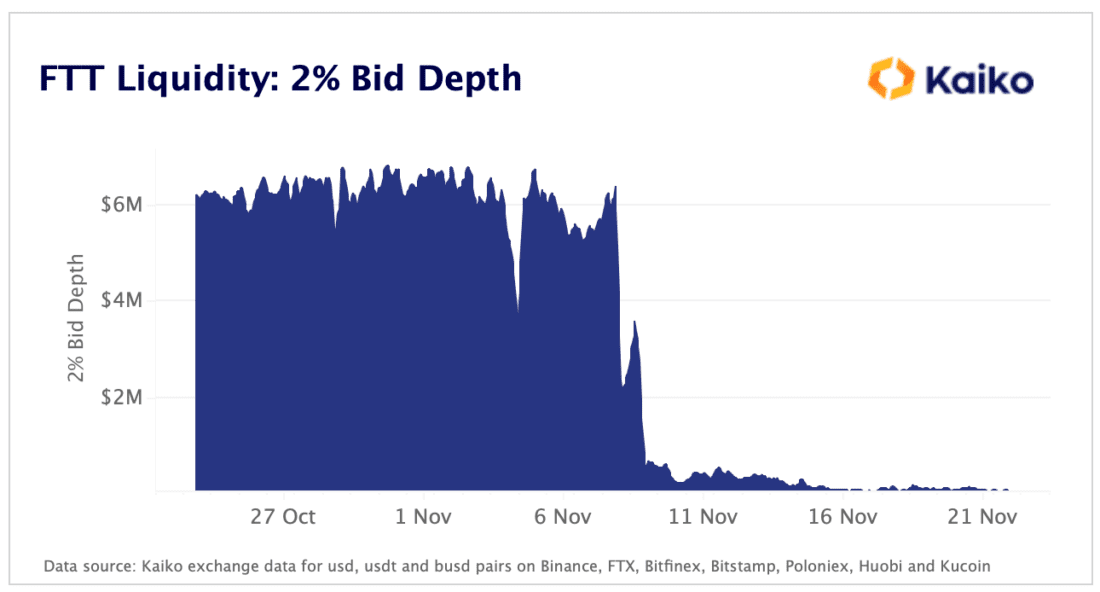

Liquidity is deeply misunderstood in crypto markets. Specifically, the metric “market depth”. Unless you are a trader, it can be hard to wrap your head around the meaning of “2% Bid Depth” and how it relates to the value of an asset.

As FTX collapsed, we took a hard look at liquidity for FTT, specifically aggregated market depth across all active markets. We noticed that just a few million dollars in bid-side depth existed on FTT order books, despite Alameda valuing this asset in the billions of dollars on their balance sheet. Essentially, what this meant is that if the FTX/Alameda entity needed to liquidate their FTT holdings, say in the case of a bank run, they would only be able to sell a few million dollars worth before suffering massive price slippage.

It now turns out that Alameda was almost certainly propping up the price of the FTT token, meaning that in the event of a sell-off, Alameda would be forced to fill these orders and accept the loss.

How could no one have noticed this obvious mismatch in valuation vs. actual market liquidity? In traditional finance, an asset’s liquidity is incorporated into its valuation on a balance sheet through various accounting methods that factor in real market conditions. This is exactly what FTX did not do. In fact, we now know they didn’t even have a real accounting department.

My new year’s wish is that all investors gain a deep understanding of the meaning of liquidity and an appreciation for tried and tested balance sheet accounting principals.

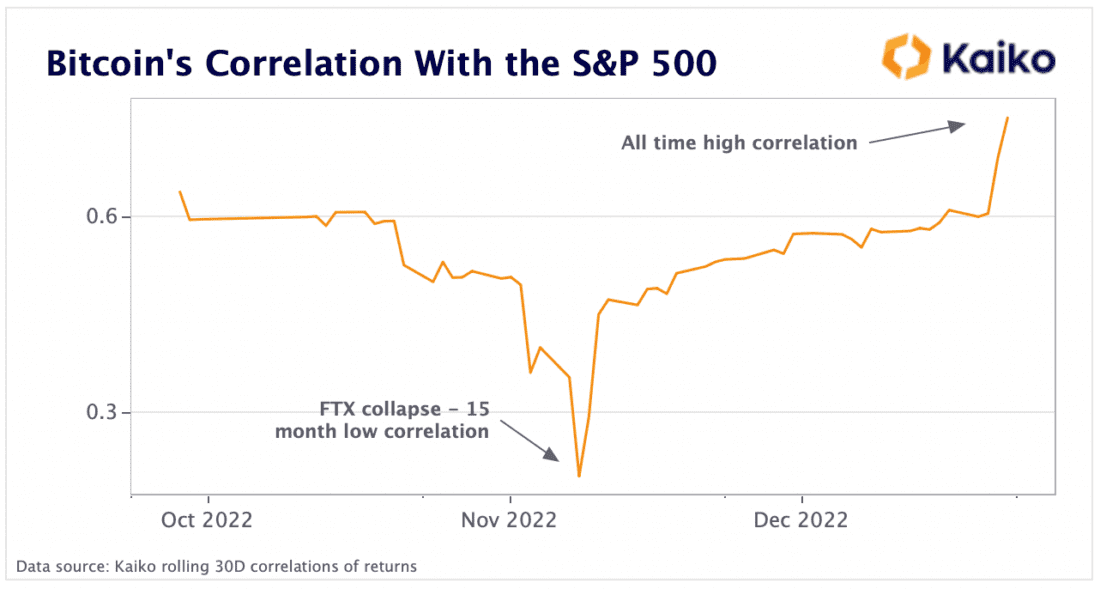

Throughout Q4, BTC’s correlation with the S&P 500 hit both an all time high and dropped to 15-month lows. The lows were reached during FTX’s collapse, while the highs emerged in the final week of December. This is the best evidence yet that macro is back.

Over the past year, global interest rate hikes have helped create the least friendly macro environment for risk assets in years, evidenced by a dramatic drawdown for crypto, equities and everything in between. Correlations across asset classes have never been higher, and it seems that the only times crypto diverged in 2022 was during idiosyncratic market events.

Central banks continued to be extremely aggressive in Q4, despite recent indicators that inflation is slowing faster than expected. Over the coming months we can expect a period of volatility resulting from the mismatch between the Fed’s hawkish rhetoric and market rate expectations, with US traders still betting on rate cuts in late 2023 as recession indicators flash red.

While the crypto industry has plenty of things to worry about right now, investors should pay close attention to changes in interest rates over the coming months. Macro could very well be be the single biggest market catalyst in 2023.

Like everyone this quarter, I found myself questioning everything I knew about crypto; specifically, what real world problems it actually solves right now. Its easy to point to the potential of this great space, but something that is needed to quiet critics in bear markets is actual product-market fit.

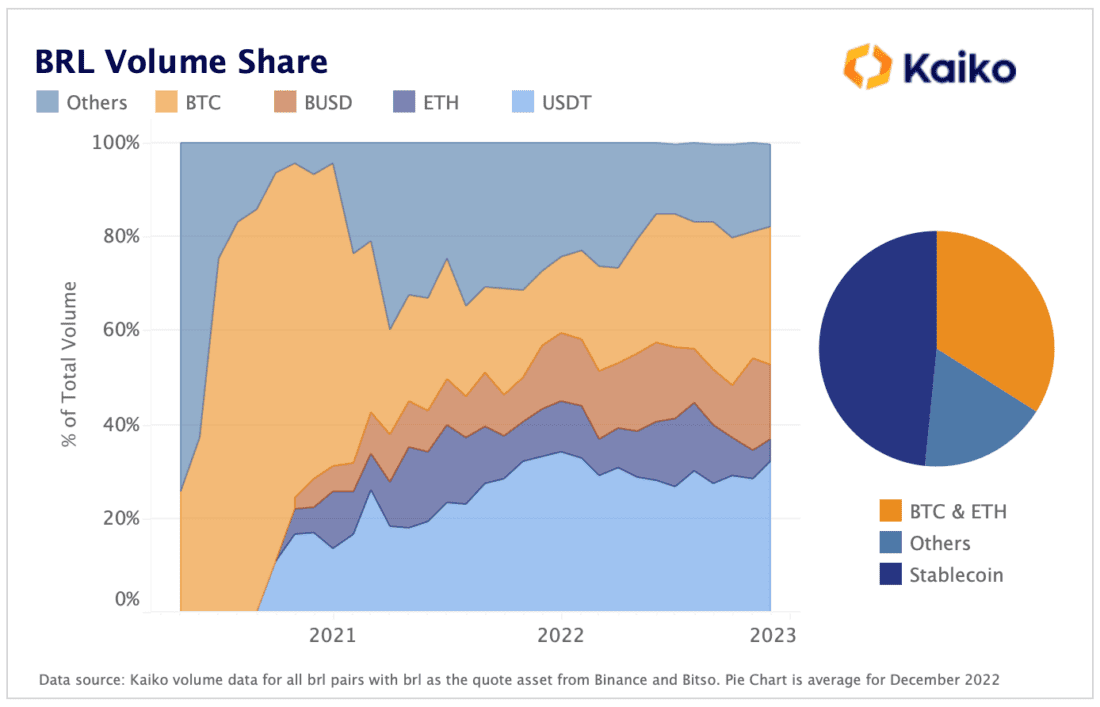

The good news is that crypto in developing economies represents something completely different to what we’re used to in Europe or the US. In developed economies, crypto represents a path to financial freedom, a safe keeping of savings and an opportunity to globalise wealth. In more developed economies, crypto is really just an investment opportunity to take part in the future of finance – it’s not saving us from much right now.

The role of crypto in developing economies is particularly important as inflation decimates savings in local currencies. This has created strong demand for USD-pegged assets, and stablecoins fill that need perfectly. We have a story on the usage in Brazil in the report, but we saw similar trends in Turkey and Mexico to name just a couple.

Stablecoins look to be crypto’s best example of product market fit and they’re genuinely improving a vast amount of lives in these countries. As long as this continues, crypto will survive and grow to solve more problems.

Q4 brought a fitting end to a rotten year in crypto as the excesses of the previous bull market were washed out in dramatic fashion. This time it was brought about by the man who had been anointed the face of crypto and regulatory voice of reason by FTX’s marketing department and fawning VCs who thought they had the next Zuckerberg. Instead, it turns out they had backed a less charismatic Elizabeth Holmes.

For an industry founded on decentralization, crypto seems to desperately gravitate towards larger than life figures, to pin its hopes on a genius builder who can bring TVL to a struggling chain or a YouTuber who can hold SBF accountable.

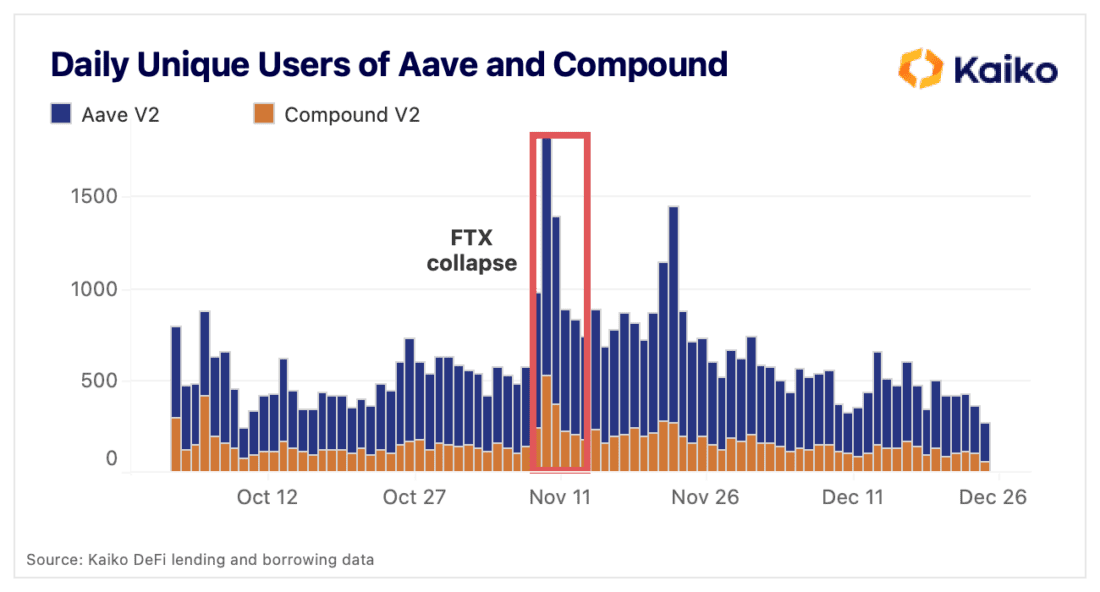

In 2023 I hope we can leave some of this mentality behind and instead focus on what makes this space exciting and different from a run-of-the-mill grift. Despite all its promise, DeFi and crypto generally have still not lived up to lofty expectations of disrupting traditional finance and solving problems for real people. Yes, it proved itself resilient following FTX’s collapse, but look at how few daily unique users there are of Ethereum’s largest lending and borrowing platforms.

There is still much work to be done to 1) make crypto more useful; 2) make crypto easier to use; and 3) limit bad actors. People like SBF create a permanent scar on crypto’s reputation, but this can be overcome by focusing on innovation and onboarding.

Specifically, I’ll be closely watching the DeFi lending and borrowing space develop, as Aave and Compound have opted for two different visions for their futures. Is it possible that Uniswap V3 will continue its utter dominance, or will other innovative DEXs be able to capture a significant share of volumes? Which Layer 2s will achieve lasting adoption post-airdrop, and which decentralized futures exchange will come out on top? These are the questions and debates that make crypto interesting, not glossy profiles of founders.

—

Originally Posted January 2, 2022 – The True Meaning of Liquidity

Smartkarma posts and insights are provided for informational purposes only and shall not be construed as or relied upon in any circumstances as professional, targeted financial or investment advice or be considered to form part of any offer for sale, subscription, solicitation or invitation to buy or subscribe for any securities or financial products. Views expressed in third-party articles are those of the authors and do not necessarily represent the views or opinion of Smartkarma.

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Smartkarma and is being posted with its permission. The views expressed in this material are solely those of the author and/or Smartkarma and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

TRADING IN BITCOIN FUTURES IS ESPECIALLY RISKY AND IS ONLY FOR CLIENTS WITH A HIGH RISK TOLERANCE AND THE FINANCIAL ABILITY TO SUSTAIN LOSSES. More information about the risk of trading Bitcoin products can be found on the IBKR website. If you're new to bitcoin, or futures in general, see Introduction to Bitcoin Futures.

TRADING IN BITCOIN FUTURES IS ESPECIALLY RISKY AND IS ONLY FOR CLIENTS WITH A HIGH RISK TOLERANCE AND THE FINANCIAL ABILITY TO SUSTAIN LOSSES. More information about the risk of trading Bitcoin products can be found on the IBKR website. If you're new to bitcoin, or futures in general, see Introduction to Bitcoin Futures.

Related Articles

Join The Conversation

For specific platform feedback and suggestions, please submit it directly to our team using these instructions.

If you have an account-specific question or concern, please reach out to Client Services.

We encourage you to look through our FAQs before posting. Your question may already be covered!